Copy to clipboard

Copy to clipboard

DJO’s parent company, Colfax Corporation, announced its intention to split into two public companies to sharpen its strategic focus and capitalize on its medical technology business opportunities. The new alignment, which is projected to be complete by the first quarter of 2022, is expected to boost the momentum that DJO has gained in the joint replacement market in recent years.

“Our abilities to successfully develop talent, drive innovation, leverage our Colfax Business System for continuous improvement and acquire attractive businesses are core to both MedTech and FabTech,” Colfax CEO Matt Trerotola said of the company split. “We believe a separation will better position each business to execute tailored strategies to deliver above-market growth, margin expansion and strong, consistent free cash flow.”

The Colfax Years

Colfax purchased DJO from the Blackstone Group in early 2019 for $3.15 billion. At the time, Colfax was a diversified technology company that provided air & gas handling and fabrication products and services to global customers. While Colfax’s purchase surprised those within orthopedics, the company sought a significant acquisition to enter the medical device space. Mr. Trerotola noted they specifically targeted the high-margin orthopedic market and a company that brought opportunities to improve and grow and a multi-year transformation to reduce costs and expand margins.

At the time of the acquisition, DJO was undergoing its own waves of transformation. The company consolidated its distribution and outsourced its logistics, improved its procurement process to reduce production costs and enhanced its quote-to-collection process. The Colfax Business System’s additional layer for continuous improvements better positioned DJO to pursue growth through acquisitions and portfolio expansions in 2019 and 2020.

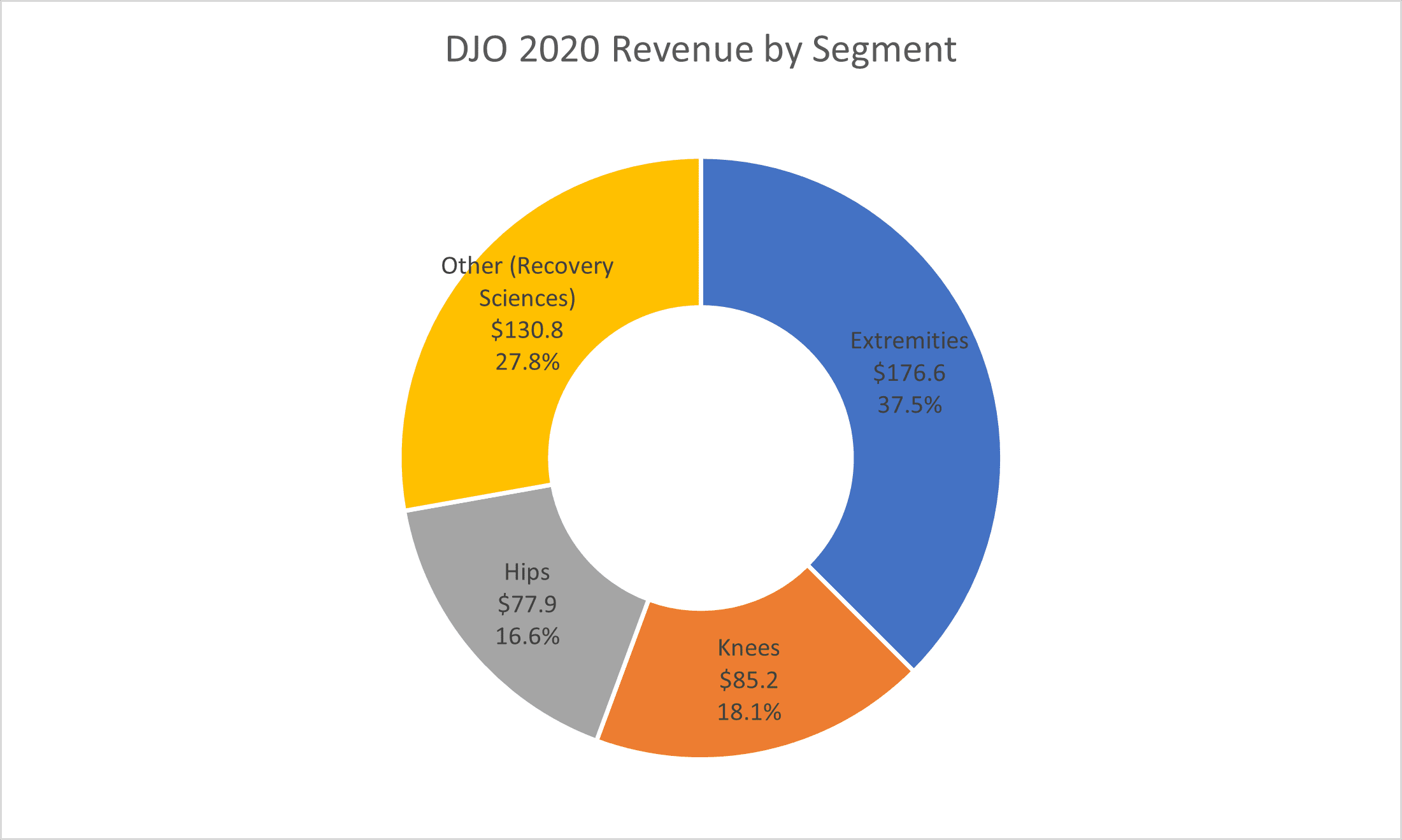

Colfax’s MedTech business secured revenue of $1.12 billion in 2020. Our estimates for 2020 orthopedic revenue were $470.5 million, -8.8% vs. 2019. Exhibit 1 shows DJO’s revenue from 2016 to 2020. Exhibit 2 shows DJO’s revenue split by segment. The company’s implant business accounts for about one third of its revenue. DJO’s Prevention and Rehabilitation division includes bracing, bone growth and muscle stimulators and various therapy solutions.

Exhibit 1: DJO Revenue 2016 to 2020

| Segment | FY 16 | FY17 | FY18 | FY19 | FY20 |

|---|---|---|---|---|---|

| Joint Replacement | $273.9 | $306.0 | $329.2 | $368.1 | $339.7 |

| Joint Replacement Growth % | 11.7% | 7.6% | 11.8% | -7.7% | |

| Knees | $72.3 | $79.0 | $86.9 | $95.8 | $85.2 |

| Knees Growth % | 9.2% | 10.1% | 10.2% | -11.0% | |

| Hips | $63.4 | $69.2 | $74.7 | $81.5 | $77.9 |

| Hips Growth % | 9.2% | 7.9% | 9.1% | -4.3% | |

| Extremities | $138.2 | $157.8 | $167.6 | $190.8 | $176.6 |

| Extremities Growth % | 14.2% | 6.2% | 13.9% | -7.5% | |

| Other (Recovery Sciences) | $147.9 | $147.7 | $146.3 | $148.1 | $130.8 |

| Other Growth % | -0.1% | -0.9% | 1.2% | -11.7% | |

| Total | $421.8 | $453.7 | $475.6 | $516.2 | $470.5 |

| Total Growth % | 7.6% | 4.8% | 8.5% | -8.8% |

Exhibit 2: DJO 2020 Revenue Split by Segment

The Portfolio Expansion

DJO’s surgical division is primarily focused on joint replacement, with a strong presence in the upper extremity. Our 2020 estimates had DJO as the seventh-largest joint replacement company and the fourth-largest extremities joint replacement company. In 2019, they were one of only three companies to exceed the mark of double-digit percent growth, along with Wright Medical (now part of Stryker) and Medacta.

Believing that it needed a presence in lower extremities, DJO implemented an aggressive bolt-on acquisition strategy in late 2020 that netted Stryker’s STAR total ankle and Trilliant Surgical. Trilliant’s portfolio of reconstruction and fixation products netted DJO a dedicated foot and ankle business line.

The company noted a rapidly aging population, sports-related injuries and increased prevalence of diabetes as key drivers of the foot and ankle market. Colfax expects the foot and ankle business to contribute $100 million in annual revenue within a few years. Leadership said it intends to remain active in developing tuck-in acquisition opportunities, primarily targeting companies in the $20 million to $30 million range. Of note, DJO’s bracing business also has a presence in the foot and ankle market.

“We’ve got a robust project we’re using very actively in our Med Tech business,” Mr. Trerotola said. “We’ve built a very robust funnel of opportunities, some of which are direct bolt-ons and some of which are more adjacencies. We’ve talked about looking at things in the small- to medium-sized range, because there’s a lot of attractive stuff that we can do in that range.”

In addition to the acquisitions, DJO remained active with new product introductions across its shoulder, hip and knee lines in 2020.

In hip and knee, DJO launched the EMPOWR Acetabular™ system and the EMPOWR Partial Knee™. EMPOWR joint replacement systems are designed to restore healthy kinematics and optimize surgical efficiencies by allowing implantation with a single tray.

“These EMPOWR advances support the acceleration of outpatient total joint procedures and the procedure migration to the ASC setting where surgeons increasingly rely on streamlined solutions,” Louis Vogt, Vice President of Sales & Marketing of DJO Surgical, said at product launch.

In extremities, DJO introduced AltiVate® Anatomic CS EDGE. The device design is based on a humeral fit analysis conducted to help optimize the fit of peripherally targeted fins within the humeral metaphysis. AltiVate Anatomic CS EDGE features a 3-fin humeral stem with serrated fin tips, allowing surgeons the option to use the implant to cut into the bone.

Also in 2020, DJO introduced Motion iQ™, a software solution designed to connect the orthopedic surgeon, care team and patient through an entire episode of care surrounding total joint replacement procedures. The app could potentially have a broader reach and adoption than competitive products due to DJO’s presence in the prehab and rehab portions of the market. Motion iQ offers personalized messaging and customized home recovery exercises and content to reinforce the surgical team’s guidance. Further, it sends the care team health and activity data.

The addition of a lower extremities line and software solutions technology follows the strategies of other large- and medium-sized joint replacement companies, presumably allowing DJO to better compete in the space.

What’s Next?

The yet-to-be-named orthopedic company is expected to be its own entity by the first quarter of 2022. Leading the new company will be Matt Trerotola (CEO), Brady Shirley (COO) and Chris Hix (CFO) – all current Colfax executives. Mr. Trerotola has served as CEO of Colfax since 2015, and Mr. Hix joined as CFO in 2016. Mr. Shirley, who has nearly three decades of experience in medical device, has been with DJO since 2014 and served as CEO since 2016.

Leaders of the new company remain bullish on the joint replacement market, and expect to be firmly positioned for organic and acquisition growth in coming years. While many orthopedic companies have refrained from providing 2021 guidance, Colfax expects a strong return of sales in 2021 with its MedTech company reaching ~$1.4 billion, +21% to +24% growth over 2020, or roughly +11% to +13% versus 2019. Progressively, the company’s focus will include aggressive growth and expansion of its joint replacement business and extension into attractive adjacencies. During its Investor Day meeting, Colfax leadership said that it aims to reach $1.7 to $2 billion by 2023.

DJO’s parent company, Colfax Corporation, announced its intention to split into two public companies to sharpen its strategic focus and capitalize on its medical technology business opportunities. The new alignment, which is projected to be complete by the first quarter of 2022, is expected to boost the momentum that DJO has gained in the...

DJO’s parent company, Colfax Corporation, announced its intention to split into two public companies to sharpen its strategic focus and capitalize on its medical technology business opportunities. The new alignment, which is projected to be complete by the first quarter of 2022, is expected to boost the momentum that DJO has gained in the joint replacement market in recent years.

“Our abilities to successfully develop talent, drive innovation, leverage our Colfax Business System for continuous improvement and acquire attractive businesses are core to both MedTech and FabTech,” Colfax CEO Matt Trerotola said of the company split. “We believe a separation will better position each business to execute tailored strategies to deliver above-market growth, margin expansion and strong, consistent free cash flow.”

The Colfax Years

Colfax purchased DJO from the Blackstone Group in early 2019 for $3.15 billion. At the time, Colfax was a diversified technology company that provided air & gas handling and fabrication products and services to global customers. While Colfax’s purchase surprised those within orthopedics, the company sought a significant acquisition to enter the medical device space. Mr. Trerotola noted they specifically targeted the high-margin orthopedic market and a company that brought opportunities to improve and grow and a multi-year transformation to reduce costs and expand margins.

At the time of the acquisition, DJO was undergoing its own waves of transformation. The company consolidated its distribution and outsourced its logistics, improved its procurement process to reduce production costs and enhanced its quote-to-collection process. The Colfax Business System’s additional layer for continuous improvements better positioned DJO to pursue growth through acquisitions and portfolio expansions in 2019 and 2020.

Colfax’s MedTech business secured revenue of $1.12 billion in 2020. Our estimates for 2020 orthopedic revenue were $470.5 million, -8.8% vs. 2019. Exhibit 1 shows DJO’s revenue from 2016 to 2020. Exhibit 2 shows DJO’s revenue split by segment. The company’s implant business accounts for about one third of its revenue. DJO’s Prevention and Rehabilitation division includes bracing, bone growth and muscle stimulators and various therapy solutions.

Exhibit 1: DJO Revenue 2016 to 2020

| Segment | FY 16 | FY17 | FY18 | FY19 | FY20 |

|---|---|---|---|---|---|

| Joint Replacement | $273.9 | $306.0 | $329.2 | $368.1 | $339.7 |

| Joint Replacement Growth % | 11.7% | 7.6% | 11.8% | -7.7% | |

| Knees | $72.3 | $79.0 | $86.9 | $95.8 | $85.2 |

| Knees Growth % | 9.2% | 10.1% | 10.2% | -11.0% | |

| Hips | $63.4 | $69.2 | $74.7 | $81.5 | $77.9 |

| Hips Growth % | 9.2% | 7.9% | 9.1% | -4.3% | |

| Extremities | $138.2 | $157.8 | $167.6 | $190.8 | $176.6 |

| Extremities Growth % | 14.2% | 6.2% | 13.9% | -7.5% | |

| Other (Recovery Sciences) | $147.9 | $147.7 | $146.3 | $148.1 | $130.8 |

| Other Growth % | -0.1% | -0.9% | 1.2% | -11.7% | |

| Total | $421.8 | $453.7 | $475.6 | $516.2 | $470.5 |

| Total Growth % | 7.6% | 4.8% | 8.5% | -8.8% |

Exhibit 2: DJO 2020 Revenue Split by Segment

The Portfolio Expansion

DJO’s surgical division is primarily focused on joint replacement, with a strong presence in the upper extremity. Our 2020 estimates had DJO as the seventh-largest joint replacement company and the fourth-largest extremities joint replacement company. In 2019, they were one of only three companies to exceed the mark of double-digit percent growth, along with Wright Medical (now part of Stryker) and Medacta.

Believing that it needed a presence in lower extremities, DJO implemented an aggressive bolt-on acquisition strategy in late 2020 that netted Stryker’s STAR total ankle and Trilliant Surgical. Trilliant’s portfolio of reconstruction and fixation products netted DJO a dedicated foot and ankle business line.

The company noted a rapidly aging population, sports-related injuries and increased prevalence of diabetes as key drivers of the foot and ankle market. Colfax expects the foot and ankle business to contribute $100 million in annual revenue within a few years. Leadership said it intends to remain active in developing tuck-in acquisition opportunities, primarily targeting companies in the $20 million to $30 million range. Of note, DJO’s bracing business also has a presence in the foot and ankle market.

“We’ve got a robust project we’re using very actively in our Med Tech business,” Mr. Trerotola said. “We’ve built a very robust funnel of opportunities, some of which are direct bolt-ons and some of which are more adjacencies. We’ve talked about looking at things in the small- to medium-sized range, because there’s a lot of attractive stuff that we can do in that range.”

In addition to the acquisitions, DJO remained active with new product introductions across its shoulder, hip and knee lines in 2020.

In hip and knee, DJO launched the EMPOWR Acetabular™ system and the EMPOWR Partial Knee™. EMPOWR joint replacement systems are designed to restore healthy kinematics and optimize surgical efficiencies by allowing implantation with a single tray.

“These EMPOWR advances support the acceleration of outpatient total joint procedures and the procedure migration to the ASC setting where surgeons increasingly rely on streamlined solutions,” Louis Vogt, Vice President of Sales & Marketing of DJO Surgical, said at product launch.

In extremities, DJO introduced AltiVate® Anatomic CS EDGE. The device design is based on a humeral fit analysis conducted to help optimize the fit of peripherally targeted fins within the humeral metaphysis. AltiVate Anatomic CS EDGE features a 3-fin humeral stem with serrated fin tips, allowing surgeons the option to use the implant to cut into the bone.

Also in 2020, DJO introduced Motion iQ™, a software solution designed to connect the orthopedic surgeon, care team and patient through an entire episode of care surrounding total joint replacement procedures. The app could potentially have a broader reach and adoption than competitive products due to DJO’s presence in the prehab and rehab portions of the market. Motion iQ offers personalized messaging and customized home recovery exercises and content to reinforce the surgical team’s guidance. Further, it sends the care team health and activity data.

The addition of a lower extremities line and software solutions technology follows the strategies of other large- and medium-sized joint replacement companies, presumably allowing DJO to better compete in the space.

What’s Next?

The yet-to-be-named orthopedic company is expected to be its own entity by the first quarter of 2022. Leading the new company will be Matt Trerotola (CEO), Brady Shirley (COO) and Chris Hix (CFO) – all current Colfax executives. Mr. Trerotola has served as CEO of Colfax since 2015, and Mr. Hix joined as CFO in 2016. Mr. Shirley, who has nearly three decades of experience in medical device, has been with DJO since 2014 and served as CEO since 2016.

Leaders of the new company remain bullish on the joint replacement market, and expect to be firmly positioned for organic and acquisition growth in coming years. While many orthopedic companies have refrained from providing 2021 guidance, Colfax expects a strong return of sales in 2021 with its MedTech company reaching ~$1.4 billion, +21% to +24% growth over 2020, or roughly +11% to +13% versus 2019. Progressively, the company’s focus will include aggressive growth and expansion of its joint replacement business and extension into attractive adjacencies. During its Investor Day meeting, Colfax leadership said that it aims to reach $1.7 to $2 billion by 2023.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.