Copy to clipboard

Copy to clipboard

Orthopedic and spine care continue to evolve, with accelerated movement of procedures from traditional hospital-based settings to ambulatory facilities. Forward-thinking providers, along with orthopedic and spine product companies, are beginning to invest in resources to understand, predict and capitalize on these changes.

Clinical and technical advances, coupled with evidence-based patient selection criteria, now make a growing pool of patients who are viable candidates for outpatient surgery. Many forces come into play, however, when considering market dynamics and predicting future potential changes.

Centers for Medicare & Medicaid Services Updates

Ongoing changes to site-of-care restrictions by the Centers for Medicare & Medicaid Services (CMS) are a key driver in the outpatient shift of orthopedic and spine procedures.

In recent years, CMS removed key musculoskeletal services from the inpatient-only list, including total knee arthroplasty in 2018, total hip arthroplasty in 2020 and partial hip and shoulder arthroplasties in 2021. Meanwhile, CMS continues to expand the ambulatory surgery center (ASC)-covered procedure list, including total knee arthroplasty in 2020 and total hip arthroplasty in 2021.[1]

In addition to its gradual removal of site-of-care restrictions, CMS recently implemented additional prior authorization requirements for cervical spinal fusions performed in hospital outpatient departments.[2] These authorizations are not required for ASCs.

Payer Pressures and the Pandemic Effect

Beyond CMS changes, commercial payers continue to expand the scope and use of their site-of-care medical necessity reviews to shift cases to ambulatory sites outside hospital campuses. For example, UnitedHealthcare has committed that more than 55% of member outpatient surgeries and radiology services will be delivered at high-quality, cost-efficient sites of care by 2030. This move, which highlights their intentions to direct more patients to ASCs,[3] makes strategic sense when ASCs can offer surgical procedures for 25% to 40% less cost than hospitals.[4]

Pandemic-fueled efforts to reduce risk and lengths of stay accelerated the outpatient and ambulatory shift substantially. Analysis by Sg2®, a Vizient company specializing in market research and intelligence, of hospital data from Strata Decision Technology, found that 62% of primary knee replacements were performed as outpatient procedures in the fourth quarter of 2020.[5] Similarly, Sg2 analysis of claims data found that the portion of commercially insured, inpatient, nonfracture primary hip replacements dropped from 77% in the fourth quarter of 2019 to 35% in the fourth quarter of 2020, with 50% performed in a hospital outpatient department and 15% performed in an ASC.[6]

Outpatient Growth Rates

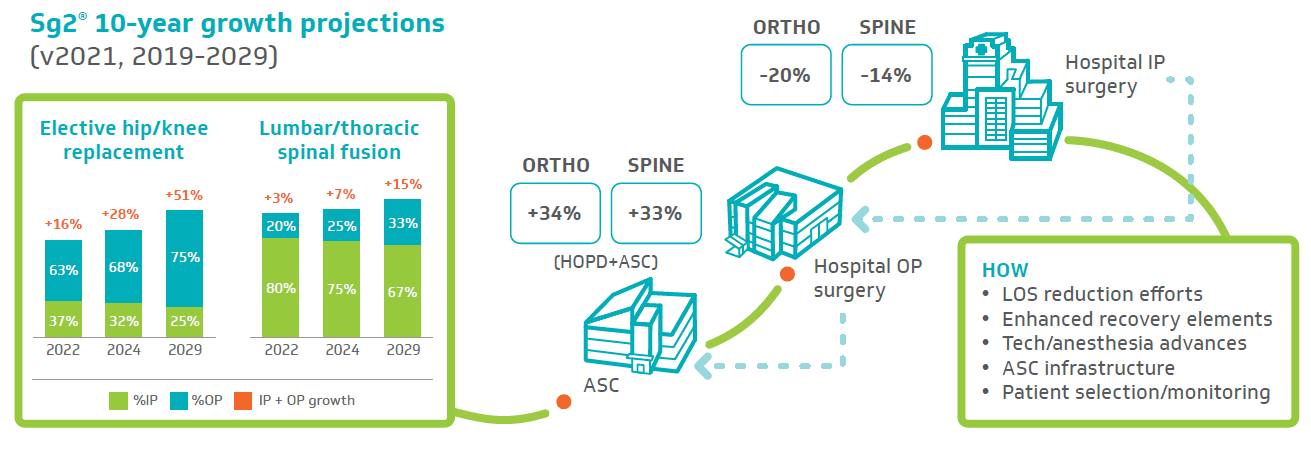

The 2021 Impact of Change® forecast from Sg2 projects strong growth in outpatient procedures through 2029 — with anticipated outpatient growth of more than 30% for orthopedics and spine. (See Figure 1.) Concurrently, the inpatient procedures forecast predicts a 20% drop in orthopedics and a 14% drop in spine. For joint replacement, the Impact of Change forecast projects that 63% of nonfracture primary knee and hip replacements in 2022 will occur in outpatient settings.[7]

Figure 1. Orthopedic and Spine Surgery: Policy changes, COVID-19 pandemic and economic pressures accelerate HOPD/ASC shift (click to enlarge)

While providers and analysts expect surgical volume to grow in both orthopedics and spine, the transformation in how and where providers deliver care will affect clinical, operational and financial components for health care organizations, service groups and vendors.

Vendor Opportunity

While providers launch programs and facilities to meet patient needs, medical device vendors also have an opportunity to transition their offerings and pricing structures for customers. In a highly competitive space, the shift in sites of care may offer a window for both current and new players to capture additional market share. The pressure to reduce costs flows downstream — from patient to provider to device company. Business sustainability and growth will require new strategies.

New Ambulatory Vendor Strategies

Traditionally, device company sales representatives focused their marketing efforts primarily on surgeons. With the emergence of integrated delivery networks and supply chain’s refined role as a more strategic department, providers and decision-makers have a wider scope of influence. Vendor sales teams will need to deploy an enhanced skill set (more akin to account management) to serve as resources for these customers.

Price structure differences among facilities, compounded by reimbursement variance, may erode vendor inpatient pricing. This will likely require new product development, pricing model revisions and redesign of sales strategies across the full spectrum of treatment sites.

While addressing new stakeholders, influencers and cost pressures, orthopedic companies will look to new aggregated data for ambulatory surgery center trends. This analysis is market-specific, even hyperlocalized, due to regulatory, competitive and ownership influences.

Refining the ASC Sales Approach

Many orthopedic and spine companies have already deployed focused teams to evaluate opportunities to partner locally and create infrastructures to support and advance the ASC business segment. As previously noted, vendors are working to expand and complement traditional sales representative roles to incorporate more strategic account management.

In February 2020, Smith+Nephew announced a formal program dedicated to supporting ambulatory facilities and the creation or advancement of outpatient surgery programs.[8] Laura Rector, Vice President of Ambulatory Surgery Center Strategy and Development at Smith+Nephew, said that the organization committed a dedicated team of people and resources to the ASC market — including a staff increase from four people to more than 100 in just two years.

Smith+Nephew’s new ASC division, Positive Connections, helps customers achieve their specific goals within ASC settings. The division’s programs, partnerships and products target needs beyond what the company’s traditional products address.[9] Smith+Nephew’s ASC service portfolio development generated complementary products and services not previously offered. Smith+Nephew acquired three companies to develop an ASC-focused digital care management platform offering greater efficiency and improvement around the patient care experience.

“ASC sustainability has become a heavily emphasized message for leading orthopedic device companies,” said Carolyn LaWell, Chief Content Officer at ORTHOWORLD, noting that several other companies have taken a similar approach.

“Companies like Stryker, Smith+Nephew and Exactech are quickly growing their service line and technology offerings to support ASC performance,” she said. “We expect more orthopedic device companies to expand beyond their implant portfolios as they respond to the growth of the ASC market.”

Other ASC customers emphasize the need for future planning. “We need to work with suppliers to know there’s a cost-efficient future and set targets and say, ‘We’re here now. We all need to get there on cost efficiency and outcome,’ ” said Robert S. Bray Jr., M.D., Founder of the DISC Sport & Spine Center and leading ASC supplier collaborator. “Any procedure we’re doing needs to be data-driven, and that data needs to loop back to efficiency, cost and outcome.”

New Strategy Development and Deployment

Like their provider customers, orthopedic companies encounter various stages as they deploy resources and develop plans to capture and leverage this business shift. Critical questions on how to best position vendors to serve emerging markets are essential in efforts to offer the services, products and support health care providers need for evolving sites of care.

The orthopedic companies that will win the race to ASC market dominance have yet to be established, according to a 2019 Bain Research article.[10] With COVID-19’s enforced pause, the chance to claim a portion of the business remains open — but the window of opportunity for companies narrows every day.

Moving Forward Together

The shift to orthopedic and spine ASCs continues to accelerate. How fast this transition happens will vary based on market and industry dynamics. CMS policy changes, commercial payer steerage, patient preference and pressure to reduce costs will continue fueling the shift forward. Taking proactive strides to prepare for this business shift will help organizations adapt and thrive in the ambulatory setting. Effective collaboration between strategic suppliers and physician partners will enable a more successful transition for all.

References

1. CY 2022 Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System Proposed Rule (CMS-1753-P). Centers for Medicare & Medicaid Services website. July 19, 2021. Accessed October 5, 2021. cms.gov/newsroom/fact-sheets/cy-2022-medicare-hospital- outpatient-prospective-payment-system-and-ambulatory-surgical-center

2. 2021 full list of outpatient department services that require prior authorization. Centers for Medicare & Medicaid Services website. 2021. Accessed October 5, 2021.

3. UnitedHealth Group releases 2020 Sustainability Report. News release. UnitedHealth Group; June 15, 2021. Accessed October 5, 2021. www. unitedhealthgroup.com/newsroom/2021/2021-06-15-unitedhealth-group- releases-2020-sustainability-report.html

4. Dyrda L. The ASC-hospital power shift: who will win the next 3-5 years? Becker’s ASC Review. June 23, 2021. Accessed October 5, 2021. www.beckersasc.com/asc-news/the-asc-hospital-power-shift-who-will-win-the- next-3-5-years.html

5. Strata Decision Technology. National Patient and Procedure Volume Tracker purchased access. Accessed July 2021. Sg2 Analysis, 2021.

6. Proprietary Sg2 All-Payer Claims Data Set; IQVIA; Accessed August 2021. Sg2 Analysis, 2021.

7. Impact of Change®, 2021; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP) 2018. Agency for Healthcare Research and Quality, Rockville, MD; Proprietary Sg2 All-Payer Claims Data Set, 2018; The following 2018 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2021; Sg2 Analysis, 2021.

8. Smith+Nephew announces ambulatory services center strategy ‘Positive Connections.’ News release. Smith+Nephew website. February 24, 2020. Accessed October 5, 2021.

9. Vega P, Bray RS, Rector L, Terada R, Zentner K. Preparing for the shift In orthopedic and spine procedures to outpatient settings. Presented at: OMTEC Virtual Education Series for Orthopedic Engineers; June 17, 2021. Accessed October 5, 2021

10. Van Diesen T, Johnson T. Ambulatory surgery center growth accelerates: Is medtech ready? Bain & Company. September 23, 2019. Accessed October 5, 2021.

Orthopedic and spine care continue to evolve, with accelerated movement of procedures from traditional hospital-based settings to ambulatory facilities. Forward-thinking providers, along with orthopedic and spine product companies, are beginning to invest in resources to understand, predict and capitalize on these changes.

Clinical and...

Orthopedic and spine care continue to evolve, with accelerated movement of procedures from traditional hospital-based settings to ambulatory facilities. Forward-thinking providers, along with orthopedic and spine product companies, are beginning to invest in resources to understand, predict and capitalize on these changes.

Clinical and technical advances, coupled with evidence-based patient selection criteria, now make a growing pool of patients who are viable candidates for outpatient surgery. Many forces come into play, however, when considering market dynamics and predicting future potential changes.

Centers for Medicare & Medicaid Services Updates

Ongoing changes to site-of-care restrictions by the Centers for Medicare & Medicaid Services (CMS) are a key driver in the outpatient shift of orthopedic and spine procedures.

In recent years, CMS removed key musculoskeletal services from the inpatient-only list, including total knee arthroplasty in 2018, total hip arthroplasty in 2020 and partial hip and shoulder arthroplasties in 2021. Meanwhile, CMS continues to expand the ambulatory surgery center (ASC)-covered procedure list, including total knee arthroplasty in 2020 and total hip arthroplasty in 2021.[1]

In addition to its gradual removal of site-of-care restrictions, CMS recently implemented additional prior authorization requirements for cervical spinal fusions performed in hospital outpatient departments.[2] These authorizations are not required for ASCs.

Payer Pressures and the Pandemic Effect

Beyond CMS changes, commercial payers continue to expand the scope and use of their site-of-care medical necessity reviews to shift cases to ambulatory sites outside hospital campuses. For example, UnitedHealthcare has committed that more than 55% of member outpatient surgeries and radiology services will be delivered at high-quality, cost-efficient sites of care by 2030. This move, which highlights their intentions to direct more patients to ASCs,[3] makes strategic sense when ASCs can offer surgical procedures for 25% to 40% less cost than hospitals.[4]

Pandemic-fueled efforts to reduce risk and lengths of stay accelerated the outpatient and ambulatory shift substantially. Analysis by Sg2®, a Vizient company specializing in market research and intelligence, of hospital data from Strata Decision Technology, found that 62% of primary knee replacements were performed as outpatient procedures in the fourth quarter of 2020.[5] Similarly, Sg2 analysis of claims data found that the portion of commercially insured, inpatient, nonfracture primary hip replacements dropped from 77% in the fourth quarter of 2019 to 35% in the fourth quarter of 2020, with 50% performed in a hospital outpatient department and 15% performed in an ASC.[6]

Outpatient Growth Rates

The 2021 Impact of Change® forecast from Sg2 projects strong growth in outpatient procedures through 2029 — with anticipated outpatient growth of more than 30% for orthopedics and spine. (See Figure 1.) Concurrently, the inpatient procedures forecast predicts a 20% drop in orthopedics and a 14% drop in spine. For joint replacement, the Impact of Change forecast projects that 63% of nonfracture primary knee and hip replacements in 2022 will occur in outpatient settings.[7]

Figure 1. Orthopedic and Spine Surgery: Policy changes, COVID-19 pandemic and economic pressures accelerate HOPD/ASC shift (click to enlarge)

While providers and analysts expect surgical volume to grow in both orthopedics and spine, the transformation in how and where providers deliver care will affect clinical, operational and financial components for health care organizations, service groups and vendors.

Vendor Opportunity

While providers launch programs and facilities to meet patient needs, medical device vendors also have an opportunity to transition their offerings and pricing structures for customers. In a highly competitive space, the shift in sites of care may offer a window for both current and new players to capture additional market share. The pressure to reduce costs flows downstream — from patient to provider to device company. Business sustainability and growth will require new strategies.

New Ambulatory Vendor Strategies

Traditionally, device company sales representatives focused their marketing efforts primarily on surgeons. With the emergence of integrated delivery networks and supply chain’s refined role as a more strategic department, providers and decision-makers have a wider scope of influence. Vendor sales teams will need to deploy an enhanced skill set (more akin to account management) to serve as resources for these customers.

Price structure differences among facilities, compounded by reimbursement variance, may erode vendor inpatient pricing. This will likely require new product development, pricing model revisions and redesign of sales strategies across the full spectrum of treatment sites.

While addressing new stakeholders, influencers and cost pressures, orthopedic companies will look to new aggregated data for ambulatory surgery center trends. This analysis is market-specific, even hyperlocalized, due to regulatory, competitive and ownership influences.

Refining the ASC Sales Approach

Many orthopedic and spine companies have already deployed focused teams to evaluate opportunities to partner locally and create infrastructures to support and advance the ASC business segment. As previously noted, vendors are working to expand and complement traditional sales representative roles to incorporate more strategic account management.

In February 2020, Smith+Nephew announced a formal program dedicated to supporting ambulatory facilities and the creation or advancement of outpatient surgery programs.[8] Laura Rector, Vice President of Ambulatory Surgery Center Strategy and Development at Smith+Nephew, said that the organization committed a dedicated team of people and resources to the ASC market — including a staff increase from four people to more than 100 in just two years.

Smith+Nephew’s new ASC division, Positive Connections, helps customers achieve their specific goals within ASC settings. The division’s programs, partnerships and products target needs beyond what the company’s traditional products address.[9] Smith+Nephew’s ASC service portfolio development generated complementary products and services not previously offered. Smith+Nephew acquired three companies to develop an ASC-focused digital care management platform offering greater efficiency and improvement around the patient care experience.

“ASC sustainability has become a heavily emphasized message for leading orthopedic device companies,” said Carolyn LaWell, Chief Content Officer at ORTHOWORLD, noting that several other companies have taken a similar approach.

“Companies like Stryker, Smith+Nephew and Exactech are quickly growing their service line and technology offerings to support ASC performance,” she said. “We expect more orthopedic device companies to expand beyond their implant portfolios as they respond to the growth of the ASC market.”

Other ASC customers emphasize the need for future planning. “We need to work with suppliers to know there’s a cost-efficient future and set targets and say, ‘We’re here now. We all need to get there on cost efficiency and outcome,’ ” said Robert S. Bray Jr., M.D., Founder of the DISC Sport & Spine Center and leading ASC supplier collaborator. “Any procedure we’re doing needs to be data-driven, and that data needs to loop back to efficiency, cost and outcome.”

New Strategy Development and Deployment

Like their provider customers, orthopedic companies encounter various stages as they deploy resources and develop plans to capture and leverage this business shift. Critical questions on how to best position vendors to serve emerging markets are essential in efforts to offer the services, products and support health care providers need for evolving sites of care.

The orthopedic companies that will win the race to ASC market dominance have yet to be established, according to a 2019 Bain Research article.[10] With COVID-19’s enforced pause, the chance to claim a portion of the business remains open — but the window of opportunity for companies narrows every day.

Moving Forward Together

The shift to orthopedic and spine ASCs continues to accelerate. How fast this transition happens will vary based on market and industry dynamics. CMS policy changes, commercial payer steerage, patient preference and pressure to reduce costs will continue fueling the shift forward. Taking proactive strides to prepare for this business shift will help organizations adapt and thrive in the ambulatory setting. Effective collaboration between strategic suppliers and physician partners will enable a more successful transition for all.

References

1. CY 2022 Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System Proposed Rule (CMS-1753-P). Centers for Medicare & Medicaid Services website. July 19, 2021. Accessed October 5, 2021. cms.gov/newsroom/fact-sheets/cy-2022-medicare-hospital- outpatient-prospective-payment-system-and-ambulatory-surgical-center

2. 2021 full list of outpatient department services that require prior authorization. Centers for Medicare & Medicaid Services website. 2021. Accessed October 5, 2021.

3. UnitedHealth Group releases 2020 Sustainability Report. News release. UnitedHealth Group; June 15, 2021. Accessed October 5, 2021. www. unitedhealthgroup.com/newsroom/2021/2021-06-15-unitedhealth-group- releases-2020-sustainability-report.html

4. Dyrda L. The ASC-hospital power shift: who will win the next 3-5 years? Becker’s ASC Review. June 23, 2021. Accessed October 5, 2021. www.beckersasc.com/asc-news/the-asc-hospital-power-shift-who-will-win-the- next-3-5-years.html

5. Strata Decision Technology. National Patient and Procedure Volume Tracker purchased access. Accessed July 2021. Sg2 Analysis, 2021.

6. Proprietary Sg2 All-Payer Claims Data Set; IQVIA; Accessed August 2021. Sg2 Analysis, 2021.

7. Impact of Change®, 2021; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP) 2018. Agency for Healthcare Research and Quality, Rockville, MD; Proprietary Sg2 All-Payer Claims Data Set, 2018; The following 2018 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; Claritas Pop-Facts®, 2021; Sg2 Analysis, 2021.

8. Smith+Nephew announces ambulatory services center strategy ‘Positive Connections.’ News release. Smith+Nephew website. February 24, 2020. Accessed October 5, 2021.

9. Vega P, Bray RS, Rector L, Terada R, Zentner K. Preparing for the shift In orthopedic and spine procedures to outpatient settings. Presented at: OMTEC Virtual Education Series for Orthopedic Engineers; June 17, 2021. Accessed October 5, 2021

10. Van Diesen T, Johnson T. Ambulatory surgery center growth accelerates: Is medtech ready? Bain & Company. September 23, 2019. Accessed October 5, 2021.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

PV

Patrick Vega is Consulting Director for Vizient’s Excelerate and PPI Orthopedics. Mr. Vega consults to member hospitals, health systems and physicians in musculoskeletal services with a focus on high-value care by aligning cost, quality and performance.