Copy to clipboard

Copy to clipboard

Elective procedures resumed in late second quarter for most of the U.S., allowing hospitals to begin to revive their more lucrative revenue lines. But as the U.S. contends with the continued spread of COVID-19, hospitals maintain a grim outlook for 2020 and into 2021.

Like most businesses, U.S. providers are making difficult decisions about their spending and strategies, said Chuck Peck, M.D., a Partner at Guidehouse and former President and CEO of Piedmont Athens Regional Medical Center in Georgia. Orthopedic companies will be better prepared to respond to their customers by understanding the business measures that hospitals are taking.

Dr. Peck shared analysis from Guidehouse’s COVID-19 Hospital & Health System Survey, which asked 174 executives in May about the pandemic’s impact on revenue, elective procedure volumes and strategies such as telehealth. In analyzing the survey response, Dr. Peck said, “Through all the uncertainty COVID-19 has presented, one thing hospitals and health systems can be certain of is that their business models will not return to what they were pre-pandemic.”

Hospitals Expect Double Digit Revenue Loss

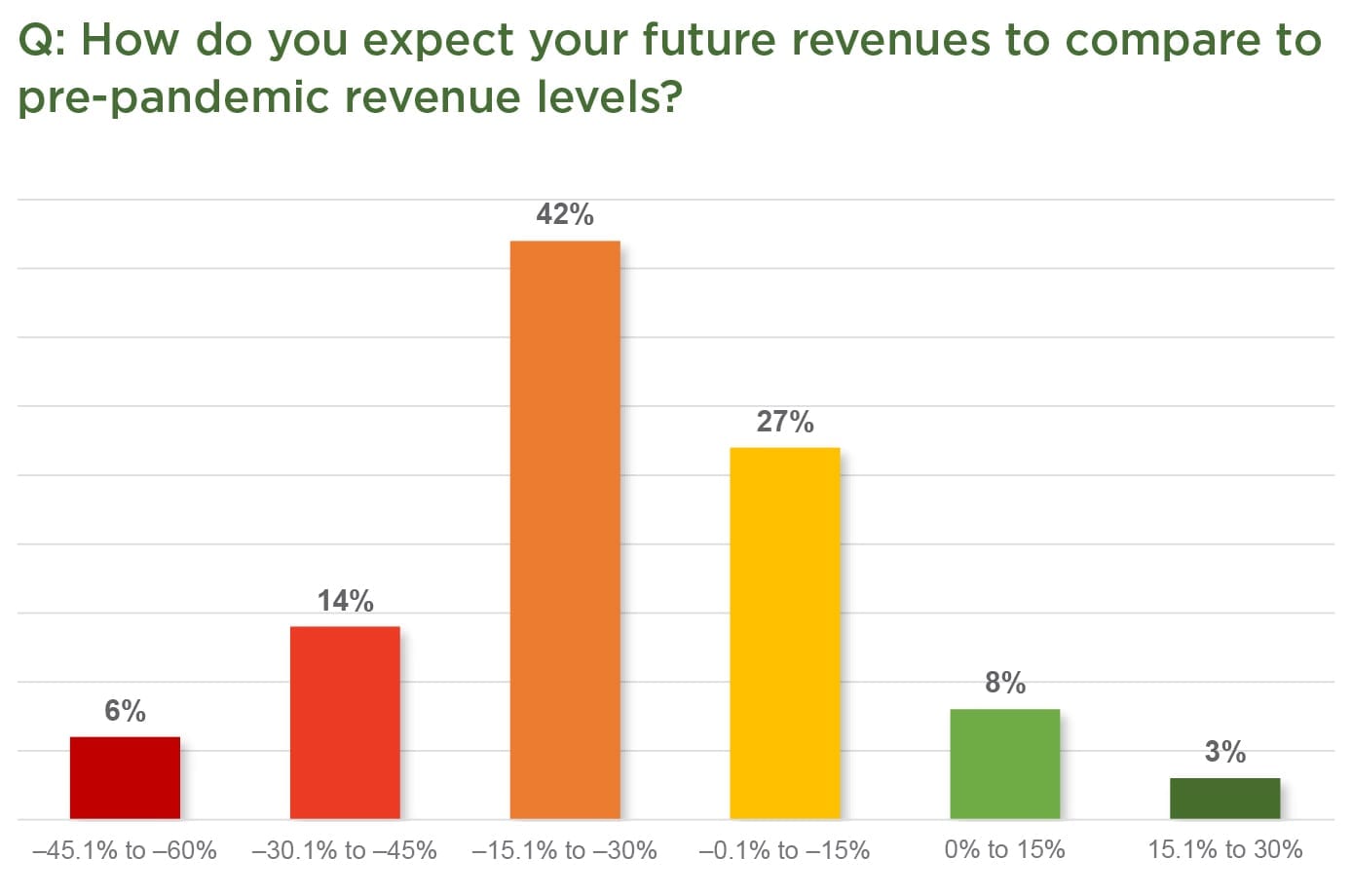

Not surprisingly, nine out of 10 executives that took Guidehouse’s survey said that they expect their organizations’ revenue to be lower at the end of 2020 than it was pre-COVID. Nearly two-thirds expect revenue to decrease by 15% or more in 2020 and one in five project revenue to decrease by 30% or more in 2020. Exhibit 1 details 2020 revenue compared to pre-COVID revenue.

Exhibit 1: 2020 vs. Pre-Pandemic Revenue (Click to enlarge)

The American Hospital Association quantified providers’ revenue losses for the first four months of the pandemic. It estimated that from March 1 to June 30, U.S. hospitals and health systems lost $202.6 billion. Canceled surgeries, outpatient treatment and reduced emergency department services resulted in a loss of $161.4 billion for U.S. non-federal hospitals, according to the association.

Hospitals are balancing the decrease in revenue with an increase in costs associated with COVID-19, everything from PPE to virtual health platforms. While the U.S. federal government announced billions of dollars in aid to hospitals, Guidehouse’s survey found that only 11% of executive respondents believed that the money would be enough to cover additional expenses from COVID-19.

Still, executives expect their hospitals and health systems to see an increase in revenue in the second half of the year and into 2021, as elective procedure volume builds and patients return to receive routine care.

“On the positive side, executives expect the long-term view won’t be as grim, foreseeing only 3% lower revenue one year from now,” Dr. Peck said.

Procedure Volume Outlook

In the middle of July, analysts noted that about 90% of the U.S. was open for elective procedures. While it’s unlikely that we’ll see the nearly nationwide halt of elective procedures again, until the virus is suppressed, we expect that procedures will stop at local levels when cities face large COVID outbreaks.

“In some hot spots, hospitals have started closing down elective surgeries again,” Dr. Peck said. “In others, even though the COVID caseload continues to be high, organizations feel comfortable that they have enough PPE, testing and tracing to continue with elective surgeries they already opened several months ago.”

U.S. hospitals have turned their focus, Peck said, to how long it will take procedures to return to pre-COVID levels.

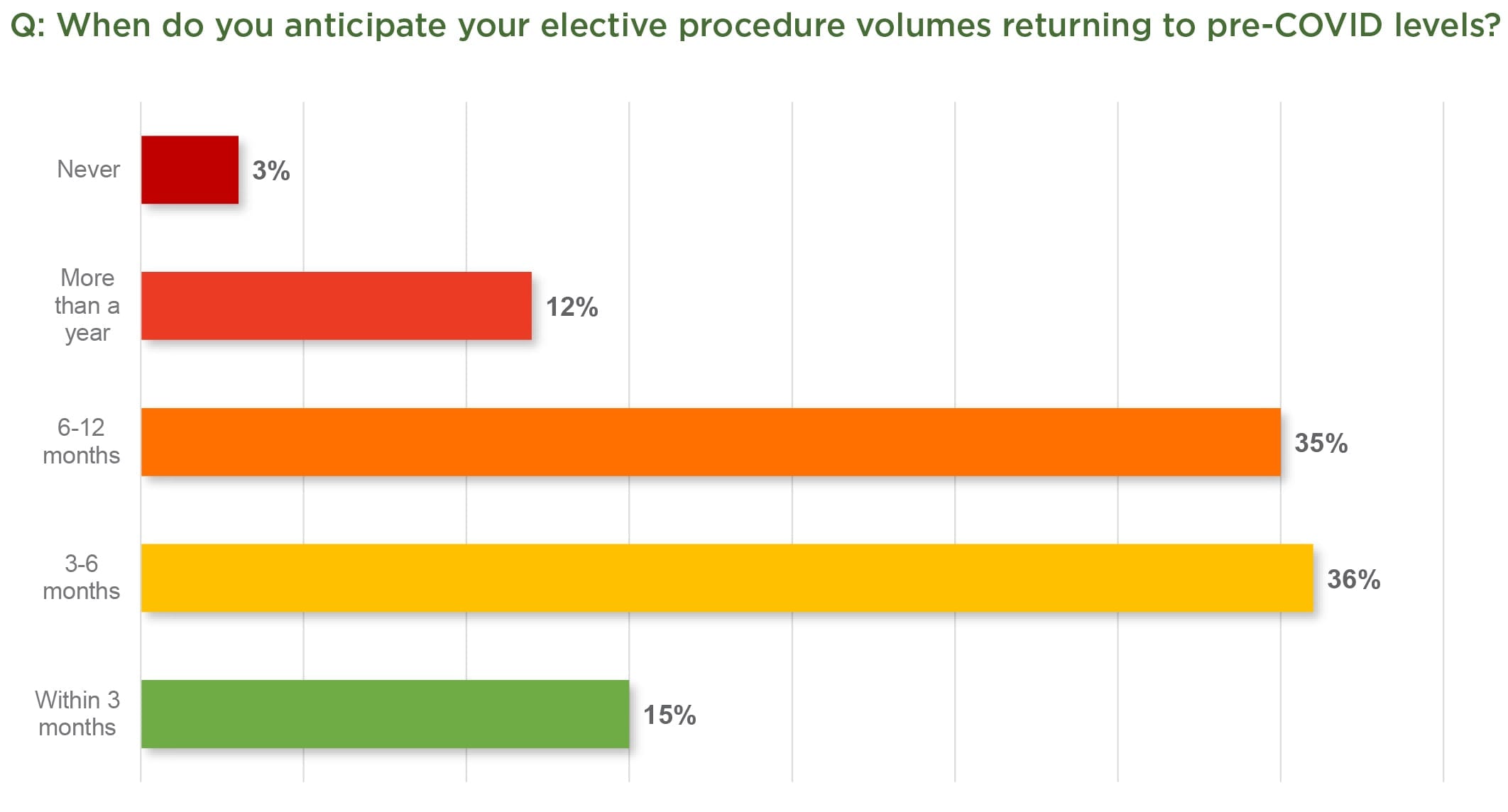

Guidehouse’s survey, which took into account all elective procedures, found that half of respondents thought it would take through the end of 2020 or longer for procedure volumes to return to pre-COVID levels. Exhibit 2 highlights the length of time executives said it would take for their organizations to ramp up procedures.

Exhibit 2: Elective Procedures Anticipated Return to Pre-COVID Levels (Click to enlarge)

Orthopedic surgeons echoed a similar sentiment. In a survey taken by 1,523 members of the American Academy of Orthopaedic Surgeons, 70% of surgeons thought that it would take five months after procedures resume to regain 90% of pre-COVID surgical volume.

Based on these assertions from hospitals and surgeons and commentary from orthopedic companies, we do not foresee orthopedic procedures returning to pre-COVID volume in 2020.

What is the Impact to Hospitals?

As hospitals balance revenue loss with an increase in expenses from COVID patients, they’re making short- and long-term decisions that could impact orthopedic companies.

“Although healthcare organizations remain focused on managing the day-to-day realities of COVID-19, they are also eyeing the future and thinking through how the crisis will impact them clinically, financially and operationally,” Dr. Peck said.

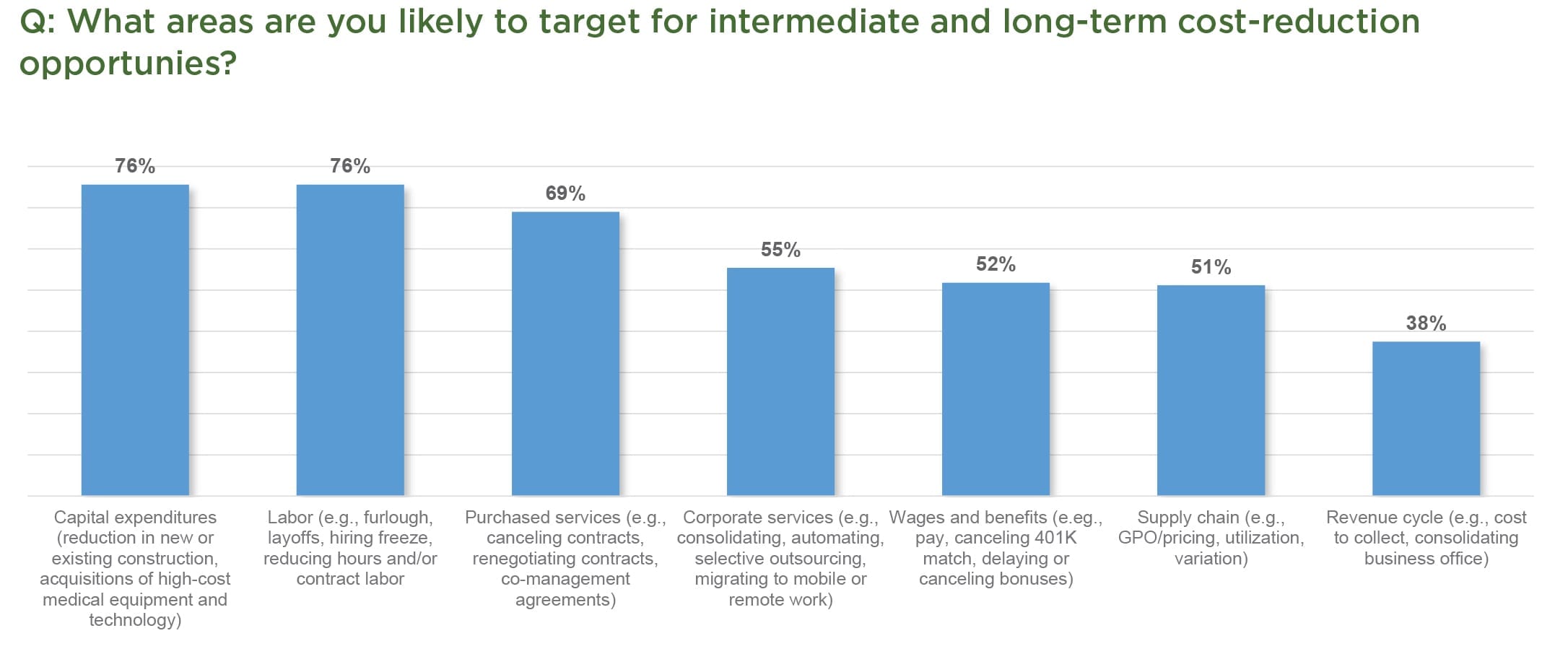

To offset the financial impact from COVID-19, providers are looking at specific areas to rein in their expenses. When asked what areas they are cutting back on the most, 76% of Guidehouse’s survey respondents indicated capital expenditure, including high-cost medical equipment and technology like robotics, and labor costs. Nearly seven out of 10 respondents noted that they’re canceling or renegotiating purchased services contracts and co-management agreements, while about half are examining supply chain expenses, including GPO pricing, utilization and variation. Respondents’ ranking of the seven areas of cost-reduction opportunities can be found in Exhibit 3.

Exhibit 3: Hospital Cost-Reduction Opportunities (Click to enlarge)

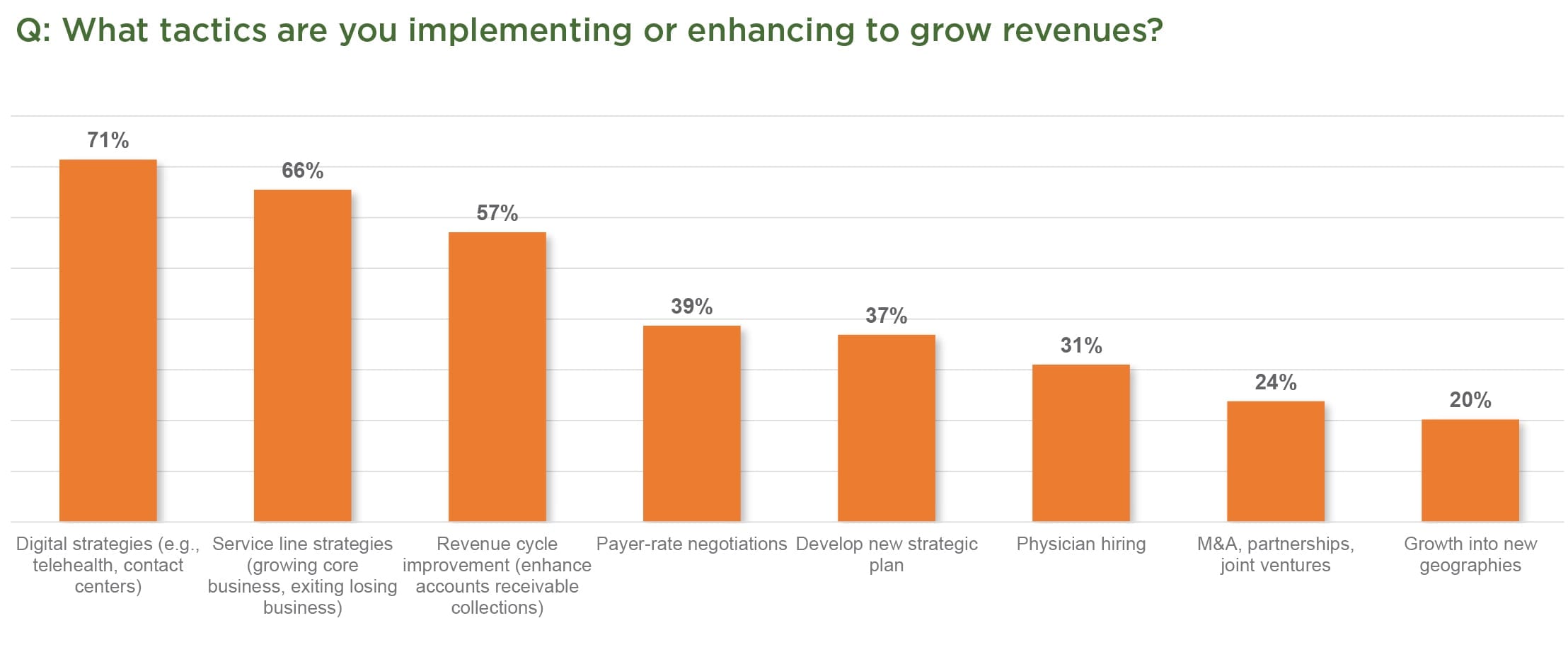

As Dr. Peck noted, providers are looking ahead to determine the best business strategies to drive revenue. When asked what tactics they’re implementing to enhance and grow revenue, 71% of survey respondents, unsurprisingly, mentioned digital strategies like telehealth and contact centers. Telehealth services are largely expected to continue, with 67% of the survey respondents indicating that their organizations will use telehealth at least five times more than they did pre-pandemic.

Second on the list of tactics to grow revenue was a focus on service line strategies, such as growing core businesses and exiting losing businesses. The full list or revenue opportunities is shown in Exhibit 4.

Exhibit 4: Hospital Tactics for Enhancing or Growing Revenue (Click to enlarge)

Orthopedics remains one of the more lucrative specialties for hospitals. Companies that understand how their provider customers are prioritizing orthopedic care could be better prepared to respond.

Advice for Orthopedic Companies

COVID-19 is forcing hospitals to rethink numerous aspects about their business, including their digital strategies, infrastructure, business models, vendor contracts and even M&A. To the latter point, 29% of Guidehouse’s survey respondents said that the pandemic has increased the likelihood of their organization participating in M&A activity or seek new partnerships.

A lesson learned from COVID-19 is that the pandemic is not impacting the U.S. equally—some states and cities have the virus controlled, while others remain hot spots for spread. Orthopedic companies will need to remain nimble in their day-to-day and long-term response to hospital needs, Dr. Peck said.

Of course, most orthopedic companies need to apply this flexibility globally. Dr. Peck advised prioritizing provider customers in stable COVID regions.

“Stay patient and flexible and expect different geographies to go at different speeds,” Dr. Peck said about working with hospitals. “Focus resources on geographies where COVID is stable or in larger facilities where they have the resources to both treat COVID and elective surgery safely and efficiently.”

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer.

Elective procedures resumed in late second quarter for most of the U.S., allowing hospitals to begin to revive their more lucrative revenue lines. But as the U.S. contends with the continued spread of COVID-19, hospitals maintain a grim outlook for 2020 and into 2021.

Like most businesses, U.S. providers are making difficult decisions about...

Elective procedures resumed in late second quarter for most of the U.S., allowing hospitals to begin to revive their more lucrative revenue lines. But as the U.S. contends with the continued spread of COVID-19, hospitals maintain a grim outlook for 2020 and into 2021.

Like most businesses, U.S. providers are making difficult decisions about their spending and strategies, said Chuck Peck, M.D., a Partner at Guidehouse and former President and CEO of Piedmont Athens Regional Medical Center in Georgia. Orthopedic companies will be better prepared to respond to their customers by understanding the business measures that hospitals are taking.

Dr. Peck shared analysis from Guidehouse’s COVID-19 Hospital & Health System Survey, which asked 174 executives in May about the pandemic’s impact on revenue, elective procedure volumes and strategies such as telehealth. In analyzing the survey response, Dr. Peck said, “Through all the uncertainty COVID-19 has presented, one thing hospitals and health systems can be certain of is that their business models will not return to what they were pre-pandemic.”

Hospitals Expect Double Digit Revenue Loss

Not surprisingly, nine out of 10 executives that took Guidehouse’s survey said that they expect their organizations’ revenue to be lower at the end of 2020 than it was pre-COVID. Nearly two-thirds expect revenue to decrease by 15% or more in 2020 and one in five project revenue to decrease by 30% or more in 2020. Exhibit 1 details 2020 revenue compared to pre-COVID revenue.

Exhibit 1: 2020 vs. Pre-Pandemic Revenue (Click to enlarge)

The American Hospital Association quantified providers’ revenue losses for the first four months of the pandemic. It estimated that from March 1 to June 30, U.S. hospitals and health systems lost $202.6 billion. Canceled surgeries, outpatient treatment and reduced emergency department services resulted in a loss of $161.4 billion for U.S. non-federal hospitals, according to the association.

Hospitals are balancing the decrease in revenue with an increase in costs associated with COVID-19, everything from PPE to virtual health platforms. While the U.S. federal government announced billions of dollars in aid to hospitals, Guidehouse’s survey found that only 11% of executive respondents believed that the money would be enough to cover additional expenses from COVID-19.

Still, executives expect their hospitals and health systems to see an increase in revenue in the second half of the year and into 2021, as elective procedure volume builds and patients return to receive routine care.

“On the positive side, executives expect the long-term view won’t be as grim, foreseeing only 3% lower revenue one year from now,” Dr. Peck said.

Procedure Volume Outlook

In the middle of July, analysts noted that about 90% of the U.S. was open for elective procedures. While it’s unlikely that we’ll see the nearly nationwide halt of elective procedures again, until the virus is suppressed, we expect that procedures will stop at local levels when cities face large COVID outbreaks.

“In some hot spots, hospitals have started closing down elective surgeries again,” Dr. Peck said. “In others, even though the COVID caseload continues to be high, organizations feel comfortable that they have enough PPE, testing and tracing to continue with elective surgeries they already opened several months ago.”

U.S. hospitals have turned their focus, Peck said, to how long it will take procedures to return to pre-COVID levels.

Guidehouse’s survey, which took into account all elective procedures, found that half of respondents thought it would take through the end of 2020 or longer for procedure volumes to return to pre-COVID levels. Exhibit 2 highlights the length of time executives said it would take for their organizations to ramp up procedures.

Exhibit 2: Elective Procedures Anticipated Return to Pre-COVID Levels (Click to enlarge)

Orthopedic surgeons echoed a similar sentiment. In a survey taken by 1,523 members of the American Academy of Orthopaedic Surgeons, 70% of surgeons thought that it would take five months after procedures resume to regain 90% of pre-COVID surgical volume.

Based on these assertions from hospitals and surgeons and commentary from orthopedic companies, we do not foresee orthopedic procedures returning to pre-COVID volume in 2020.

What is the Impact to Hospitals?

As hospitals balance revenue loss with an increase in expenses from COVID patients, they’re making short- and long-term decisions that could impact orthopedic companies.

“Although healthcare organizations remain focused on managing the day-to-day realities of COVID-19, they are also eyeing the future and thinking through how the crisis will impact them clinically, financially and operationally,” Dr. Peck said.

To offset the financial impact from COVID-19, providers are looking at specific areas to rein in their expenses. When asked what areas they are cutting back on the most, 76% of Guidehouse’s survey respondents indicated capital expenditure, including high-cost medical equipment and technology like robotics, and labor costs. Nearly seven out of 10 respondents noted that they’re canceling or renegotiating purchased services contracts and co-management agreements, while about half are examining supply chain expenses, including GPO pricing, utilization and variation. Respondents’ ranking of the seven areas of cost-reduction opportunities can be found in Exhibit 3.

Exhibit 3: Hospital Cost-Reduction Opportunities (Click to enlarge)

As Dr. Peck noted, providers are looking ahead to determine the best business strategies to drive revenue. When asked what tactics they’re implementing to enhance and grow revenue, 71% of survey respondents, unsurprisingly, mentioned digital strategies like telehealth and contact centers. Telehealth services are largely expected to continue, with 67% of the survey respondents indicating that their organizations will use telehealth at least five times more than they did pre-pandemic.

Second on the list of tactics to grow revenue was a focus on service line strategies, such as growing core businesses and exiting losing businesses. The full list or revenue opportunities is shown in Exhibit 4.

Exhibit 4: Hospital Tactics for Enhancing or Growing Revenue (Click to enlarge)

Orthopedics remains one of the more lucrative specialties for hospitals. Companies that understand how their provider customers are prioritizing orthopedic care could be better prepared to respond.

Advice for Orthopedic Companies

COVID-19 is forcing hospitals to rethink numerous aspects about their business, including their digital strategies, infrastructure, business models, vendor contracts and even M&A. To the latter point, 29% of Guidehouse’s survey respondents said that the pandemic has increased the likelihood of their organization participating in M&A activity or seek new partnerships.

A lesson learned from COVID-19 is that the pandemic is not impacting the U.S. equally—some states and cities have the virus controlled, while others remain hot spots for spread. Orthopedic companies will need to remain nimble in their day-to-day and long-term response to hospital needs, Dr. Peck said.

Of course, most orthopedic companies need to apply this flexibility globally. Dr. Peck advised prioritizing provider customers in stable COVID regions.

“Stay patient and flexible and expect different geographies to go at different speeds,” Dr. Peck said about working with hospitals. “Focus resources on geographies where COVID is stable or in larger facilities where they have the resources to both treat COVID and elective surgery safely and efficiently.”

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.