Copy to clipboard

Copy to clipboard

Sales from arthroscopy/soft tissue repair products in 2017 surpassed $5.3 billion and grew 6.2% vs. 2016, according to our estimates published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The segment exceeded our projections, partially due to better-than-expected growth by players like DePuy Synthes, Stryker and Zimmer Biomet.

The top-tier players have invested in the space through R&D and acquisitions in recent years, and their ability to expand the market or take share from the dominant leaders, Arthrex and Smith & Nephew, will be worth watching in the coming years. We direct you to Exhibit 1 for a closer look at individual company and total market performance.

Exhibit 1A: Arthroscopy/Soft Tissue Sales Performance: Top Players and All Others ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Arthrex | $1,732.5 | $1,540.0 | $192.5 | 12.5% |

| Smith & Nephew | $1,243.0 | $1,218.0 | $25.0 | 2.1% |

| DePuy Synthes | $710.5 | $696.4 | $14.1 | 2.0% |

| Stryker | $494.0 | $461.5 | $32.5 | 7.0% |

| ConMed | $429.0 | $422.2 | $6.8 | 1.6% |

| Zimmer Biomet | $129.4 | $124.2 | $5.2 | 4.2% |

| Karl Storz | $114.6 | $109.1 | $5.5 | 5.0% |

| ~120 companies with revenue below $99MM | $465.5 | $438.3 | $27.2 | 6.2% |

| Total | $5,318.5 | $5,009.7 | $308.8 | 6.2% |

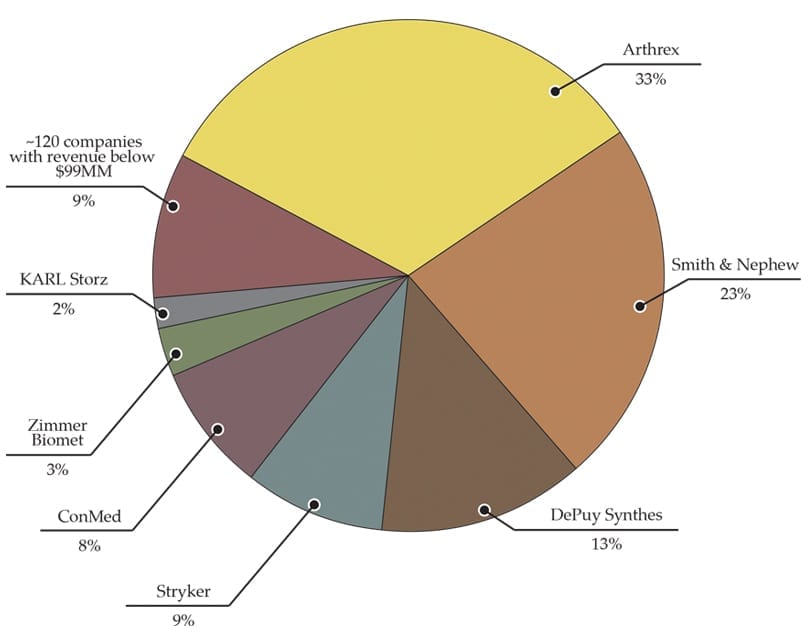

Exhibit 1B: Arthroscopy/Soft Tissue Market Share: Top Players and All Others

To provide perspective on three of the top players:

Our estimates conclude that Arthrex controls one-third of the arthroscopy/soft tissue market and continues to experience sales at double the market growth rate. Among the products for which Arthrex received 510(k) clearances in 2017 and 1H18 were anchors and screws for the foot, knee and shoulder, including the Knotless SutureTak Anchor, NanoSuture Anchor and PushLock Anchor.

Smith & Nephew, the second-largest player in the segment, experienced softer growth in 2017 due to lower-than-expected adoption of its legacy resection and radiofrequency products—a challenge that the company continued to cite in its 1Q18 earnings call. The company expects 2018 to be stronger, with rollouts of its LENS visualization and WEREWOLF COBLATION products, as well as Rotation Medical’s tissue regeneration product for rotator cuff, which Smith & Nephew purchased in 4Q17. In 1Q18, Smith & Nephew posted arthroscopy/soft tissue revenue of $322.0 million, +4.7% vs. 1Q17.

Of note, in 4Q17, ConMed returned to growth for the first time in seven quarters, posting U.S. sales up 5.3% and international up 10.5% vs. 4Q16. New product rollouts (more expected in 3Q) and tuck-in acquisitions have been a part of their growth story, including the acquisitions of KFx Medical’s AppianFx soft tissue fixation and MedShape’s ExoShape Anterior Cruciate Ligament fixation. ConMed posted 1Q18 revenue of $108.9 million, +4.9% vs. 1Q17.

We project that the arthroscopy/soft tissue market will continue to grow in the 6% range for each of the next five years. Medium and small orthopaedic companies will expand their portfolios to include complementary devices that meet the needs of sports medicine surgeons, and larger companies will make acquisitions. Specifically, the following forces will play a role in the segment’s growth:

- Patient demographics are suitable to grow the arthroscopy/soft tissue market, as younger, more active folks seek interventional procedures to keep them mobile prior to joint reconstruction.

- The top-tier players are committed to expanding their portfolios, whether through their own R&D efforts or bolt-on acquisitions. In recent years, we’ve stated that the more product-diverse companies see the segment as complementary to other product lines like joint reconstruction, e.g. Zimmer Biomet’s Subchondroplasty and Wright Medical’s 2018 license agreement with KFx Medical for knotless rotator cuff repair. Conversely, in 2017, Arthrex received regulatory clearance for its own total knee and total shoulder products. This point is magnified by a suggestion by shoulder surgeon C. Scott Humphrey (See below), that the move of total joint arthroplasty to ASCs could benefit surgeon owners, who are losing money on arthroscopy.

- The segment remains ripe for acquisitions of novel technologies developed by startups. Companies span the spectrum in this space, from Cartiva and its PMA synthetic cartilage implant to treat arthritis in the great toe to Trice Medical’s mi-eye diagnostic equipment. ConMed, DePuy Synthes, Smith & Nephew, Stryker and Zimmer Biomet have purchased companies in the last two years to boost their positions.

- Companies have begun to emphasize expansion beyond traditional arthroscopy/soft tissue products toward an integrated experience in and out of the operating room, like Arthrex’s Synergy and all-in-one platforms like Smith & Nephew’s LENS and Stryker’s 1588 AIM Platform, both cited in earnings calls as growth drivers. As companies seek to maintain or boost revenue in this segment, it’s our expectation that they will look for ways to make the surgeon experience more enhanced and efficient.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

| Surgeon Cites Low-Cost Implants, Orthobiologics and Total Joint as Future of Arthroscopy Narrative Editor’s Note: To understand current and future trends in the arthroscopy/soft tissue market, we asked C. Scott Humphrey, M.D., Founder of the Humphrey Shoulder Clinic, to share his perspective as a clinician. He believes that the space is healthy, and an improved economy has led to more well-insured patients. His comments on product trends and market forces follow. Product Trends The current mechanical devices, such as suture anchors, arthroscopy towers, etc., work well. From my perspective as a surgeon, as little as five years ago providers might have worried that lower-cost implants might lead to inferior clinical results. Now there are many high-quality implant and instrumentation options available to surgeons, surgery centers and hospitals at various price points. At this point in time, I don’t feel that choosing the less expensive products is going to negatively affect patient outcomes. So, we are seeing commoditization of many of these products. Better, faster, simpler and less expensive implant technology is always welcome. But companies in this space will likely be competing based on price and service, rather than wowing surgeons with new innovation. For the last 10+ years, many have believed that biologics/soft tissues were the future for the orthopaedic industry. Perhaps this will be true, but we are still waiting for long-term outcomes studies to confirm the efficacy of many procedures that utilize these recently-developed biologic products. Until the clinical results of these products are proven, insurance payors and hospitals will continue to be skeptical and resist paying for them. The day is nearing when we will see who amongst those that invested in various orthobiologic technologies will be high-fiving one another, or perhaps cursing the day that they invested in what turned out to be well-intentioned pixie dust. Market Forces Several market forces will impact this space over the next five years—one of the biggest is surgeon incentives. There is a trend of orthopaedic surgeons migrating from private practice to hospital employment. When this occurs, surgeon motivations change. Hospital administrators often place their employed surgeons on committees with the goal of standardizing O.R. equipment and implants in order to control costs. From my observations, this leads to a limited number of vendors in the O.R. As a result, it becomes much harder for newer, smaller companies to get their products into the hospitals. This has the potential to hinder advancement in the field, since it is the small, agile companies that have historically been big drivers of innovation. On a positive note, the gradual acceptance of total joint arthroplasty as an outpatient procedure has most ambulatory surgery center owners excited. While reimbursement for most arthroscopic and sports medicine procedures has slowly declined, outpatient arthroplasty might provide a means for ASC owners to make up for the loss. Improvements in post-operative pain management will allow surgeons to perform more complex cases on an outpatient basis, and this should create opportunity for ASCs and for companies that strive to produce products that will help ASCs make the transition. On a related note, given the national drive to address the opioid crisis, there is likely a bright future for products that will facilitate postoperative pain management without use of narcotics. |

Sales from arthroscopy/soft tissue repair products in 2017 surpassed $5.3 billion and grew 6.2% vs. 2016, according to our estimates published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The segment exceeded our projections, partially due to better-than-expected growth by players like DePuy Synthes, Stryker and Zimmer Biomet.

The...

Sales from arthroscopy/soft tissue repair products in 2017 surpassed $5.3 billion and grew 6.2% vs. 2016, according to our estimates published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The segment exceeded our projections, partially due to better-than-expected growth by players like DePuy Synthes, Stryker and Zimmer Biomet.

The top-tier players have invested in the space through R&D and acquisitions in recent years, and their ability to expand the market or take share from the dominant leaders, Arthrex and Smith & Nephew, will be worth watching in the coming years. We direct you to Exhibit 1 for a closer look at individual company and total market performance.

Exhibit 1A: Arthroscopy/Soft Tissue Sales Performance: Top Players and All Others ($Millions)

| 2017 | 2016 | $ Change | % Change | |

| Arthrex | $1,732.5 | $1,540.0 | $192.5 | 12.5% |

| Smith & Nephew | $1,243.0 | $1,218.0 | $25.0 | 2.1% |

| DePuy Synthes | $710.5 | $696.4 | $14.1 | 2.0% |

| Stryker | $494.0 | $461.5 | $32.5 | 7.0% |

| ConMed | $429.0 | $422.2 | $6.8 | 1.6% |

| Zimmer Biomet | $129.4 | $124.2 | $5.2 | 4.2% |

| Karl Storz | $114.6 | $109.1 | $5.5 | 5.0% |

| ~120 companies with revenue below $99MM | $465.5 | $438.3 | $27.2 | 6.2% |

| Total | $5,318.5 | $5,009.7 | $308.8 | 6.2% |

Exhibit 1B: Arthroscopy/Soft Tissue Market Share: Top Players and All Others

To provide perspective on three of the top players:

Our estimates conclude that Arthrex controls one-third of the arthroscopy/soft tissue market and continues to experience sales at double the market growth rate. Among the products for which Arthrex received 510(k) clearances in 2017 and 1H18 were anchors and screws for the foot, knee and shoulder, including the Knotless SutureTak Anchor, NanoSuture Anchor and PushLock Anchor.

Smith & Nephew, the second-largest player in the segment, experienced softer growth in 2017 due to lower-than-expected adoption of its legacy resection and radiofrequency products—a challenge that the company continued to cite in its 1Q18 earnings call. The company expects 2018 to be stronger, with rollouts of its LENS visualization and WEREWOLF COBLATION products, as well as Rotation Medical’s tissue regeneration product for rotator cuff, which Smith & Nephew purchased in 4Q17. In 1Q18, Smith & Nephew posted arthroscopy/soft tissue revenue of $322.0 million, +4.7% vs. 1Q17.

Of note, in 4Q17, ConMed returned to growth for the first time in seven quarters, posting U.S. sales up 5.3% and international up 10.5% vs. 4Q16. New product rollouts (more expected in 3Q) and tuck-in acquisitions have been a part of their growth story, including the acquisitions of KFx Medical’s AppianFx soft tissue fixation and MedShape’s ExoShape Anterior Cruciate Ligament fixation. ConMed posted 1Q18 revenue of $108.9 million, +4.9% vs. 1Q17.

We project that the arthroscopy/soft tissue market will continue to grow in the 6% range for each of the next five years. Medium and small orthopaedic companies will expand their portfolios to include complementary devices that meet the needs of sports medicine surgeons, and larger companies will make acquisitions. Specifically, the following forces will play a role in the segment’s growth:

- Patient demographics are suitable to grow the arthroscopy/soft tissue market, as younger, more active folks seek interventional procedures to keep them mobile prior to joint reconstruction.

- The top-tier players are committed to expanding their portfolios, whether through their own R&D efforts or bolt-on acquisitions. In recent years, we’ve stated that the more product-diverse companies see the segment as complementary to other product lines like joint reconstruction, e.g. Zimmer Biomet’s Subchondroplasty and Wright Medical’s 2018 license agreement with KFx Medical for knotless rotator cuff repair. Conversely, in 2017, Arthrex received regulatory clearance for its own total knee and total shoulder products. This point is magnified by a suggestion by shoulder surgeon C. Scott Humphrey (See below), that the move of total joint arthroplasty to ASCs could benefit surgeon owners, who are losing money on arthroscopy.

- The segment remains ripe for acquisitions of novel technologies developed by startups. Companies span the spectrum in this space, from Cartiva and its PMA synthetic cartilage implant to treat arthritis in the great toe to Trice Medical’s mi-eye diagnostic equipment. ConMed, DePuy Synthes, Smith & Nephew, Stryker and Zimmer Biomet have purchased companies in the last two years to boost their positions.

- Companies have begun to emphasize expansion beyond traditional arthroscopy/soft tissue products toward an integrated experience in and out of the operating room, like Arthrex’s Synergy and all-in-one platforms like Smith & Nephew’s LENS and Stryker’s 1588 AIM Platform, both cited in earnings calls as growth drivers. As companies seek to maintain or boost revenue in this segment, it’s our expectation that they will look for ways to make the surgeon experience more enhanced and efficient.

Carolyn LaWell is ORTHOWORLD’s Chief Content Officer. She can be reached by email.

| Surgeon Cites Low-Cost Implants, Orthobiologics and Total Joint as Future of Arthroscopy Narrative Editor’s Note: To understand current and future trends in the arthroscopy/soft tissue market, we asked C. Scott Humphrey, M.D., Founder of the Humphrey Shoulder Clinic, to share his perspective as a clinician. He believes that the space is healthy, and an improved economy has led to more well-insured patients. His comments on product trends and market forces follow. Product Trends The current mechanical devices, such as suture anchors, arthroscopy towers, etc., work well. From my perspective as a surgeon, as little as five years ago providers might have worried that lower-cost implants might lead to inferior clinical results. Now there are many high-quality implant and instrumentation options available to surgeons, surgery centers and hospitals at various price points. At this point in time, I don’t feel that choosing the less expensive products is going to negatively affect patient outcomes. So, we are seeing commoditization of many of these products. Better, faster, simpler and less expensive implant technology is always welcome. But companies in this space will likely be competing based on price and service, rather than wowing surgeons with new innovation. For the last 10+ years, many have believed that biologics/soft tissues were the future for the orthopaedic industry. Perhaps this will be true, but we are still waiting for long-term outcomes studies to confirm the efficacy of many procedures that utilize these recently-developed biologic products. Until the clinical results of these products are proven, insurance payors and hospitals will continue to be skeptical and resist paying for them. The day is nearing when we will see who amongst those that invested in various orthobiologic technologies will be high-fiving one another, or perhaps cursing the day that they invested in what turned out to be well-intentioned pixie dust. Market Forces Several market forces will impact this space over the next five years—one of the biggest is surgeon incentives. There is a trend of orthopaedic surgeons migrating from private practice to hospital employment. When this occurs, surgeon motivations change. Hospital administrators often place their employed surgeons on committees with the goal of standardizing O.R. equipment and implants in order to control costs. From my observations, this leads to a limited number of vendors in the O.R. As a result, it becomes much harder for newer, smaller companies to get their products into the hospitals. This has the potential to hinder advancement in the field, since it is the small, agile companies that have historically been big drivers of innovation. On a positive note, the gradual acceptance of total joint arthroplasty as an outpatient procedure has most ambulatory surgery center owners excited. While reimbursement for most arthroscopic and sports medicine procedures has slowly declined, outpatient arthroplasty might provide a means for ASC owners to make up for the loss. Improvements in post-operative pain management will allow surgeons to perform more complex cases on an outpatient basis, and this should create opportunity for ASCs and for companies that strive to produce products that will help ASCs make the transition. On a related note, given the national drive to address the opioid crisis, there is likely a bright future for products that will facilitate postoperative pain management without use of narcotics. |

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

CL

Carolyn LaWell is ORTHOWORLD's Chief Content Officer. She joined ORTHOWORLD in 2012 to oversee its editorial and industry education. She previously served in editor roles at B2B magazines and newspapers.