Copy to clipboard

Copy to clipboard

Acquisitions, divestitures, market entries and exits have shaped portfolios for many of the orthopaedic industry’s top players, in recent years. In this article, we look at such activity from the ten companies that represent #6 through #15 on our list of the largest device companies ranked by revenue: Arthrex, DJO, NuVasive, Aesculap, Wright Medical, Globus Medical, ConMed, Orthofix, Exactech and Acumed.

While orthopaedics‘ top five companies—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew and Medtronic—are diversifying across market segments, the ten companies in this group primarily specialize within one or two areas of joint reconstruction, spine, arthroscopy/soft tissue and extremities.

According to our estimates, these companies range in annual revenue from $250 million to $2 billion (See Exhibit 1.), and accounted for nearly $7.5 billion or 15.5% of the orthopaedic industry‘s $48.1 billion in 2016 revenue. New product launches and acquisitions drove all but Aesculap and ConMed to post above-market overall growth of 3.2% in 2016 vs. 2015. This stands in contrast to the growth posted by the top five; of those, only two companies posted growth at or above market in 2016: Stryker at 4.9% and Zimmer Biomet at 3.2%.

Exhibit 1: Performance for Orthopaedic Device Players from #6 to #15 ($Millions)

| Company | 2016 | 2015 | $ Chg | % Chg |

|---|---|---|---|---|

| Arthrex | $2,048.0 | $1,833.1 | $214.9 | 11.7% |

| DJO | $1,155.4 | $1,113.6 | $41.8 | 3.8% |

| NuVasive | $962.1 | $811.1 | $151.0 | 18.6% |

| Aesculap | $731.1 | $711.9 | $19.2 | 2.7% |

| Wright Medical | $690.4 | $626.4 | $64.0 | 10.2% |

| Globus Medical | $564.0 | $544.8 | $19.2 | 3.5% |

| ConMed | $422.1 | $444.9 | ($22.8) | (5.1%) |

| Orthofix | $409.8 | $396.5 | $13.3 | 3.4% |

| Exactech | $258.8 | $243.7 | $15.1 | 6.2% |

| Acumed | $251.7 | $238.0 | $13.7 | 5.8% |

| Total | $7,493.0 | $6,964.0 | $529.0 | 7.6% |

Share Breakdown by Market Segment

Together, these 10 companies achieved revenue of nearly $7.5BB in 2016; this pie shows how that was spread across the market segments. The figure in parentheses shows how much share they collectively own in these market segments. For instance, 21% of the $7.5BB pertains to spine; together, these 10 companies own ~18% of the overall spine market.

*Other contains CMF, bone growth stim,bracing/soft goods, etc.

Rankings within Segments

We looked at the top ten companies within each market segment. Here, we’ve summarized where these next-tier companies land in the ranks of their peers in AR/ST, spine, joint recon, trauma and orthobiologics.

Arthroscopy / Soft Tissue Repair

| Rank | Company | Revenue |

|---|---|---|

| 1 | Arthrex | $1,540.0 |

Spine

| Rank | Company | Revenue |

|---|---|---|

| 3 | NuVasive | $801.9 |

| 5 | Globus Medical | $536.69 |

Joint Replacement

| Rank | Company | Revenue |

|---|---|---|

| 5 | Aesculap | $401.0 |

| 6 | Wright Medical | $306.6 |

| 7 | Exactech | $222.7 |

| 10 | DJO | $209.7 |

Trauma

| Rank | Company | Revenue |

|---|---|---|

| 5 | Wright Medical | $267.1 |

| 6 | Acumed | $189.4 |

| 8 | Aesculap | $117.9 |

| 10 | Orthofix | $102.7 |

Orthobiologics

| Rank | Company | Revenue |

|---|---|---|

| 4 | Arthrex | $378.0 |

Here, we recap recent initiatives undertaken by the next-tier players to support their growth and strategic priorities.

#6: Arthrex

2016 Revenue: $2.0 billion, +11.7%

The leader in the arthroscopy/soft tissue repair and #4 player in orthobiologics, according to our estimates, Arthrex has signed distribution and product development agreements in those spaces—for instance, renewing its long-term agreement with LifeNet Health to provide allograft implants and instrumentation and explore new applications, like cartilage repair, building on their co-development of alternatives to joint replacement. Arthrex also signed a new multi-year distribution agreement with Vivex Biomedical, following their co-development of BioCartilage, and was selected as CollPlant’s exclusive distributor for Vergenix STR soft tissue repair matrix in Europe, the Middle East, India and certain African countries.

At the company’s Orthopedic Technology & Innovation Forum in 1Q17, Arthrex highlighted Synergy MSK Ultrasound, an in-office imaging platform that supports numerous applications. Synergy is a wireless, handheld system that allows surgeons to display high-resolution images through an app. Arthrex is marketing Synergy MSK globally.

#7: DJO Global

2016 Revenue: $1.1 billion, +3.8%

DJO launched the AltiVate Anatomic Shoulder featuring P2, DJO’s proprietary “porous porous” coating designed to provide superior bone ingrowth. The system features a short humeral stem and a glenoid component with Drop and Go technology, encompassing trilobe features on the peripheral pegs for immediate fixation. The system joins the AltiVate next-gen reverse shoulder, which launched in 3Q15.

Other new shoulder, knee and hip products launched in the last two years have contributed to DJO posting high growth in joint reconstruction, which increased 27.5% in 2016 vs. 2015. In 2014, the company acquired Zimmer’s Discovery Total Elbow for the U.S. market.

DJO fully executed a business transition in 1Q17. The initiative, led by President and CEO Brady Shirley, targets working capital/liquidity improvements; organizational effectiveness; procurement spend optimization; manufacturing, distribution, supply and operations planning; and customer/product profitability improvements (exiting non-strategic and low-margin revenue segments). In announcing 1Q17 earning results, DJO noted plans to replace half of the top 30 leadership roles and numerous leaders in the next level.

#8 NuVasive

2016 Revenue: $962.1 million, +18.6%

NuVasive, which is projected to surpass $1 billion in revenue in 2017, continues to make investments in spine, trauma and pediatrics.

In April, the company launched RELINE Trauma, designed to offer intra-op customization in the treatment of spinal fractures. This is reportedly the first trauma system that can accommodate traditional open, Maximum Access Surgery or hybrid procedures, depending on pathology and patient needs. A dual rack system supports independent lordosis restoration and parallel compression/distraction for ligamentotaxis, and allows procedures to be completed by one surgeon rather than two. The product is integrated with NuVasive’s computer assisted technologies.

Also in April, NuVasive received 510(k) clearance for UNYTE, a bone-compressing system to treat complex/ poorly-healing fractures. Leadership expects that UNYTE could cannibalize ex-fix completely.

Continuing to grow its Japanese business, which it launched in 2013, NuVasive received Japan regulatory approval for instruments used in the eXtreme Lateral Interbody Fusion procedure.

#9 Aesculap

2016 Revenue: $731.1 million, +2.7%

Thus far in 2017, Aesculap has made two announcements related to its spine portfolio, which we estimate at 23% of its total revenue. First, the company offered a warranty program for Plasmapore XP-coated spinal interbody fusion devices, reported to be the first facility risk-share agreement on a titanium-enhanced PEEK interbody in the spine industry to warrant against delamination of a surface enhancement. This news accompanied the launch of the TSpace XP interbody system, which is treated with Plasmapore XP.

Aesculap also presented long-term data from study of its activ-L artificial lumbar disc. Studies indicate that, at five years, activ-L had a protective effect on the progression of degenerative disc disease at adjacent levels in 91.2% of patients. The data reiterated the role of lumbar total disc replacement in delaying the progression of adjacent segment disease.

#10: Wright Medical

2016 Revenue: $690.4 million, +10.2%

In 1Q17, Wright Medical launched Tornier’s BLUEPRINT computer-aided surgical planning software/patient-specific instruments. (Tornier had received FDA 510(k) clearance for the technology in 2015.) BLUEPRINT, along with Wright’s PROPHECY case planning software, helps to better forecast the exact instrumentation and implants needed for ease of case. (Approximately 70% of procedures using Wright’s total ankle are completed with PROPHECY enabling technology.)

Wright Medical and Tornier continued their product line integration following their 2015 merge. In 2016, Tornier legacy hip and knee products were sold to Corin, as Wright sought to exit those markets completely.

#11: Globus Medical

2016 Revenue: $564.0 million, +3.5%

Globus Medical seeks to derive 15% of its overall sales from trauma and robotics by 2020. In 1Q17, the company received CE Mark approval for the Excelsius GPS robotic trajectory guidance and navigation system. GPS supports minimally invasive and open orthopaedic and neurosurgical procedures, with applications in the cervical spine, sacro-ilium, long bones, cranium, etc. The system integrates with the company’s own implants and instruments, and is compatible with pre-op CT, intra-op CT and fluoroscopic imaging modalities.

In May, Globus received a letter from FDA indicating that the company had not sufficiently addressed questions on its 510(k) submission for GPS. Globus expedited a revised filing, and still expects to gain clearance within 2017.

#12: ConMed

2016 Revenue: $422.1 million, -5.1%

ConMed introduced seven new products at AAOS: four that they consider “minor” and three “major.” The latter included the CuffLink Double Row rotator cuff repair system, diamond-like coated shaver blades and the Trinity 3-in-1 camera system, marketed as an economical option for ASCs and emerging markets.

ConMed has not posted positive quarterly growth since 4Q15. A turnaround initiative, launched in 3Q16, includes a revamp of marketing and a focused list of R&D projects and priorities.

In efforts to enhance its portfolio, ConMed purchased MedShape’s ExoShape Anterior Cruciate Ligament fixation system in 3Q17. ExoShape products have been used since 2011 and include femoral and tibial soft tissue fasteners for fixation of soft tissue grafts in reconstruction procedures.

#13: Orthofix

2016 Revenue: $409.8 million, +3.4%

Orthofix launched the JuniOrtho brand to house products and services that treat pediatric orthopaedic and congenital deformities. The company’s pediatric extremity fixation offerings began with launch of a limb lengthener in the early 1980s. Today, its products include the TL HEX TrueLok Hexapod system and Guided Growth plates, available in over 70 countries.

The company also announced FDA Premarket and European CE Mark Approval for its next-generation CervicalStim and SpinalStim bone growth stimulators. U.S. availability will include the Stim onTrack mobile app to support patient engagement and real-time delivery of data to the physician. The Class III devices employ low-level pulsed electromagnetic field (PEMF), designed to activate and augment the body’s natural healing process, in a non-invasive treatment to promote post-op spinal fusion.

Recently, NASS issued first-of-its-kind coverage recommendations for electrical bone growth stimulators, supporting use of PEMF stimulation devices as an adjunct to spinal fusion. Orthofix is conducting IDE clinical trials to collect safety and effectiveness data for the CervicalStim system in treating odontoid fractures and Physio-Stim for knee osteoarthritis.

#14. Exactech

2016 Revenue: $258.8 million, +6.2%

Exactech divested its spine assets to ChoiceSpine earlier this year. Spine represented a small portion of Exactech’s revenue in 2016 (about 3.3%, by our estimates); the transaction allows Exactech to reallocate resources to focus exclusively on joint recon, which grew at 8.6% in 2016 vs. 2015.

Thus far in 2017, Exactech has announced product developments for shoulder, knee and hip. The company received FDA 510(k) clearance to market ExactechGPS shoulder and knee applications, combining pre-op planning with computer-assisted surgery. Exactech also announced the first U.S. surgery with the Equinoxe Preserve humeral stem using the shoulder application, and also completed initial procedures in its U.S. pilot launch for the Truliant Knee and the Alteon HA Femoral Hip Stem. Full U.S. launch for both is slated for 2018.

#15: Acumed

2016 Revenue: $251.7 million, +5.8%

Acumed’s product launches have included expansion of its ankle and elbow lines. The company launched Ankle Plating System 3, comprising seven plate families that span the lateral, medial and posterior malleoli that are used in combination with the Acumed Small Fragment Base Set to treat fractures. Tension Band Pins and Acutrak AcuTwist Compression Screws are also included in the tray.

Acumed also released the Slide-Loc Anatomic Radial Head, a 3-part modular implant with a slide-loading design that does not require a set screw.

Of note, the company named Sharon Wolfington as its President and CEO in 1Q17. Wolfington most recently served as President of DJO Recovery Sciences.

This is not a full list of product clearances and launches by these companies, by far. The products mentioned are meant to highlight the activity that each company has prioritized and announced publicly. We believe that these companies are well-positioned within their niches to continue to experience above-market growth, and could even be targeted for acquisition. We look forward to reviewing, and sharing, second quarter earnings as they’re released in the coming weeks. Until then, remember, THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® provides further detail of each company’s activity within each market segment.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

Acquisitions, divestitures, market entries and exits have shaped portfolios for many of the orthopaedic industry’s top players, in recent years. In this article, we look at such activity from the ten companies that represent #6 through #15 on our list of the largest device companies ranked by revenue: Arthrex, DJO, NuVasive, Aesculap, Wright...

Acquisitions, divestitures, market entries and exits have shaped portfolios for many of the orthopaedic industry’s top players, in recent years. In this article, we look at such activity from the ten companies that represent #6 through #15 on our list of the largest device companies ranked by revenue: Arthrex, DJO, NuVasive, Aesculap, Wright Medical, Globus Medical, ConMed, Orthofix, Exactech and Acumed.

While orthopaedics‘ top five companies—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew and Medtronic—are diversifying across market segments, the ten companies in this group primarily specialize within one or two areas of joint reconstruction, spine, arthroscopy/soft tissue and extremities.

According to our estimates, these companies range in annual revenue from $250 million to $2 billion (See Exhibit 1.), and accounted for nearly $7.5 billion or 15.5% of the orthopaedic industry‘s $48.1 billion in 2016 revenue. New product launches and acquisitions drove all but Aesculap and ConMed to post above-market overall growth of 3.2% in 2016 vs. 2015. This stands in contrast to the growth posted by the top five; of those, only two companies posted growth at or above market in 2016: Stryker at 4.9% and Zimmer Biomet at 3.2%.

Exhibit 1: Performance for Orthopaedic Device Players from #6 to #15 ($Millions)

| Company | 2016 | 2015 | $ Chg | % Chg |

|---|---|---|---|---|

| Arthrex | $2,048.0 | $1,833.1 | $214.9 | 11.7% |

| DJO | $1,155.4 | $1,113.6 | $41.8 | 3.8% |

| NuVasive | $962.1 | $811.1 | $151.0 | 18.6% |

| Aesculap | $731.1 | $711.9 | $19.2 | 2.7% |

| Wright Medical | $690.4 | $626.4 | $64.0 | 10.2% |

| Globus Medical | $564.0 | $544.8 | $19.2 | 3.5% |

| ConMed | $422.1 | $444.9 | ($22.8) | (5.1%) |

| Orthofix | $409.8 | $396.5 | $13.3 | 3.4% |

| Exactech | $258.8 | $243.7 | $15.1 | 6.2% |

| Acumed | $251.7 | $238.0 | $13.7 | 5.8% |

| Total | $7,493.0 | $6,964.0 | $529.0 | 7.6% |

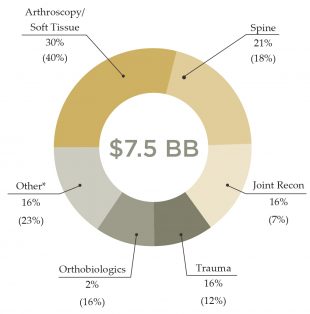

Share Breakdown by Market Segment

Together, these 10 companies achieved revenue of nearly $7.5BB in 2016; this pie shows how that was spread across the market segments. The figure in parentheses shows how much share they collectively own in these market segments. For instance, 21% of the $7.5BB pertains to spine; together, these 10 companies own ~18% of the overall spine market.

*Other contains CMF, bone growth stim,bracing/soft goods, etc.

Rankings within Segments

We looked at the top ten companies within each market segment. Here, we’ve summarized where these next-tier companies land in the ranks of their peers in AR/ST, spine, joint recon, trauma and orthobiologics.

Arthroscopy / Soft Tissue Repair

| Rank | Company | Revenue |

|---|---|---|

| 1 | Arthrex | $1,540.0 |

Spine

| Rank | Company | Revenue |

|---|---|---|

| 3 | NuVasive | $801.9 |

| 5 | Globus Medical | $536.69 |

Joint Replacement

| Rank | Company | Revenue |

|---|---|---|

| 5 | Aesculap | $401.0 |

| 6 | Wright Medical | $306.6 |

| 7 | Exactech | $222.7 |

| 10 | DJO | $209.7 |

Trauma

| Rank | Company | Revenue |

|---|---|---|

| 5 | Wright Medical | $267.1 |

| 6 | Acumed | $189.4 |

| 8 | Aesculap | $117.9 |

| 10 | Orthofix | $102.7 |

Orthobiologics

| Rank | Company | Revenue |

|---|---|---|

| 4 | Arthrex | $378.0 |

Here, we recap recent initiatives undertaken by the next-tier players to support their growth and strategic priorities.

#6: Arthrex

2016 Revenue: $2.0 billion, +11.7%

The leader in the arthroscopy/soft tissue repair and #4 player in orthobiologics, according to our estimates, Arthrex has signed distribution and product development agreements in those spaces—for instance, renewing its long-term agreement with LifeNet Health to provide allograft implants and instrumentation and explore new applications, like cartilage repair, building on their co-development of alternatives to joint replacement. Arthrex also signed a new multi-year distribution agreement with Vivex Biomedical, following their co-development of BioCartilage, and was selected as CollPlant’s exclusive distributor for Vergenix STR soft tissue repair matrix in Europe, the Middle East, India and certain African countries.

At the company’s Orthopedic Technology & Innovation Forum in 1Q17, Arthrex highlighted Synergy MSK Ultrasound, an in-office imaging platform that supports numerous applications. Synergy is a wireless, handheld system that allows surgeons to display high-resolution images through an app. Arthrex is marketing Synergy MSK globally.

#7: DJO Global

2016 Revenue: $1.1 billion, +3.8%

DJO launched the AltiVate Anatomic Shoulder featuring P2, DJO’s proprietary “porous porous” coating designed to provide superior bone ingrowth. The system features a short humeral stem and a glenoid component with Drop and Go technology, encompassing trilobe features on the peripheral pegs for immediate fixation. The system joins the AltiVate next-gen reverse shoulder, which launched in 3Q15.

Other new shoulder, knee and hip products launched in the last two years have contributed to DJO posting high growth in joint reconstruction, which increased 27.5% in 2016 vs. 2015. In 2014, the company acquired Zimmer’s Discovery Total Elbow for the U.S. market.

DJO fully executed a business transition in 1Q17. The initiative, led by President and CEO Brady Shirley, targets working capital/liquidity improvements; organizational effectiveness; procurement spend optimization; manufacturing, distribution, supply and operations planning; and customer/product profitability improvements (exiting non-strategic and low-margin revenue segments). In announcing 1Q17 earning results, DJO noted plans to replace half of the top 30 leadership roles and numerous leaders in the next level.

#8 NuVasive

2016 Revenue: $962.1 million, +18.6%

NuVasive, which is projected to surpass $1 billion in revenue in 2017, continues to make investments in spine, trauma and pediatrics.

In April, the company launched RELINE Trauma, designed to offer intra-op customization in the treatment of spinal fractures. This is reportedly the first trauma system that can accommodate traditional open, Maximum Access Surgery or hybrid procedures, depending on pathology and patient needs. A dual rack system supports independent lordosis restoration and parallel compression/distraction for ligamentotaxis, and allows procedures to be completed by one surgeon rather than two. The product is integrated with NuVasive’s computer assisted technologies.

Also in April, NuVasive received 510(k) clearance for UNYTE, a bone-compressing system to treat complex/ poorly-healing fractures. Leadership expects that UNYTE could cannibalize ex-fix completely.

Continuing to grow its Japanese business, which it launched in 2013, NuVasive received Japan regulatory approval for instruments used in the eXtreme Lateral Interbody Fusion procedure.

#9 Aesculap

2016 Revenue: $731.1 million, +2.7%

Thus far in 2017, Aesculap has made two announcements related to its spine portfolio, which we estimate at 23% of its total revenue. First, the company offered a warranty program for Plasmapore XP-coated spinal interbody fusion devices, reported to be the first facility risk-share agreement on a titanium-enhanced PEEK interbody in the spine industry to warrant against delamination of a surface enhancement. This news accompanied the launch of the TSpace XP interbody system, which is treated with Plasmapore XP.

Aesculap also presented long-term data from study of its activ-L artificial lumbar disc. Studies indicate that, at five years, activ-L had a protective effect on the progression of degenerative disc disease at adjacent levels in 91.2% of patients. The data reiterated the role of lumbar total disc replacement in delaying the progression of adjacent segment disease.

#10: Wright Medical

2016 Revenue: $690.4 million, +10.2%

In 1Q17, Wright Medical launched Tornier’s BLUEPRINT computer-aided surgical planning software/patient-specific instruments. (Tornier had received FDA 510(k) clearance for the technology in 2015.) BLUEPRINT, along with Wright’s PROPHECY case planning software, helps to better forecast the exact instrumentation and implants needed for ease of case. (Approximately 70% of procedures using Wright’s total ankle are completed with PROPHECY enabling technology.)

Wright Medical and Tornier continued their product line integration following their 2015 merge. In 2016, Tornier legacy hip and knee products were sold to Corin, as Wright sought to exit those markets completely.

#11: Globus Medical

2016 Revenue: $564.0 million, +3.5%

Globus Medical seeks to derive 15% of its overall sales from trauma and robotics by 2020. In 1Q17, the company received CE Mark approval for the Excelsius GPS robotic trajectory guidance and navigation system. GPS supports minimally invasive and open orthopaedic and neurosurgical procedures, with applications in the cervical spine, sacro-ilium, long bones, cranium, etc. The system integrates with the company’s own implants and instruments, and is compatible with pre-op CT, intra-op CT and fluoroscopic imaging modalities.

In May, Globus received a letter from FDA indicating that the company had not sufficiently addressed questions on its 510(k) submission for GPS. Globus expedited a revised filing, and still expects to gain clearance within 2017.

#12: ConMed

2016 Revenue: $422.1 million, -5.1%

ConMed introduced seven new products at AAOS: four that they consider “minor” and three “major.” The latter included the CuffLink Double Row rotator cuff repair system, diamond-like coated shaver blades and the Trinity 3-in-1 camera system, marketed as an economical option for ASCs and emerging markets.

ConMed has not posted positive quarterly growth since 4Q15. A turnaround initiative, launched in 3Q16, includes a revamp of marketing and a focused list of R&D projects and priorities.

In efforts to enhance its portfolio, ConMed purchased MedShape’s ExoShape Anterior Cruciate Ligament fixation system in 3Q17. ExoShape products have been used since 2011 and include femoral and tibial soft tissue fasteners for fixation of soft tissue grafts in reconstruction procedures.

#13: Orthofix

2016 Revenue: $409.8 million, +3.4%

Orthofix launched the JuniOrtho brand to house products and services that treat pediatric orthopaedic and congenital deformities. The company’s pediatric extremity fixation offerings began with launch of a limb lengthener in the early 1980s. Today, its products include the TL HEX TrueLok Hexapod system and Guided Growth plates, available in over 70 countries.

The company also announced FDA Premarket and European CE Mark Approval for its next-generation CervicalStim and SpinalStim bone growth stimulators. U.S. availability will include the Stim onTrack mobile app to support patient engagement and real-time delivery of data to the physician. The Class III devices employ low-level pulsed electromagnetic field (PEMF), designed to activate and augment the body’s natural healing process, in a non-invasive treatment to promote post-op spinal fusion.

Recently, NASS issued first-of-its-kind coverage recommendations for electrical bone growth stimulators, supporting use of PEMF stimulation devices as an adjunct to spinal fusion. Orthofix is conducting IDE clinical trials to collect safety and effectiveness data for the CervicalStim system in treating odontoid fractures and Physio-Stim for knee osteoarthritis.

#14. Exactech

2016 Revenue: $258.8 million, +6.2%

Exactech divested its spine assets to ChoiceSpine earlier this year. Spine represented a small portion of Exactech’s revenue in 2016 (about 3.3%, by our estimates); the transaction allows Exactech to reallocate resources to focus exclusively on joint recon, which grew at 8.6% in 2016 vs. 2015.

Thus far in 2017, Exactech has announced product developments for shoulder, knee and hip. The company received FDA 510(k) clearance to market ExactechGPS shoulder and knee applications, combining pre-op planning with computer-assisted surgery. Exactech also announced the first U.S. surgery with the Equinoxe Preserve humeral stem using the shoulder application, and also completed initial procedures in its U.S. pilot launch for the Truliant Knee and the Alteon HA Femoral Hip Stem. Full U.S. launch for both is slated for 2018.

#15: Acumed

2016 Revenue: $251.7 million, +5.8%

Acumed’s product launches have included expansion of its ankle and elbow lines. The company launched Ankle Plating System 3, comprising seven plate families that span the lateral, medial and posterior malleoli that are used in combination with the Acumed Small Fragment Base Set to treat fractures. Tension Band Pins and Acutrak AcuTwist Compression Screws are also included in the tray.

Acumed also released the Slide-Loc Anatomic Radial Head, a 3-part modular implant with a slide-loading design that does not require a set screw.

Of note, the company named Sharon Wolfington as its President and CEO in 1Q17. Wolfington most recently served as President of DJO Recovery Sciences.

This is not a full list of product clearances and launches by these companies, by far. The products mentioned are meant to highlight the activity that each company has prioritized and announced publicly. We believe that these companies are well-positioned within their niches to continue to experience above-market growth, and could even be targeted for acquisition. We look forward to reviewing, and sharing, second quarter earnings as they’re released in the coming weeks. Until then, remember, THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® provides further detail of each company’s activity within each market segment.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.