Copy to clipboard

Copy to clipboard

Worldwide orthopaedic product sales reached $46.6 billion in 2015, an increase of 1.2 percent over 2014, according to ORTHOWORLD® estimates. The numbers cited in the latest installment of THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® show that industry growth slowed from the two to three percent range in recent years due to various economic and industry factors.

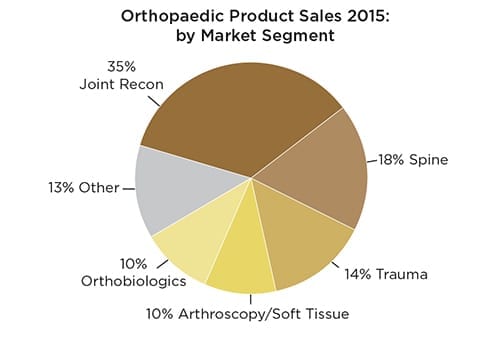

First, pressure on product pricing affected the larger segments of joint reconstruction and spine as purchasing power continued to shift from surgeons to public and private payors. Second, regulatory scrutiny continued to play out, impacting R&D investments and product launches. Neither of these factors are new, and hence are part of daily business in orthopaedics. Still, they directly influence the top line. As is outlined in the Annual Report, companies are positioning themselves to profitably respond to these headwinds.

First, pressure on product pricing affected the larger segments of joint reconstruction and spine as purchasing power continued to shift from surgeons to public and private payors. Second, regulatory scrutiny continued to play out, impacting R&D investments and product launches. Neither of these factors are new, and hence are part of daily business in orthopaedics. Still, they directly influence the top line. As is outlined in the Annual Report, companies are positioning themselves to profitably respond to these headwinds.

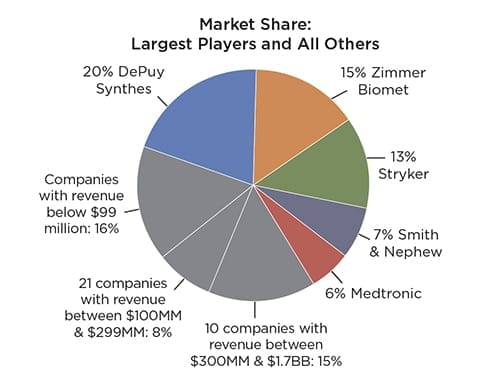

Third, international currencies were weaker than the U.S. dollar, and emerging markets like Brazil and China experienced softer growth than in years past. This directly impacted the as-reported sales performance of many of the large- and mid-tier global companies. The industry’s five largest players by revenue—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew and Medtronic—derive between 30 percent and 50 percent of their sales from international markets.

Third, international currencies were weaker than the U.S. dollar, and emerging markets like Brazil and China experienced softer growth than in years past. This directly impacted the as-reported sales performance of many of the large- and mid-tier global companies. The industry’s five largest players by revenue—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew and Medtronic—derive between 30 percent and 50 percent of their sales from international markets.

These five companies account for 61 percent of total orthopaedic sales; therefore, their performance heavily weights industry growth.

In spite of these factors, demographics alone continue to support the need for musculoskeletal treatments worldwide. This is evidenced by the fact that the majority of mid-sized and small companies grew at a faster pace than the industry as a whole.

Worldwide orthopaedic product sales reached $46.6 billion in 2015, an increase of 1.2 percent over 2014, according to ORTHOWORLD® estimates. The numbers cited in the latest installment of THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® show that industry growth slowed from the two to three percent range in recent years due to various economic and...

Worldwide orthopaedic product sales reached $46.6 billion in 2015, an increase of 1.2 percent over 2014, according to ORTHOWORLD® estimates. The numbers cited in the latest installment of THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT® show that industry growth slowed from the two to three percent range in recent years due to various economic and industry factors.

First, pressure on product pricing affected the larger segments of joint reconstruction and spine as purchasing power continued to shift from surgeons to public and private payors. Second, regulatory scrutiny continued to play out, impacting R&D investments and product launches. Neither of these factors are new, and hence are part of daily business in orthopaedics. Still, they directly influence the top line. As is outlined in the Annual Report, companies are positioning themselves to profitably respond to these headwinds.

Third, international currencies were weaker than the U.S. dollar, and emerging markets like Brazil and China experienced softer growth than in years past. This directly impacted the as-reported sales performance of many of the large- and mid-tier global companies. The industry’s five largest players by revenue—DePuy Synthes, Zimmer Biomet, Stryker, Smith & Nephew and Medtronic—derive between 30 percent and 50 percent of their sales from international markets.

These five companies account for 61 percent of total orthopaedic sales; therefore, their performance heavily weights industry growth.

In spite of these factors, demographics alone continue to support the need for musculoskeletal treatments worldwide. This is evidenced by the fact that the majority of mid-sized and small companies grew at a faster pace than the industry as a whole.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

JV

Julie Vetalice is ORTHOWORLD's Editorial Assistant. She has covered the orthopedic industry for over 20 years, having joined the company in 1999.