Copy to clipboard

Copy to clipboard

Spine is the largest individual segment that we track, accounting for 18.2% of the orthopedic industry’s overall revenue. Excluding biologics, sales of orthopedic spine products topped $9.3 billion in 2018, growing +2.7% vs. 2017. Growth in the segment exceeded our expectations, as several companies in the top 10 posted double-digit increases that offset lower performance by manufacturers at the top of the list.

Let’s take a deeper look at past, present and forecasted performance.

Mid-tier Players Experience Faster Growth, Take Market Share

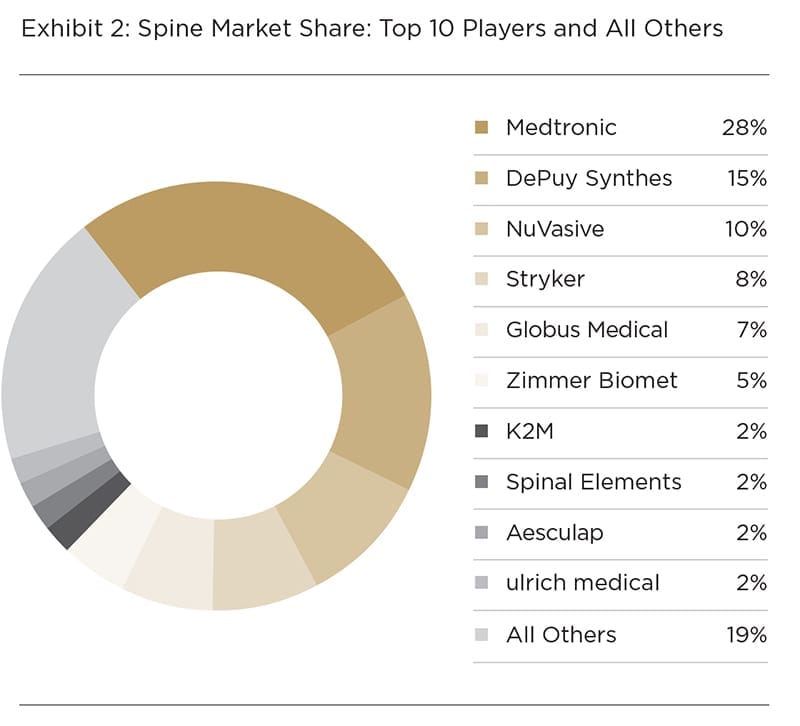

Exhibit 1 and Exhibit 2 show 2018 spine sales for players with revenue over $60 million, as well as the market share for the top ten players. The top two, Medtronic and DePuy Synthes, each notched revenue above $1 billion and accounted for nearly 43% of the entire spine market. Sales for these top two players decreased -2% vs. 2017.

Medtronic improved incrementally over 2017, but still fell short of market growth. Company leadership is encouraged, though, as they believe that strong Mazor robotic sales bodes well for the future growth rate of implant purchases. The spine segment has been a chronic underperformer for DePuy Synthes for several years, but 2018 was particularly difficult as the backslide hit high single digits.

Medtronic improved incrementally over 2017, but still fell short of market growth. Company leadership is encouraged, though, as they believe that strong Mazor robotic sales bodes well for the future growth rate of implant purchases. The spine segment has been a chronic underperformer for DePuy Synthes for several years, but 2018 was particularly difficult as the backslide hit high single digits.

The next tier of companies includes a broad revenue range spanning $50 million to $999 million, comprising 42% of the market by total revenue. These companies grew at three times the market rate, with 2018 stand-out performances by NuVasive, Stryker, Globus Medical, Spinal Elements and ulrich Medical. Zimmer Biomet restructured their spine business in 2018 while pursuing growth, colorfully describing the process as driving a car down the street while changing the fan belt.

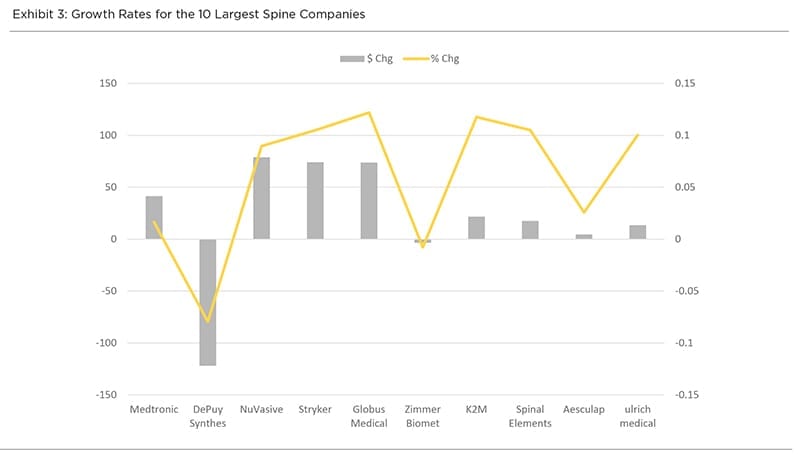

Exhibit 3 shows the relationship of absolute revenue and percentage growth for 2018. As previously mentioned, while the segment lacked strong growth at the top end, NuVasive, Stryker and Globus Medical represent a fast-growing core that drove spine sales above our 2017 projection.

In general, spine-focused companies performed far better (+5.2%) than their diversified competitors (-1.3%) in 2018 vs. 2017. Stryker was the only diversified company to manage strong spine growth, and stands to further improve its position via the November 2018 acquisition of K2M. The transaction gave Stryker an immediate upgrade to its spine portfolio, as well as an R&D engine with a steady flow of new products. Company leadership pointed to the minimal customer overlap between the two salesforces. Stryker’s ability to manage a smooth integration will play a key role in determining how much the gap with NuVasive can be closed in 2019.

In general, spine-focused companies performed far better (+5.2%) than their diversified competitors (-1.3%) in 2018 vs. 2017. Stryker was the only diversified company to manage strong spine growth, and stands to further improve its position via the November 2018 acquisition of K2M. The transaction gave Stryker an immediate upgrade to its spine portfolio, as well as an R&D engine with a steady flow of new products. Company leadership pointed to the minimal customer overlap between the two salesforces. Stryker’s ability to manage a smooth integration will play a key role in determining how much the gap with NuVasive can be closed in 2019.

A Look at 2019 and Beyond

The top 10 public companies saw high-single-digit growth in the spine segment in the first quarter of 2019, as shown in Exhibit 4. Medtronic’s core spine business was down -1.1% for the quarter, but was offset by the 26 Mazor X systems sold. NuVasive’s growth was driven by U.S. hardware sales of new products launched in late 2018. Stryker’s integration of K2M is proceeding to expectations, with spine sales growing 2% on a combined company basis. Globus’ double-digit growth was driven by new products and upselling through ExcelsiusGPS.

We project the spine segment to hold steady in the mid-2% growth range through 2023. The weight and lack of below-market growth from Medtronic, DePuy Synthes and Zimmer Biomet in recent years will continue to hinder growth rates overall in the segment. Together these three companies control 48% of the spine market, but continue to post inconsistent revenue.

Players at the top of the next revenue tier, NuVasive, Stryker and Globus Medical, hold 25% of the spine market with an opportunity to take more share in 2019. All three continued positive performance trends in 1Q19, and we expect that momentum to continue based on upcoming product launches. NuVasive has announced that a new robotics platform will be integrated with their Pulse navigation technology, Stryker broadened its portfolio through the acquisition of K2M and Globus Medical took steps to expand the features and versatility of their ExcelsiusGPS robotic system. These players, together with smaller companies innovating through materials science, manufacturing techniques and new procedural approaches, will sustain the growth of the segment. SI-BONE is projected to reach our $60 million+ tier in 2019, and is an example of companies looking for innovation and revenue opportunities in specialty or adjacent submarkets.

Much of the data shared here was originally published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®, a Member benefit. Download your copy to learn more about spine trends and players.

Mike Evers is ORTHOWORLD’s Market Analyst.

Spine is the largest individual segment that we track, accounting for 18.2% of the orthopedic industry’s overall revenue. Excluding biologics, sales of orthopedic spine products topped $9.3 billion in 2018, growing +2.7% vs. 2017. Growth in the segment exceeded our expectations, as several companies in the top 10 posted double-digit increases...

Spine is the largest individual segment that we track, accounting for 18.2% of the orthopedic industry’s overall revenue. Excluding biologics, sales of orthopedic spine products topped $9.3 billion in 2018, growing +2.7% vs. 2017. Growth in the segment exceeded our expectations, as several companies in the top 10 posted double-digit increases that offset lower performance by manufacturers at the top of the list.

Let’s take a deeper look at past, present and forecasted performance.

Mid-tier Players Experience Faster Growth, Take Market Share

Exhibit 1 and Exhibit 2 show 2018 spine sales for players with revenue over $60 million, as well as the market share for the top ten players. The top two, Medtronic and DePuy Synthes, each notched revenue above $1 billion and accounted for nearly 43% of the entire spine market. Sales for these top two players decreased -2% vs. 2017.

Medtronic improved incrementally over 2017, but still fell short of market growth. Company leadership is encouraged, though, as they believe that strong Mazor robotic sales bodes well for the future growth rate of implant purchases. The spine segment has been a chronic underperformer for DePuy Synthes for several years, but 2018 was particularly difficult as the backslide hit high single digits.

The next tier of companies includes a broad revenue range spanning $50 million to $999 million, comprising 42% of the market by total revenue. These companies grew at three times the market rate, with 2018 stand-out performances by NuVasive, Stryker, Globus Medical, Spinal Elements and ulrich Medical. Zimmer Biomet restructured their spine business in 2018 while pursuing growth, colorfully describing the process as driving a car down the street while changing the fan belt.

Exhibit 3 shows the relationship of absolute revenue and percentage growth for 2018. As previously mentioned, while the segment lacked strong growth at the top end, NuVasive, Stryker and Globus Medical represent a fast-growing core that drove spine sales above our 2017 projection.

In general, spine-focused companies performed far better (+5.2%) than their diversified competitors (-1.3%) in 2018 vs. 2017. Stryker was the only diversified company to manage strong spine growth, and stands to further improve its position via the November 2018 acquisition of K2M. The transaction gave Stryker an immediate upgrade to its spine portfolio, as well as an R&D engine with a steady flow of new products. Company leadership pointed to the minimal customer overlap between the two salesforces. Stryker’s ability to manage a smooth integration will play a key role in determining how much the gap with NuVasive can be closed in 2019.

A Look at 2019 and Beyond

The top 10 public companies saw high-single-digit growth in the spine segment in the first quarter of 2019, as shown in Exhibit 4. Medtronic’s core spine business was down -1.1% for the quarter, but was offset by the 26 Mazor X systems sold. NuVasive’s growth was driven by U.S. hardware sales of new products launched in late 2018. Stryker’s integration of K2M is proceeding to expectations, with spine sales growing 2% on a combined company basis. Globus’ double-digit growth was driven by new products and upselling through ExcelsiusGPS.

We project the spine segment to hold steady in the mid-2% growth range through 2023. The weight and lack of below-market growth from Medtronic, DePuy Synthes and Zimmer Biomet in recent years will continue to hinder growth rates overall in the segment. Together these three companies control 48% of the spine market, but continue to post inconsistent revenue.

Players at the top of the next revenue tier, NuVasive, Stryker and Globus Medical, hold 25% of the spine market with an opportunity to take more share in 2019. All three continued positive performance trends in 1Q19, and we expect that momentum to continue based on upcoming product launches. NuVasive has announced that a new robotics platform will be integrated with their Pulse navigation technology, Stryker broadened its portfolio through the acquisition of K2M and Globus Medical took steps to expand the features and versatility of their ExcelsiusGPS robotic system. These players, together with smaller companies innovating through materials science, manufacturing techniques and new procedural approaches, will sustain the growth of the segment. SI-BONE is projected to reach our $60 million+ tier in 2019, and is an example of companies looking for innovation and revenue opportunities in specialty or adjacent submarkets.

Much of the data shared here was originally published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®, a Member benefit. Download your copy to learn more about spine trends and players.

Mike Evers is ORTHOWORLD’s Market Analyst.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.