Copy to clipboard

Copy to clipboard

The migration of inpatient procedures to the ambulatory setting may be likened to the western expansion of the United States — fraught with obstacles but ultimately inevitable. Since the early 1970s, a steady progression of procedures has exited inpatient settings led by pioneers in the space. Prepared orthopedic companies can influence ambulatory procedure expansion and shoulder exploration of when and where these procedures will boom. To do so, they must stay abreast of which orthopedic procedures will move and how to support them.

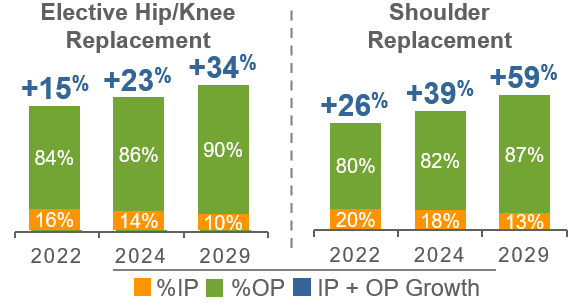

Much has been written in recent years about total hip and total knee arthroplasty procedures exiting inpatient settings. This migration is expected to continue, according to Sg2, a Vizient company. Figure 1 below illustrates the rate at which the shift is predicted to occur for joint replacement surgeries.

Figure 1: Elective Hip/Knee Replacement and Shoulder Replacement

The Medicare Inpatient Only (IPO) procedure list qualifies the site of service by emphasizing patient safety and quality outcomes, and it is considered a standard for what can and cannot be performed on an outpatient basis. The IPO list, along with the addenda and fee schedules for the Outpatient Prospective Payment System (OPPS) covering hospital outpatient departments (HOPD) and the Ambulatory Surgery Center (ASC) system, can provide insight into the remaining procedures with opportunity for future Medicare beneficiary growth in ambulatory settings. Though many of the more complex orthopedic surgeries have moved off the IPO list and are now allowed in an HOPD, a few key procedures are not covered by Medicare when performed in an ASC. At the forefront of these procedures are opportunities in shoulder and ankle arthroplasty, as well as spinal procedures — especially fusions.

Shoulder, Ankle and Spine Surgeries

Two shoulder arthroplasty procedures stand out among large joint replacement procedures that are not yet Medicare-approved for ASCs: total joint and hemiarthroplasty. Though removed from the IPO list, these procedures have yet to be added for Medicare coverage in an ASC. Nonetheless, ready surgeons are currently performing these procedures safely in ASCs when reimbursed by commercial payors.

Hemiarthroplasty “resurfacing” techniques involve implanting humeral (arm bone) head caps without a humeral stem. Unlike hip resurfacing, which has a specific Common Procedural Terminology (CPT) code, shoulder resurfacing does not. Coding guidance recommends reporting the procedure as an “unlisted procedure of the shoulder” rather than using the shoulder hemiarthroplasty CPT code. This guidance can present a challenge for facilities as reimbursement contracts tend to pay unfavorably for “unlisted” procedure types. While shoulder resurfacing is a suitable procedure for the HOPD and ASC setting, further coding development is required for these procedures to be accurately reported and reimbursed through governmental and commercial payor pathways. Until then, surgeons may be reluctant to perform these procedures in ASCs.

Like shoulder arthroplasty, ankle arthroplasty was removed from the IPO list. It is reimbursed in the HOPD setting, but not in the ASC. While ankle replacement is not as commonly performed as other joint replacement surgeries, the number of procedures is growing and more surgeons and device companies are entering the specialized foot and ankle space. We envision Medicare ultimately approving this procedure in the ASC, providing Medicare beneficiaries with the same high-quality, lower-cost care experienced from other ambulatory arthroplasty procedures.

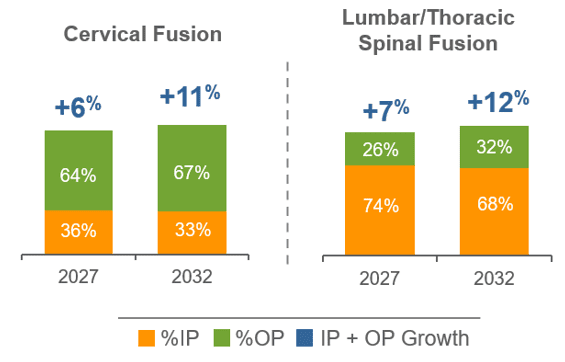

The next developing procedural territory is in spinal surgery, specifically lumbar fusion. While many spine procedures remain on the Medicare IPO list, commercial payors may elect to allow these procedures in an ASC setting. Those currently performed on an outpatient basis range from simple decompressions to more complex procedures, such as anterior lumbar interbody fusion. In 2023, one spine procedure was removed from the IPO list, which allows an “additional level” of posterior lumbar fusion using an interbody technique to be performed in the HOPD setting. This procedure was added to the OPPS list of covered procedures; however, its Medicare coverage status has not offered added reimbursement beyond the initial fusion level.

The graph below shows Sg2’s predictions for the growth of spine surgeries in the outpatient setting.

Figure 2: Cervical Fusion and Lumbar/Thoracic Spinal Fusion

With steady growth in lumbar fusion procedures, Medicare has limited ASC reimbursement to strictly one procedure type: posterior/posterolateral fusion with instrumentation (implanting pedicle screws and rods). Techniques using commonly implanted interbody devices or a combination procedure using both instrumentation and interbody devices are not covered in ASCs. Some surgeons may find this limiting if their preferred fusion technique incorporates interbody devices. Additional procedures yet to be reimbursed in an ASC that are reimbursed in an HOPD are decompression surgeries during which more than two vertebral segments are addressed. However, one- and two-level decompressions are paid in the ASC setting. Given the success of minimally invasive decompressions, we expect the addition of more levels to be a future opportunity.

Coding, Pricing and Budling: What Vendors Should Know

In my experience as a musculoskeletal ASC administrator, there are a few areas that savvy device companies can support to aid in the procedure migration. First, having insight into applicable procedure coding to aid facilities with financial analysis is crucial. Vendors that perform better than others in this area publish documents with specific diagnosis and procedural coding to assist in reporting the use of their technology.

The second initiative is understanding the cost of devices in relation to reimbursement and ensuring ample margin for facilities. Most ASCs are for-profit entities with physician owners. Effective vendors will price products competitively with a “win-win” strategy for the center and the surgeon. One consideration for a successful strategy is to product bundle at a case rate rather than line-item charges. This approach simplifies pro forma analysis and shares risk in performing new procedures. It also leads to joint success in growth and is an opportunity to improve efficiencies. Operationally, successful orthopedic companies will smooth out and enhance the migration into new procedures by:

- Participating in facility partnership through new procedure marketing and surgeon recruitment

- Reducing barriers to entry (available and affordable technology, documented/shared program success from like facilities)

- Providing early education to facility staff in all areas of case planning and performance (hands-on clinical training, coding and billing support, patient educational and procedural resources)

- Streamlining instrumentation and implants (early delivery, modeled for smaller spaces and faster pace settings)

To predict where procedures will progress to ambulatory settings, one must consider the previous migration pattern of orthopedic procedures. Markets with pioneering surgeons have experienced the migration pattern to ASCs for years, while other markets may lag behind the adoption curve. Bustling surgery centers already well versed in procedural safety and proficiency will likely be the first to perform more expansive procedures. Markets lacking ASC penetration may also experience rapid growth. However, it takes time to build out new programs and gain efficiency. New ASCs tend to begin with basic surgeries before venturing into more complex ones.

ASCs with the capacity for extended stay may have been the first to stake claim in complex procedures. The ability to keep a patient overnight or within a multi-day convalescent care environment allows for greater accommodation where procedures may require extended recovery for pain management or initiation of physical medicine. Individual state licensing will help predict opportunities for procedural expansion where extended stay capacity is allowed. Facilities leveraging this capacity are better poised to push the boundaries in procedure or patient complexity compared to those limited to short-stay operations.

Lastly, determining precisely when the migration of the above procedures will occur is difficult for several reasons. Previous Medicare consideration of eliminating the IPO list was unsuccessful, while the unpredicted tailwind of the pandemic helped push procedure migration forward. Fortunately, the above arthroplasty and fusion procedures are already being performed in ASCs when covered by commercial insurance. This offers greater insight into the safety, procedural efficiency and cost effectiveness Medicare could benefit from if the program removed restrictions and allowed practitioners to determine the optimal venue based on patient needs.

The transitional success and burgeoning momentum for hip and knee procedures will likely lead to quicker outpatient acceptance of shoulder and ankle arthroplasty and spine procedures. For now, the timing of the shift is indeterminable. Perhaps the best roadmap we can provide is, “Coming soon to a (n operating) theater near you.”

Figure 1: Analysis excludes 0–17 age group. Ortho surgery includes ortho service line, IP and OP major therapeutic procedures group, and arthroscopy procedures. Elective hip/knee replacement includes Osteoarthritis CARE Family, IP/OP primary hip/knee replacement. Shoulder replacement includes Osteoarthritis and Musculoskeletal Injury – Shoulder/Elbow/Upper Arm CARE Families only.

Sources: Impact of Change®, 2022; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP) 2019. Agency for Healthcare Research and Quality, Rockville, MD; Proprietary Sg2 All-Payer Claims Data Set, 2019; The following 2019 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2022; Sg2 Analysis, 2022.

Figure 2: Analysis excludes 0–17 age group. Spine includes spine service line, IP and OP major therapeutic procedures groups only.

Sources: Impact of Change®, 2022; Proprietary Sg2 All-Payer Claims Data Set, 2019; The following 2019 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2022; Sg2 Analysis, 2022.

The migration of inpatient procedures to the ambulatory setting may be likened to the western expansion of the United States — fraught with obstacles but ultimately inevitable. Since the early 1970s, a steady progression of procedures has exited inpatient settings led by pioneers in the space. Prepared orthopedic companies can influence...

The migration of inpatient procedures to the ambulatory setting may be likened to the western expansion of the United States — fraught with obstacles but ultimately inevitable. Since the early 1970s, a steady progression of procedures has exited inpatient settings led by pioneers in the space. Prepared orthopedic companies can influence ambulatory procedure expansion and shoulder exploration of when and where these procedures will boom. To do so, they must stay abreast of which orthopedic procedures will move and how to support them.

Much has been written in recent years about total hip and total knee arthroplasty procedures exiting inpatient settings. This migration is expected to continue, according to Sg2, a Vizient company. Figure 1 below illustrates the rate at which the shift is predicted to occur for joint replacement surgeries.

Figure 1: Elective Hip/Knee Replacement and Shoulder Replacement

The Medicare Inpatient Only (IPO) procedure list qualifies the site of service by emphasizing patient safety and quality outcomes, and it is considered a standard for what can and cannot be performed on an outpatient basis. The IPO list, along with the addenda and fee schedules for the Outpatient Prospective Payment System (OPPS) covering hospital outpatient departments (HOPD) and the Ambulatory Surgery Center (ASC) system, can provide insight into the remaining procedures with opportunity for future Medicare beneficiary growth in ambulatory settings. Though many of the more complex orthopedic surgeries have moved off the IPO list and are now allowed in an HOPD, a few key procedures are not covered by Medicare when performed in an ASC. At the forefront of these procedures are opportunities in shoulder and ankle arthroplasty, as well as spinal procedures — especially fusions.

Shoulder, Ankle and Spine Surgeries

Two shoulder arthroplasty procedures stand out among large joint replacement procedures that are not yet Medicare-approved for ASCs: total joint and hemiarthroplasty. Though removed from the IPO list, these procedures have yet to be added for Medicare coverage in an ASC. Nonetheless, ready surgeons are currently performing these procedures safely in ASCs when reimbursed by commercial payors.

Hemiarthroplasty “resurfacing” techniques involve implanting humeral (arm bone) head caps without a humeral stem. Unlike hip resurfacing, which has a specific Common Procedural Terminology (CPT) code, shoulder resurfacing does not. Coding guidance recommends reporting the procedure as an “unlisted procedure of the shoulder” rather than using the shoulder hemiarthroplasty CPT code. This guidance can present a challenge for facilities as reimbursement contracts tend to pay unfavorably for “unlisted” procedure types. While shoulder resurfacing is a suitable procedure for the HOPD and ASC setting, further coding development is required for these procedures to be accurately reported and reimbursed through governmental and commercial payor pathways. Until then, surgeons may be reluctant to perform these procedures in ASCs.

Like shoulder arthroplasty, ankle arthroplasty was removed from the IPO list. It is reimbursed in the HOPD setting, but not in the ASC. While ankle replacement is not as commonly performed as other joint replacement surgeries, the number of procedures is growing and more surgeons and device companies are entering the specialized foot and ankle space. We envision Medicare ultimately approving this procedure in the ASC, providing Medicare beneficiaries with the same high-quality, lower-cost care experienced from other ambulatory arthroplasty procedures.

The next developing procedural territory is in spinal surgery, specifically lumbar fusion. While many spine procedures remain on the Medicare IPO list, commercial payors may elect to allow these procedures in an ASC setting. Those currently performed on an outpatient basis range from simple decompressions to more complex procedures, such as anterior lumbar interbody fusion. In 2023, one spine procedure was removed from the IPO list, which allows an “additional level” of posterior lumbar fusion using an interbody technique to be performed in the HOPD setting. This procedure was added to the OPPS list of covered procedures; however, its Medicare coverage status has not offered added reimbursement beyond the initial fusion level.

The graph below shows Sg2’s predictions for the growth of spine surgeries in the outpatient setting.

Figure 2: Cervical Fusion and Lumbar/Thoracic Spinal Fusion

With steady growth in lumbar fusion procedures, Medicare has limited ASC reimbursement to strictly one procedure type: posterior/posterolateral fusion with instrumentation (implanting pedicle screws and rods). Techniques using commonly implanted interbody devices or a combination procedure using both instrumentation and interbody devices are not covered in ASCs. Some surgeons may find this limiting if their preferred fusion technique incorporates interbody devices. Additional procedures yet to be reimbursed in an ASC that are reimbursed in an HOPD are decompression surgeries during which more than two vertebral segments are addressed. However, one- and two-level decompressions are paid in the ASC setting. Given the success of minimally invasive decompressions, we expect the addition of more levels to be a future opportunity.

Coding, Pricing and Budling: What Vendors Should Know

In my experience as a musculoskeletal ASC administrator, there are a few areas that savvy device companies can support to aid in the procedure migration. First, having insight into applicable procedure coding to aid facilities with financial analysis is crucial. Vendors that perform better than others in this area publish documents with specific diagnosis and procedural coding to assist in reporting the use of their technology.

The second initiative is understanding the cost of devices in relation to reimbursement and ensuring ample margin for facilities. Most ASCs are for-profit entities with physician owners. Effective vendors will price products competitively with a “win-win” strategy for the center and the surgeon. One consideration for a successful strategy is to product bundle at a case rate rather than line-item charges. This approach simplifies pro forma analysis and shares risk in performing new procedures. It also leads to joint success in growth and is an opportunity to improve efficiencies. Operationally, successful orthopedic companies will smooth out and enhance the migration into new procedures by:

- Participating in facility partnership through new procedure marketing and surgeon recruitment

- Reducing barriers to entry (available and affordable technology, documented/shared program success from like facilities)

- Providing early education to facility staff in all areas of case planning and performance (hands-on clinical training, coding and billing support, patient educational and procedural resources)

- Streamlining instrumentation and implants (early delivery, modeled for smaller spaces and faster pace settings)

To predict where procedures will progress to ambulatory settings, one must consider the previous migration pattern of orthopedic procedures. Markets with pioneering surgeons have experienced the migration pattern to ASCs for years, while other markets may lag behind the adoption curve. Bustling surgery centers already well versed in procedural safety and proficiency will likely be the first to perform more expansive procedures. Markets lacking ASC penetration may also experience rapid growth. However, it takes time to build out new programs and gain efficiency. New ASCs tend to begin with basic surgeries before venturing into more complex ones.

ASCs with the capacity for extended stay may have been the first to stake claim in complex procedures. The ability to keep a patient overnight or within a multi-day convalescent care environment allows for greater accommodation where procedures may require extended recovery for pain management or initiation of physical medicine. Individual state licensing will help predict opportunities for procedural expansion where extended stay capacity is allowed. Facilities leveraging this capacity are better poised to push the boundaries in procedure or patient complexity compared to those limited to short-stay operations.

Lastly, determining precisely when the migration of the above procedures will occur is difficult for several reasons. Previous Medicare consideration of eliminating the IPO list was unsuccessful, while the unpredicted tailwind of the pandemic helped push procedure migration forward. Fortunately, the above arthroplasty and fusion procedures are already being performed in ASCs when covered by commercial insurance. This offers greater insight into the safety, procedural efficiency and cost effectiveness Medicare could benefit from if the program removed restrictions and allowed practitioners to determine the optimal venue based on patient needs.

The transitional success and burgeoning momentum for hip and knee procedures will likely lead to quicker outpatient acceptance of shoulder and ankle arthroplasty and spine procedures. For now, the timing of the shift is indeterminable. Perhaps the best roadmap we can provide is, “Coming soon to a (n operating) theater near you.”

Figure 1: Analysis excludes 0–17 age group. Ortho surgery includes ortho service line, IP and OP major therapeutic procedures group, and arthroscopy procedures. Elective hip/knee replacement includes Osteoarthritis CARE Family, IP/OP primary hip/knee replacement. Shoulder replacement includes Osteoarthritis and Musculoskeletal Injury – Shoulder/Elbow/Upper Arm CARE Families only.

Sources: Impact of Change®, 2022; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP) 2019. Agency for Healthcare Research and Quality, Rockville, MD; Proprietary Sg2 All-Payer Claims Data Set, 2019; The following 2019 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2022; Sg2 Analysis, 2022.

Figure 2: Analysis excludes 0–17 age group. Spine includes spine service line, IP and OP major therapeutic procedures groups only.

Sources: Impact of Change®, 2022; Proprietary Sg2 All-Payer Claims Data Set, 2019; The following 2019 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2022; Sg2 Analysis, 2022.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ER

Ernie Robles RN, BS, consulting director for Vizient, has 35 years of experience in clinical, revenue cycle and operational roles. As an experienced healthcare administrator and clinician, he has served in both acute and non-acute settings.