Copy to clipboard

Copy to clipboard

Joint reconstruction accounts for 37% of the global orthopaedic industry. We estimate that joint reconstruction product revenue surpassed $18 billion in 2017, an increase of $560.3 million or 3.2% vs. 2016. These numbers were published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® and are depicted in Exhibit 1, below.

Exhibit 1: 2017 Joint Reconstruction Sales Performance: Top 10 and All Others ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Zimmer Biomet | $5,021.9 | $5,012.5 | $9.4 | 0.2% |

| Stryker | $3,584.5 | $3,408.0 | $176.5 | 5.2% |

| DePuy Synthes | $3,350.2 | $3,315.4 | $34.8 | 1.1% |

| Smith & Nephew | $1,669.5 | $1,609.8 | $59.8 | 3.7% |

| Top-Tier Players Total | $13,626.1 | $13,345.7 | $280.5 | 2.1% |

| Aesculap | $414.3 | $401.0 | $13.3 | 3.3% |

| Wright Medical | $338.3 | $306.6 | $31.7 | 10.3% |

| Medacta | $266.2 | $236.6 | $29.6 | 12.5% |

| Exactech | $256.6 | $241.1 | $15.5 | 6.4% |

| DJO Surgical | $253.6 | $209.6 | $44.0 | 21.0% |

| MicroPort Orthopedics | $211.8 | $205.2 | $6.6 | 3.2% |

| Next-Tier Players Total | $1,740.8 | $1,600.1 | $140.7 | 8.8% |

| 6 companies w/revenue between $100MM-$210MM | $898.6 | $830.5 | $68.1 | 8.2% |

| ~150 companies w/revenue below $99MM | $1,853.5 | $1,782.4 | $71.0 | 4.0% |

| Total | $18,119.0 | $17,558.7 | $560.3 | 3.2% |

In 2017, the knee and hip markets came in under our projections due to a slowing of international markets and weather-related incidents in the U.S. during the year, while extremities reconstruction maintained high-single-digit growth, benefiting from shoulder and ankle procedures.

The seven public companies among the top 10 players in joint reconstruction—Zimmer Biomet, Stryker, DePuy Synthes, Smith & Nephew, Wright Medical, DJO and MicroPort Orthopedics—posted 1H18 joint reconstruction sales of $7.5 billion, an increase of $299.5 million or 4.1% vs. 1H17. (See Exhibit 2.) These seven companies posted joint reconstruction sales +2.4% in 1H17 vs. 1H16.

Exhibit 2: 1H18 Joint Reconstruction Sales Performance: Top 7 Public Companies ($Millions)

| 1H18 | 1H17 | $ Change | % Change | |

| Zimmer Biomet | $2,604.2 | $2,524.0 | $80.2 | 3.2% |

| DePuy Synthes | $1,735.5 | $1,736.9 | -$1.4 | -0.1% |

| Stryker | $1,856.3 | $1,738.4 | $117.9 | 6.8% |

| Smith & Nephew | $871.5 | $834.9 | $36.6 | 4.4% |

| Wright Medical | $197.7 | $163.4 | $34.3 | 21.0% |

| DJO | $142.0 | $121.0 | $21.0 | 17.4% |

| MicroPort Orthopedics | $119.7 | $108.8 | $10.9 | 10.0% |

| Total | $7,526.9 | $7,227.4 | $299.5 | 4.1% |

Leadership from these companies have commented on positive adoption of new products. Therefore, results from 1H18 indicate that the joint reconstruction market could outpace our projection of 3.4% growth for 2018.

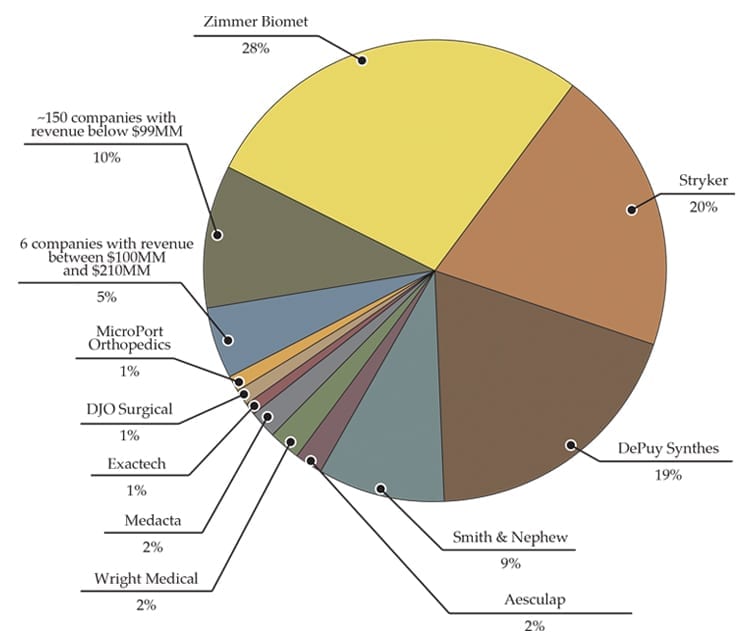

Zimmer Biomet remains the dominant player in the total joint reconstruction market, with 28% market share. Combined, the top four companies in the segment account for 76% of sales, and the top ten companies account for 85% of sales. (See Exhibit 3.)

Exhibit 3: 2017 Joint Reconstruction Market Share: Top Players and All Others

Let’s look closer at past activity and future predictions for hip, knee and extremities.

HIPS AND KNEES

Knee and hip implants face price pressure globally. In 2017, major players noted a decrease in price of 1% to 3% in the U.S., as well as increased competition. Companies posted consistent ex-U.S. growth in years past, though in 2017 there was greater mention of increased competition and capped prices in some countries. For example, in India, knee prices were slashed between 59% and 69%. This impacted DePuy Synthes’ knee sales by $12 million in 2017. The India knee implant price cap will be imposed for another year, through August 2019.

Although pressures persist, an increase in procedures has lent stability to the segments. We expect the top ten players to post positive knee and hip growth in 2018. We expect the knee and hip segments to continue growth in the low-single-digit rage through 2022 due to the following factors.

A study highlighted by the American Academy of Orthopaedic Surgeons noted that primary total joint reconstruction is expected to grow 171% through 2030, reaching 635,000 procedures per year in the U.S., and primary total knee reconstruction is expected to grow 189% through 2030, reaching 1.28 million procedures per year. Players in the market can expect growth in procedure volume globally.

The top four players derive the largest portion of their sales from joint reconstruction. It’s a priority market for them. To remain competitive, these four are engaged in R&D or have launched a diversified group of products that cater to a diversified group of surgeons. These include robotics, navigation, additive manufacturing, solutions to monitor episodes of care, lower-tiered products in emerging markets and the ability to engage in risk sharing programs.

The Centers for Medicare & Medicaid began to cover total knee replacement in the outpatient setting in 2018. Private payors have incentivized this move in knee and hip for several years. OEMs able to simplify procedures and assist ASCs in this transition, presumably smaller more nimble companies, have an opportunity for greater revenue growth.

The sheer size of the joint reconstruction market makes it attractive to new players. Established orthopaedic companies or startups that are able to offer implants at lower prices, or meet the demands of efficiency and outcomes, will be well-positioned to scale themselves or be acquired and then scaled. We identified three companies that received their first FDA 510(k) clearance for a knee device in 2017— Amplitude Surgical, Bodycad and XpandOrtho—and three that received their first FDA 510(k) clearance for a hip in 2017—ConforMIS, Responsive Orthopedics (acquired by Medtronic) and SurgTech.

EXTREMITIES

The extremities reconstruction market remains a reliable source of revenue for the segment’s top players, growing 8.0% in 2017 vs. 2016 to surpass $2 billion. Six of the top 10 extremities companies—Wright Medical, DJO, Exactech, Stryker, Arthrosurface, LimaCorporate—posted double-digit growth in 2017 vs. 2016.

This growth was buoyed by new shoulder and ankle product offerings. Wright Medical noted 29% year-over-year growth in its upper extremity products. DJO launched its anatomic shoulder, featuring a proprietary “porous porous” coating. Exactech launched a total ankle and shoulder stems. Companies experiencing this growth continue beyond the top ten and include Integra LifeSciences and Corin. Stemless designs for the shoulder and adoption of planning, navigation and robotic technology have fueled growth of surgical procedures in this market.

We expect the extremities recon segment to continue growth in the high-single-digit range through 2022 due to the following factors.

The number of U.S. shoulder and ankle procedures grew nearly 10% in 2017 vs. 2016. This is compared to hand/wrist and elbow, growing at 7% and digits growing at 4%, according to Orthopedic Network News. The same report showed 61% of extremities procedures taking place in shoulder and 3% in ankle. Growth in procedure volume in the U.S. and ex-U.S., including Europe and Japan, will continue to propel this segment of the market.

Mimicking what has taken place in knee and hip, we expect companies to make their implant portfolios more appealing with technology that aids the procedure, from preoperative planning to robotics.

Companies with knowledge of the extremity space may enter the faster-growing markets of shoulder and ankle, seeing them as complementary to their current R&D efforts and surgeon relationships.

LOOKING AHEAD

To outline the direction of the overall joint reconstruction segment, we asked Stan Mendenhall, Editor of Orthopedic Network News, to provide perspective that he’s gained from his reader base of hospital administrators. His responses:

Products that reduce costs and improve quality, and those that create new business for device companies, will significantly impact the joint reconstruction space in the next five years. For example, shoulder replacement year-over-year growth exceeds hip and knee replacement largely as a result of expanded indications for shoulder replacement. The knee and hip markets have matured. Niche areas for shoulders, elbows, ankles, wrists and other joints are being and will continue to be targeted by many companies.

The movement of joint replacement procedures to outpatient centers will have an enormous impact on the industry. ORTHOWORLD has cited previous surveys noting that the market was 85% inpatient/15% outpatient in 2016. That number is expected to shift to nearly 60% inpatient/40% outpatient by 2022, and nearly 50/50 by 2024. Not only will device companies need to consider their strategies to meet their customers’ needs, but this will also impact hospital infrastructure, as they were largely built for inpatient care.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

Joint reconstruction accounts for 37% of the global orthopaedic industry. We estimate that joint reconstruction product revenue surpassed $18 billion in 2017, an increase of $560.3 million or 3.2% vs. 2016. These numbers were published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® and are depicted in Exhibit 1, below.

Exhibit 1: 2017...

Joint reconstruction accounts for 37% of the global orthopaedic industry. We estimate that joint reconstruction product revenue surpassed $18 billion in 2017, an increase of $560.3 million or 3.2% vs. 2016. These numbers were published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® and are depicted in Exhibit 1, below.

Exhibit 1: 2017 Joint Reconstruction Sales Performance: Top 10 and All Others ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Zimmer Biomet | $5,021.9 | $5,012.5 | $9.4 | 0.2% |

| Stryker | $3,584.5 | $3,408.0 | $176.5 | 5.2% |

| DePuy Synthes | $3,350.2 | $3,315.4 | $34.8 | 1.1% |

| Smith & Nephew | $1,669.5 | $1,609.8 | $59.8 | 3.7% |

| Top-Tier Players Total | $13,626.1 | $13,345.7 | $280.5 | 2.1% |

| Aesculap | $414.3 | $401.0 | $13.3 | 3.3% |

| Wright Medical | $338.3 | $306.6 | $31.7 | 10.3% |

| Medacta | $266.2 | $236.6 | $29.6 | 12.5% |

| Exactech | $256.6 | $241.1 | $15.5 | 6.4% |

| DJO Surgical | $253.6 | $209.6 | $44.0 | 21.0% |

| MicroPort Orthopedics | $211.8 | $205.2 | $6.6 | 3.2% |

| Next-Tier Players Total | $1,740.8 | $1,600.1 | $140.7 | 8.8% |

| 6 companies w/revenue between $100MM-$210MM | $898.6 | $830.5 | $68.1 | 8.2% |

| ~150 companies w/revenue below $99MM | $1,853.5 | $1,782.4 | $71.0 | 4.0% |

| Total | $18,119.0 | $17,558.7 | $560.3 | 3.2% |

In 2017, the knee and hip markets came in under our projections due to a slowing of international markets and weather-related incidents in the U.S. during the year, while extremities reconstruction maintained high-single-digit growth, benefiting from shoulder and ankle procedures.

The seven public companies among the top 10 players in joint reconstruction—Zimmer Biomet, Stryker, DePuy Synthes, Smith & Nephew, Wright Medical, DJO and MicroPort Orthopedics—posted 1H18 joint reconstruction sales of $7.5 billion, an increase of $299.5 million or 4.1% vs. 1H17. (See Exhibit 2.) These seven companies posted joint reconstruction sales +2.4% in 1H17 vs. 1H16.

Exhibit 2: 1H18 Joint Reconstruction Sales Performance: Top 7 Public Companies ($Millions)

| 1H18 | 1H17 | $ Change | % Change | |

| Zimmer Biomet | $2,604.2 | $2,524.0 | $80.2 | 3.2% |

| DePuy Synthes | $1,735.5 | $1,736.9 | -$1.4 | -0.1% |

| Stryker | $1,856.3 | $1,738.4 | $117.9 | 6.8% |

| Smith & Nephew | $871.5 | $834.9 | $36.6 | 4.4% |

| Wright Medical | $197.7 | $163.4 | $34.3 | 21.0% |

| DJO | $142.0 | $121.0 | $21.0 | 17.4% |

| MicroPort Orthopedics | $119.7 | $108.8 | $10.9 | 10.0% |

| Total | $7,526.9 | $7,227.4 | $299.5 | 4.1% |

Leadership from these companies have commented on positive adoption of new products. Therefore, results from 1H18 indicate that the joint reconstruction market could outpace our projection of 3.4% growth for 2018.

Zimmer Biomet remains the dominant player in the total joint reconstruction market, with 28% market share. Combined, the top four companies in the segment account for 76% of sales, and the top ten companies account for 85% of sales. (See Exhibit 3.)

Exhibit 3: 2017 Joint Reconstruction Market Share: Top Players and All Others

Let’s look closer at past activity and future predictions for hip, knee and extremities.

HIPS AND KNEES

Knee and hip implants face price pressure globally. In 2017, major players noted a decrease in price of 1% to 3% in the U.S., as well as increased competition. Companies posted consistent ex-U.S. growth in years past, though in 2017 there was greater mention of increased competition and capped prices in some countries. For example, in India, knee prices were slashed between 59% and 69%. This impacted DePuy Synthes’ knee sales by $12 million in 2017. The India knee implant price cap will be imposed for another year, through August 2019.

Although pressures persist, an increase in procedures has lent stability to the segments. We expect the top ten players to post positive knee and hip growth in 2018. We expect the knee and hip segments to continue growth in the low-single-digit rage through 2022 due to the following factors.

A study highlighted by the American Academy of Orthopaedic Surgeons noted that primary total joint reconstruction is expected to grow 171% through 2030, reaching 635,000 procedures per year in the U.S., and primary total knee reconstruction is expected to grow 189% through 2030, reaching 1.28 million procedures per year. Players in the market can expect growth in procedure volume globally.

The top four players derive the largest portion of their sales from joint reconstruction. It’s a priority market for them. To remain competitive, these four are engaged in R&D or have launched a diversified group of products that cater to a diversified group of surgeons. These include robotics, navigation, additive manufacturing, solutions to monitor episodes of care, lower-tiered products in emerging markets and the ability to engage in risk sharing programs.

The Centers for Medicare & Medicaid began to cover total knee replacement in the outpatient setting in 2018. Private payors have incentivized this move in knee and hip for several years. OEMs able to simplify procedures and assist ASCs in this transition, presumably smaller more nimble companies, have an opportunity for greater revenue growth.

The sheer size of the joint reconstruction market makes it attractive to new players. Established orthopaedic companies or startups that are able to offer implants at lower prices, or meet the demands of efficiency and outcomes, will be well-positioned to scale themselves or be acquired and then scaled. We identified three companies that received their first FDA 510(k) clearance for a knee device in 2017— Amplitude Surgical, Bodycad and XpandOrtho—and three that received their first FDA 510(k) clearance for a hip in 2017—ConforMIS, Responsive Orthopedics (acquired by Medtronic) and SurgTech.

EXTREMITIES

The extremities reconstruction market remains a reliable source of revenue for the segment’s top players, growing 8.0% in 2017 vs. 2016 to surpass $2 billion. Six of the top 10 extremities companies—Wright Medical, DJO, Exactech, Stryker, Arthrosurface, LimaCorporate—posted double-digit growth in 2017 vs. 2016.

This growth was buoyed by new shoulder and ankle product offerings. Wright Medical noted 29% year-over-year growth in its upper extremity products. DJO launched its anatomic shoulder, featuring a proprietary “porous porous” coating. Exactech launched a total ankle and shoulder stems. Companies experiencing this growth continue beyond the top ten and include Integra LifeSciences and Corin. Stemless designs for the shoulder and adoption of planning, navigation and robotic technology have fueled growth of surgical procedures in this market.

We expect the extremities recon segment to continue growth in the high-single-digit range through 2022 due to the following factors.

The number of U.S. shoulder and ankle procedures grew nearly 10% in 2017 vs. 2016. This is compared to hand/wrist and elbow, growing at 7% and digits growing at 4%, according to Orthopedic Network News. The same report showed 61% of extremities procedures taking place in shoulder and 3% in ankle. Growth in procedure volume in the U.S. and ex-U.S., including Europe and Japan, will continue to propel this segment of the market.

Mimicking what has taken place in knee and hip, we expect companies to make their implant portfolios more appealing with technology that aids the procedure, from preoperative planning to robotics.

Companies with knowledge of the extremity space may enter the faster-growing markets of shoulder and ankle, seeing them as complementary to their current R&D efforts and surgeon relationships.

LOOKING AHEAD

To outline the direction of the overall joint reconstruction segment, we asked Stan Mendenhall, Editor of Orthopedic Network News, to provide perspective that he’s gained from his reader base of hospital administrators. His responses:

Products that reduce costs and improve quality, and those that create new business for device companies, will significantly impact the joint reconstruction space in the next five years. For example, shoulder replacement year-over-year growth exceeds hip and knee replacement largely as a result of expanded indications for shoulder replacement. The knee and hip markets have matured. Niche areas for shoulders, elbows, ankles, wrists and other joints are being and will continue to be targeted by many companies.

The movement of joint replacement procedures to outpatient centers will have an enormous impact on the industry. ORTHOWORLD has cited previous surveys noting that the market was 85% inpatient/15% outpatient in 2016. That number is expected to shift to nearly 60% inpatient/40% outpatient by 2022, and nearly 50/50 by 2024. Not only will device companies need to consider their strategies to meet their customers’ needs, but this will also impact hospital infrastructure, as they were largely built for inpatient care.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.