Copy to clipboard

Copy to clipboard

Orthopaedic industry revenue reached $49.3 billion worldwide in 2017 and grew at 3.7%, ~$1.7 billion over 2016, according to our estimates to be published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® in May.

In 2017, the 20 largest orthopaedic device companies—those with revenue above $200 million—posted growth. That’s a statement we haven’t made for at least the last five years, and one we think indicates positive momentum in orthopaedics. What fueled this growth? New product launches, acquisitions and international expansion were the most-cited contributors by company executives.

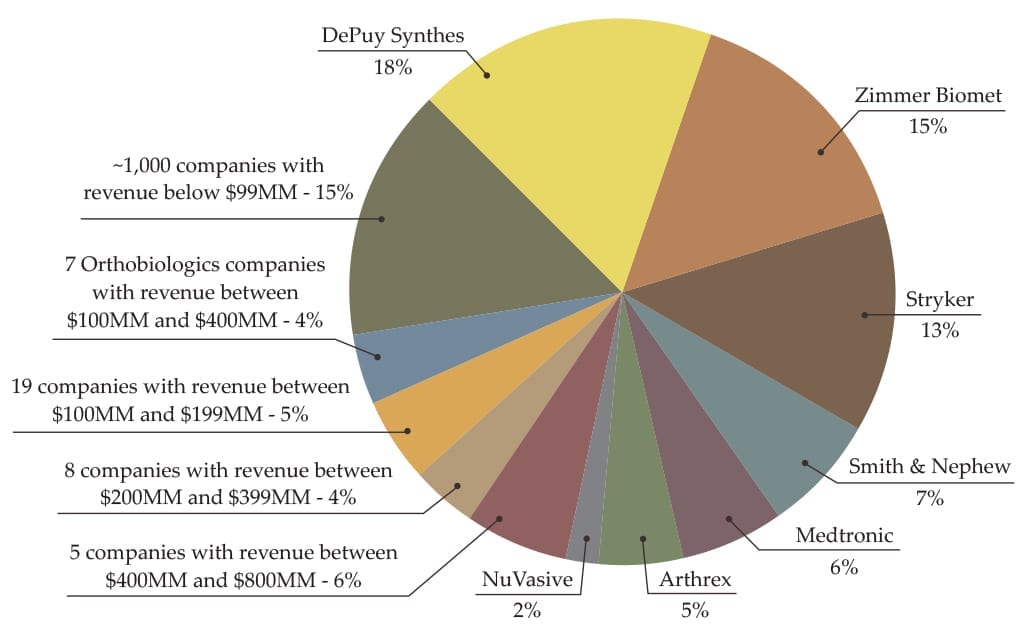

In Exhibit 1, we offer a high-level view of the top-tier companies and revenue for the next-tiers, while Exhibit 2 provides market share. Combined revenue for the top-tier companies—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew, Medtronic, Arthrex and NuVasive—accounts for 66% of the total orthopaedic industry. Together, these companies grew at a rate of 3.1% vs. the 3.7% industry average.

Exhibit 1: 2017 Total Orthopaedic Sales Performance ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| DePuy Synthes | $8,791.4 | $8,756.5 | $34.9 | 0.4% |

| Zimmer Biomet | $7,273.9 | $7,100.9 | $173.0 | 2.4% |

| Stryker | $6,670.0 | $6,330.8 | $339.2 | 5.4% |

| Smith & Nephew | $3,353.4 | $3,250.5 | $102.9 | 3.2% |

| Medtronic | $2,966.0 | $2,930.0 | $36.0 | 1.2% |

| Arthrex | $2,267.3 | $2,048.1 | $219.2 | 10.7% |

| NuVasive | $1,029.5 | $962.0 | $67.5 | 7.0% |

| 5 companies with revenue between $400MM and $800MM | $3,000.3 | $2,817.4 | $182.9 | 6.5% |

| 8 companies with revenue between $200MM and $399MM | $1,982.8 | $1,843.3 | $139.5 | 7.6% |

| 19 companies with revenue between $100MM and $199MM | $2,629.2 | $2,464.5 | $164.7 | 6.7% |

| 7 Orthobiologics companies with revenue between $100MM and $400MM | $1,884.9 | $1,825.2 | $59.7 | 3.3% |

| ~1,000 companies with revenue below $99MM | $7,520.1 | $7,256.7 | $263.4 | 3.6% |

| Total | $49,368.8 | $47,585.9 | $1,782.9 | 3.7% |

Exhibit 2: 2017 Market Share for Top-Tier Players and All Others

As can be seen in Exhibit 1, the tiers of device companies with revenue between $100 million and $800 million combined to generate revenue growth ~3% to ~4% higher than the industry as a whole. These companies often play in fewer market segments. As the Annual Report details, companies in these lower tiers are mainly experiencing growth in the highly pressured joint reconstruction and spine market segments.

In your review of the information in Exhibits 1 and 2, we feel it’s important to note that we called out predominantly orthobiologic companies with revenue above $100 million. These seven companies combined to grow at 3% in 2017 vs. 2016. Our rationale for separating orthobiologic and device companies was that 1) they are different types of companies from R&D, manufacturing and supply chain standpoints, and competitors and vendors view them through different lenses; 2) combining orthobiologic and device companies masked the growth experienced on the traditional hardware side of the industry.

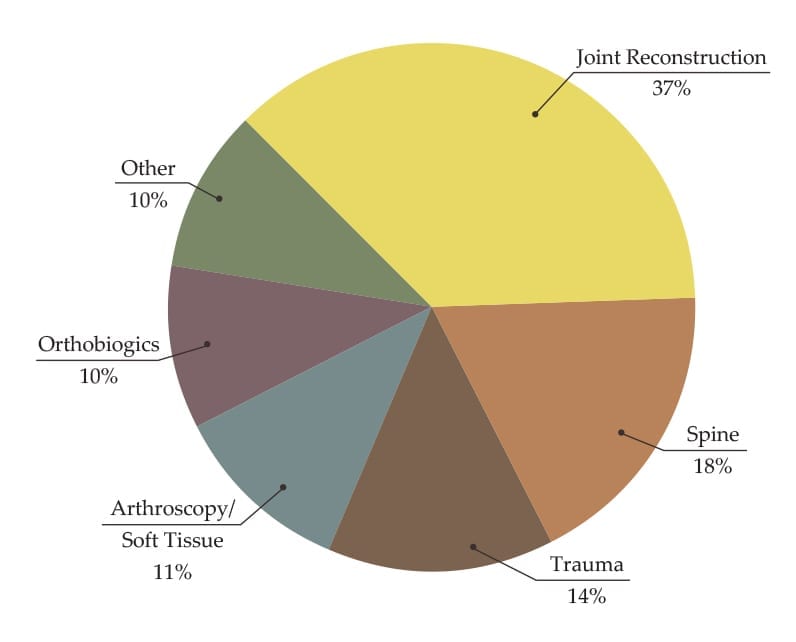

In looking at each market segment in 2017, we took away a few high-level observations, which are bulleted below and substantiated in Exhibits 3 and 4.

Exhibit 3: Product Segment Performance 2017 vs. 2016 ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Joint Reconstruction | $18,119.0 | $17,558.7 | $560.3 | 3.2% |

| Knee | $8,783.3 | $8,533.8 | $249.5 | 2.9% |

| Hip | $7,225.7 | $7,071.5 | $154.2 | 2.2% |

| Extremities | $2,110.0 | $1,953.4 | $156.6 | 8.0% |

| Spine | $9,080.9 | $8,883.7 | $197.2 | 2.2% |

| Trauma | $6,920.0 | $6,614.8 | $305.2 | 4.6% |

| Arthroscopy/Soft Tissue | $5,318.5 | $5,009.7 | $308.8 | 6.2% |

| Orthobiologics | $5,097.1 | $4,946.2 | $150.9 | 3.1% |

| Other* | $4,833.3 | $4,572.8 | $260.5 | 5.7% |

| Total | $49,368.8 | $47,585.9 | $1,782.9 | 3.7% |

*Other contains CMF, bone growth stimulation, bracing/soft goods, etc.

Exhibit 4: 2017 Orthopaedic Product Sales by Market Segment

- Joint reconstruction and spine, the two largest segments by revenue, together account for 55% of orthopaedic market revenue. Companies of all sizes within these segments continue to vocalize that payors and hospitals are pushing back on implant prices and demanding proof that products will perform as marketed. The 2% year-over-year growth of the hip, knee and spine markets is partially attributed to this payor and hospital scrutiny.

- Growth in the trauma market is largely driven by patient demographics and the need to heal broken bones. New products in 2017 came from all sorts of companies: top trauma players, those well-established in other segments and startups, as well, which drove market growth.

- Arthroscopy/soft tissue benefits from a younger, educated population that seeks to return to an active lifestyle. This market is dominated by seven players that control more than 90% of the market. These companies are actively launching new products for new indications, which ultimately leads to revenue.

- Orthobiologics are used across all orthopaedic segments. The faster-growing portions of the segment come from the use of products in arthroscopy/soft tissue or sports medicine. Use of orthobiologics remains scrutinized for joint reconstruction and spine indications.

We recommend that you download your Member copy of the newest Annual Report (publishing May 7) for a closer look at company and market segment specifics, as well as our five-year projections. We estimate that orthopaedic industry revenue will grow in the high 3% range over the next five years. Our forecast is conservative, yet optimistic, and based on trends identified in recent years that will carry through to the next decade.

On the conservative side:

While the top five players all posted positive revenue growth in 2017 vs. 2016, they continued to experience inconsistent (and in some cases flat or negative) revenue growth in the two largest market segments: joint reconstruction and spine. Consistency in year-over-year growth from these players is necessary for us to move beyond our conservative market projections.

International markets, specifically Asia, China and Europe, lack stability. Governments are enacting tougher regulations and decreasing reimbursement. More resources are required to enter or remain on the market in these countries, and companies stand to make less money on the products sold.

The demand for clinical and economic data on product performance in the U.S. is greater than we once thought. The move from volume to value and the rise of alternative payments was originally focused on joint reconstruction and spine. In our conversations with surgeons, payors and hospitals now require proof of outcomes across the board. We believe that this development will hinder growth of smaller companies that are seen as today’s industry innovators.

On the optimistic side:

Demographics. The need to heal bones, replace joints and repair tissue will continue as the global population grows in age and in numbers.

Supplier companies have indicated that sales are strong, in some cases too strong to keep up, and they are upbeat about the next nine months. For an industry that grew in the 2% to 3% range in recent years, we found this optimism to be unlike what we’ve heard in years past. Through our conversations, we could not identify the underlying market forces; however, we think that suspension of the device tax and the overhaul of the U.S. corporate tax will provide companies the ability to allocate earnings gains to R&D, operations and people.

Companies have invested in myriad opportunities that respond to surgeon and hospital demands. In implantables, we expect growth to come from additive manufacturing and new materials and coatings that promote bone in-growth and prevent infection. In regard to technology in the O.R., companies continue to develop planning, navigation and robotic tools, as well as instrument reduction and instrument packaging in order to create efficiencies and predictability. We expect a combination of these ideas will bring growth if well executed upon by companies.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

Orthopaedic industry revenue reached $49.3 billion worldwide in 2017 and grew at 3.7%, ~$1.7 billion over 2016, according to our estimates to be published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® in May.

In 2017, the 20 largest orthopaedic device companies—those with revenue above $200 million—posted growth. That’s a statement we...

Orthopaedic industry revenue reached $49.3 billion worldwide in 2017 and grew at 3.7%, ~$1.7 billion over 2016, according to our estimates to be published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® in May.

In 2017, the 20 largest orthopaedic device companies—those with revenue above $200 million—posted growth. That’s a statement we haven’t made for at least the last five years, and one we think indicates positive momentum in orthopaedics. What fueled this growth? New product launches, acquisitions and international expansion were the most-cited contributors by company executives.

In Exhibit 1, we offer a high-level view of the top-tier companies and revenue for the next-tiers, while Exhibit 2 provides market share. Combined revenue for the top-tier companies—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew, Medtronic, Arthrex and NuVasive—accounts for 66% of the total orthopaedic industry. Together, these companies grew at a rate of 3.1% vs. the 3.7% industry average.

Exhibit 1: 2017 Total Orthopaedic Sales Performance ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| DePuy Synthes | $8,791.4 | $8,756.5 | $34.9 | 0.4% |

| Zimmer Biomet | $7,273.9 | $7,100.9 | $173.0 | 2.4% |

| Stryker | $6,670.0 | $6,330.8 | $339.2 | 5.4% |

| Smith & Nephew | $3,353.4 | $3,250.5 | $102.9 | 3.2% |

| Medtronic | $2,966.0 | $2,930.0 | $36.0 | 1.2% |

| Arthrex | $2,267.3 | $2,048.1 | $219.2 | 10.7% |

| NuVasive | $1,029.5 | $962.0 | $67.5 | 7.0% |

| 5 companies with revenue between $400MM and $800MM | $3,000.3 | $2,817.4 | $182.9 | 6.5% |

| 8 companies with revenue between $200MM and $399MM | $1,982.8 | $1,843.3 | $139.5 | 7.6% |

| 19 companies with revenue between $100MM and $199MM | $2,629.2 | $2,464.5 | $164.7 | 6.7% |

| 7 Orthobiologics companies with revenue between $100MM and $400MM | $1,884.9 | $1,825.2 | $59.7 | 3.3% |

| ~1,000 companies with revenue below $99MM | $7,520.1 | $7,256.7 | $263.4 | 3.6% |

| Total | $49,368.8 | $47,585.9 | $1,782.9 | 3.7% |

Exhibit 2: 2017 Market Share for Top-Tier Players and All Others

As can be seen in Exhibit 1, the tiers of device companies with revenue between $100 million and $800 million combined to generate revenue growth ~3% to ~4% higher than the industry as a whole. These companies often play in fewer market segments. As the Annual Report details, companies in these lower tiers are mainly experiencing growth in the highly pressured joint reconstruction and spine market segments.

In your review of the information in Exhibits 1 and 2, we feel it’s important to note that we called out predominantly orthobiologic companies with revenue above $100 million. These seven companies combined to grow at 3% in 2017 vs. 2016. Our rationale for separating orthobiologic and device companies was that 1) they are different types of companies from R&D, manufacturing and supply chain standpoints, and competitors and vendors view them through different lenses; 2) combining orthobiologic and device companies masked the growth experienced on the traditional hardware side of the industry.

In looking at each market segment in 2017, we took away a few high-level observations, which are bulleted below and substantiated in Exhibits 3 and 4.

Exhibit 3: Product Segment Performance 2017 vs. 2016 ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Joint Reconstruction | $18,119.0 | $17,558.7 | $560.3 | 3.2% |

| Knee | $8,783.3 | $8,533.8 | $249.5 | 2.9% |

| Hip | $7,225.7 | $7,071.5 | $154.2 | 2.2% |

| Extremities | $2,110.0 | $1,953.4 | $156.6 | 8.0% |

| Spine | $9,080.9 | $8,883.7 | $197.2 | 2.2% |

| Trauma | $6,920.0 | $6,614.8 | $305.2 | 4.6% |

| Arthroscopy/Soft Tissue | $5,318.5 | $5,009.7 | $308.8 | 6.2% |

| Orthobiologics | $5,097.1 | $4,946.2 | $150.9 | 3.1% |

| Other* | $4,833.3 | $4,572.8 | $260.5 | 5.7% |

| Total | $49,368.8 | $47,585.9 | $1,782.9 | 3.7% |

*Other contains CMF, bone growth stimulation, bracing/soft goods, etc.

Exhibit 4: 2017 Orthopaedic Product Sales by Market Segment

- Joint reconstruction and spine, the two largest segments by revenue, together account for 55% of orthopaedic market revenue. Companies of all sizes within these segments continue to vocalize that payors and hospitals are pushing back on implant prices and demanding proof that products will perform as marketed. The 2% year-over-year growth of the hip, knee and spine markets is partially attributed to this payor and hospital scrutiny.

- Growth in the trauma market is largely driven by patient demographics and the need to heal broken bones. New products in 2017 came from all sorts of companies: top trauma players, those well-established in other segments and startups, as well, which drove market growth.

- Arthroscopy/soft tissue benefits from a younger, educated population that seeks to return to an active lifestyle. This market is dominated by seven players that control more than 90% of the market. These companies are actively launching new products for new indications, which ultimately leads to revenue.

- Orthobiologics are used across all orthopaedic segments. The faster-growing portions of the segment come from the use of products in arthroscopy/soft tissue or sports medicine. Use of orthobiologics remains scrutinized for joint reconstruction and spine indications.

We recommend that you download your Member copy of the newest Annual Report (publishing May 7) for a closer look at company and market segment specifics, as well as our five-year projections. We estimate that orthopaedic industry revenue will grow in the high 3% range over the next five years. Our forecast is conservative, yet optimistic, and based on trends identified in recent years that will carry through to the next decade.

On the conservative side:

While the top five players all posted positive revenue growth in 2017 vs. 2016, they continued to experience inconsistent (and in some cases flat or negative) revenue growth in the two largest market segments: joint reconstruction and spine. Consistency in year-over-year growth from these players is necessary for us to move beyond our conservative market projections.

International markets, specifically Asia, China and Europe, lack stability. Governments are enacting tougher regulations and decreasing reimbursement. More resources are required to enter or remain on the market in these countries, and companies stand to make less money on the products sold.

The demand for clinical and economic data on product performance in the U.S. is greater than we once thought. The move from volume to value and the rise of alternative payments was originally focused on joint reconstruction and spine. In our conversations with surgeons, payors and hospitals now require proof of outcomes across the board. We believe that this development will hinder growth of smaller companies that are seen as today’s industry innovators.

On the optimistic side:

Demographics. The need to heal bones, replace joints and repair tissue will continue as the global population grows in age and in numbers.

Supplier companies have indicated that sales are strong, in some cases too strong to keep up, and they are upbeat about the next nine months. For an industry that grew in the 2% to 3% range in recent years, we found this optimism to be unlike what we’ve heard in years past. Through our conversations, we could not identify the underlying market forces; however, we think that suspension of the device tax and the overhaul of the U.S. corporate tax will provide companies the ability to allocate earnings gains to R&D, operations and people.

Companies have invested in myriad opportunities that respond to surgeon and hospital demands. In implantables, we expect growth to come from additive manufacturing and new materials and coatings that promote bone in-growth and prevent infection. In regard to technology in the O.R., companies continue to develop planning, navigation and robotic tools, as well as instrument reduction and instrument packaging in order to create efficiencies and predictability. We expect a combination of these ideas will bring growth if well executed upon by companies.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.