Copy to clipboard

Copy to clipboard

Historically, orthopedic and spine device vendors have focused largely on the surgeon as a primary customer. From the hospital’s perspective, vendors catered to the physician while the hospital paid the bill, even as reimbursement declined. While some vendors still cling to this model, progressive device companies are starting to understand the limitations of traditional marketing and sales in favor of more holistic approaches to product development and sales. During this highly dynamic time, especially with the profound effect of COVID-19, there are opportunities to better understand and leverage the knowledge of providers. This behavior allows vendors to serve customers more effectively by augmenting core sales practices with account management tools.

This column offers commentary on three developments that will assist vendors in growing sales and supporting customers.

Vendor Engagement

Transactional sales to strategic account management

In the mid-term, providers will focus on reducing costs by driving the management of the payment and accurately understanding and managing costs, with devices often being a first-line cost savings target. (In current parlance, the catchall term “healthcare providers” may include hospitals, health systems, physicians, specialty practices and other healthcare professionals and services.) Although fee-for-service reimbursement remains the dominant model, payment is inexorably moving to newer models. Other quality and cost containment initiatives (physician employment, bundled payment, gainsharing, co-management and others) that impact physician reimbursement are challenging device brand loyalty and years-long relationships with vendors. This could shift device preferences in favor of competitive products that will bring greater value, lower price or patient benefit. Proactive vendor alignment with these collaborative efforts in managing cost drivers can result in novel approaches and avoidance of commoditization of implants with the attendant price pressure.

A Strategic Sourcing professional recently suggested that vendors and suppliers need to “wear the buyer’s hat” as an approach steeped in customer knowledge to strategically align selling with buying. Additionally, thriving will require that vendors access and collaborate across multiple departments and functions – administrative, finance, operations, clinical and supply chain.

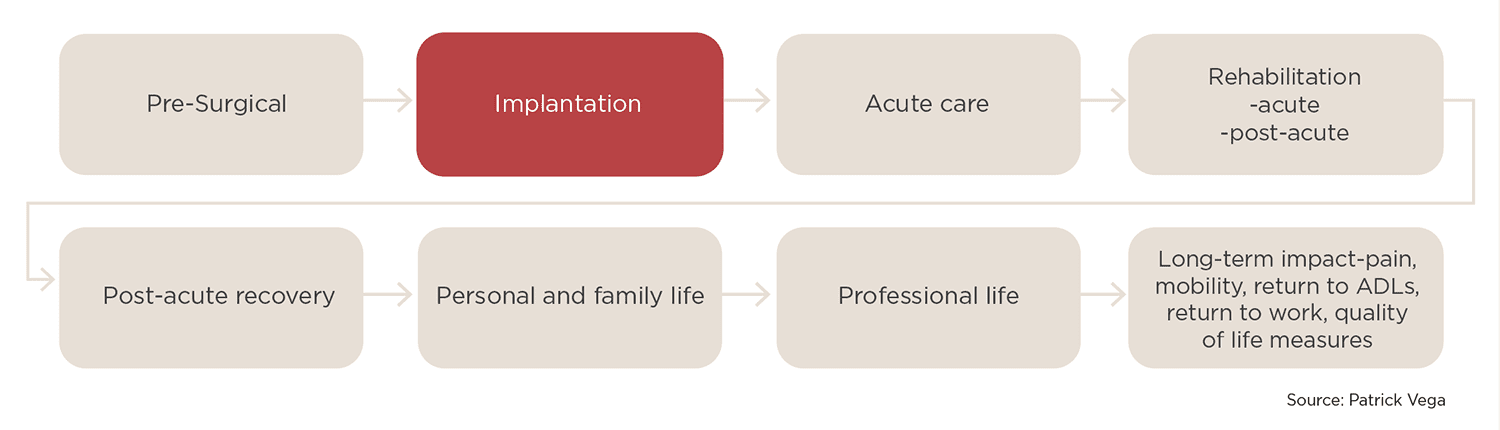

Exhibit 1 illustrates the traditional model of selling to the physician and purchasing at the time of implantation, with minimal focus on the broader context of care and product lifecycle across the provider-patient continuum. Such a focus limits both the vendor perspective and opportunities to engage more broadly with other key hospital and patient stakeholders.

Exhibit 1: Traditional Vendor Selling Model (Click to enlarge)

By engaging before, during and after the sale, vendors may be able to shape use of their products according to provider needs, achieving more influence on brand choice, creating greater value and support sustained brand loyalty. This type of partnership can result in supporting not only a sales transaction, but also ongoing strategic dialogue with hospital leadership.

Hospital Purchasing Scale

Transition from free-standing hospitals and small systems to the consolidation of multiple hospitals into Integrated Delivery Networks, impacting Supply Chain processes

In the pursuit of scale and market share, hospitals, community-based services and practices have merged into multisite, multiservice organizational entities over larger geographies, often called Integrated Delivery Networks (IDNs). A vendor’s knowledge of this transforming provider environment is often limited to typical touchpoints: physicians, purchasing and the supply chain.

IDN emergence has many implications for vendors: increasingly centralized decision-making on purchasing, less influence among physicians, sophisticated and data-supported evaluation of products, a heightened focus on demonstrable quality and the need to understand and navigate health systems beyond sales. Vendor success will require their understanding and nimble compliance with evolving Value Analysis processes and requirements.

Physician Data

Physician access to comparative cost, quality, and performance data

In the broadest sense, hospital/physician alignment means that the core elements of healthcare delivery; clinical, financial, outcomes and operations are moving away from hospitals and physicians working independently, and often at cross purposes to one another, toward greater collaboration. Fueled by data insights and greater incentives, physicians are eagerly taking greater ownership in managing costs and quality. With implantables sometimes representing a large percentage of surgical cost, devices are a prime target for scrutiny. Further, in many of the reimbursement models already in place or being piloted, physician reimbursement will be impacted by selection of devices. It is reasonable to anticipate that physician’s loyalties to brand will be, at a minimum, stressed if not abandoned in favor of products that are clinically comparable and less costly and improve their compensation.

Vendor Opportunity

As hospitals, health systems and their associated providers live in a more complex environment, traditional approaches to selling products and services have become less effective. Vendors who endeavor to both understand the provider continuum and meaningfully invest in a partnership with providers can be rewarded with market share growth, reciprocal value and more permanence in their relations with providers and IDNs. With hospitals, physicians and payors increasingly focused on collaboration, cost-containment and preparing for new reimbursement models, what should device companies be doing?

To recap, vendors should aspire to:

- Deliberately and assertively focus on an expanded customer base of buyers and decision makers,

- Deeply understand hospital systems of care and how a vendor’s product “lives” in the provider and patient environments,

- Seek a seat at the “strategy table” with hospital leadership; solicit and respond to opportunities to increase collaboration,

- Offer demonstrably differentiated products with meaningful outcomes data,

- Achieve conversance in all reimbursement models: fee-for-service, bundled payment, capitation and risk,

- Pursue collaborative, long-term relationships with IDNs and physicians.

While for some readers these recommendations may seem vague, the best and longest lasting relationships often begin with only limited understanding. However, with initiative, intentionality and a commitment to collaborate, such relationships can lead to sustained partnerships that are beneficial to vendor, hospital and patients.

Historically, orthopedic and spine device vendors have focused largely on the surgeon as a primary customer. From the hospital’s perspective, vendors catered to the physician while the hospital paid the bill, even as reimbursement declined. While some vendors still cling to this model, progressive device companies are starting to understand the...

Historically, orthopedic and spine device vendors have focused largely on the surgeon as a primary customer. From the hospital’s perspective, vendors catered to the physician while the hospital paid the bill, even as reimbursement declined. While some vendors still cling to this model, progressive device companies are starting to understand the limitations of traditional marketing and sales in favor of more holistic approaches to product development and sales. During this highly dynamic time, especially with the profound effect of COVID-19, there are opportunities to better understand and leverage the knowledge of providers. This behavior allows vendors to serve customers more effectively by augmenting core sales practices with account management tools.

This column offers commentary on three developments that will assist vendors in growing sales and supporting customers.

Vendor Engagement

Transactional sales to strategic account management

In the mid-term, providers will focus on reducing costs by driving the management of the payment and accurately understanding and managing costs, with devices often being a first-line cost savings target. (In current parlance, the catchall term “healthcare providers” may include hospitals, health systems, physicians, specialty practices and other healthcare professionals and services.) Although fee-for-service reimbursement remains the dominant model, payment is inexorably moving to newer models. Other quality and cost containment initiatives (physician employment, bundled payment, gainsharing, co-management and others) that impact physician reimbursement are challenging device brand loyalty and years-long relationships with vendors. This could shift device preferences in favor of competitive products that will bring greater value, lower price or patient benefit. Proactive vendor alignment with these collaborative efforts in managing cost drivers can result in novel approaches and avoidance of commoditization of implants with the attendant price pressure.

A Strategic Sourcing professional recently suggested that vendors and suppliers need to “wear the buyer’s hat” as an approach steeped in customer knowledge to strategically align selling with buying. Additionally, thriving will require that vendors access and collaborate across multiple departments and functions – administrative, finance, operations, clinical and supply chain.

Exhibit 1 illustrates the traditional model of selling to the physician and purchasing at the time of implantation, with minimal focus on the broader context of care and product lifecycle across the provider-patient continuum. Such a focus limits both the vendor perspective and opportunities to engage more broadly with other key hospital and patient stakeholders.

Exhibit 1: Traditional Vendor Selling Model (Click to enlarge)

By engaging before, during and after the sale, vendors may be able to shape use of their products according to provider needs, achieving more influence on brand choice, creating greater value and support sustained brand loyalty. This type of partnership can result in supporting not only a sales transaction, but also ongoing strategic dialogue with hospital leadership.

Hospital Purchasing Scale

Transition from free-standing hospitals and small systems to the consolidation of multiple hospitals into Integrated Delivery Networks, impacting Supply Chain processes

In the pursuit of scale and market share, hospitals, community-based services and practices have merged into multisite, multiservice organizational entities over larger geographies, often called Integrated Delivery Networks (IDNs). A vendor’s knowledge of this transforming provider environment is often limited to typical touchpoints: physicians, purchasing and the supply chain.

IDN emergence has many implications for vendors: increasingly centralized decision-making on purchasing, less influence among physicians, sophisticated and data-supported evaluation of products, a heightened focus on demonstrable quality and the need to understand and navigate health systems beyond sales. Vendor success will require their understanding and nimble compliance with evolving Value Analysis processes and requirements.

Physician Data

Physician access to comparative cost, quality, and performance data

In the broadest sense, hospital/physician alignment means that the core elements of healthcare delivery; clinical, financial, outcomes and operations are moving away from hospitals and physicians working independently, and often at cross purposes to one another, toward greater collaboration. Fueled by data insights and greater incentives, physicians are eagerly taking greater ownership in managing costs and quality. With implantables sometimes representing a large percentage of surgical cost, devices are a prime target for scrutiny. Further, in many of the reimbursement models already in place or being piloted, physician reimbursement will be impacted by selection of devices. It is reasonable to anticipate that physician’s loyalties to brand will be, at a minimum, stressed if not abandoned in favor of products that are clinically comparable and less costly and improve their compensation.

Vendor Opportunity

As hospitals, health systems and their associated providers live in a more complex environment, traditional approaches to selling products and services have become less effective. Vendors who endeavor to both understand the provider continuum and meaningfully invest in a partnership with providers can be rewarded with market share growth, reciprocal value and more permanence in their relations with providers and IDNs. With hospitals, physicians and payors increasingly focused on collaboration, cost-containment and preparing for new reimbursement models, what should device companies be doing?

To recap, vendors should aspire to:

- Deliberately and assertively focus on an expanded customer base of buyers and decision makers,

- Deeply understand hospital systems of care and how a vendor’s product “lives” in the provider and patient environments,

- Seek a seat at the “strategy table” with hospital leadership; solicit and respond to opportunities to increase collaboration,

- Offer demonstrably differentiated products with meaningful outcomes data,

- Achieve conversance in all reimbursement models: fee-for-service, bundled payment, capitation and risk,

- Pursue collaborative, long-term relationships with IDNs and physicians.

While for some readers these recommendations may seem vague, the best and longest lasting relationships often begin with only limited understanding. However, with initiative, intentionality and a commitment to collaborate, such relationships can lead to sustained partnerships that are beneficial to vendor, hospital and patients.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

PV

Patrick Vega is Consulting Director for Vizient’s Excelerate and PPI Orthopedics. Mr. Vega consults to member hospitals, health systems and physicians in musculoskeletal services with a focus on high-value care by aligning cost, quality and performance.