Copy to clipboard

Copy to clipboard

The COVID-19 pandemic did little to slow the orthopedic market’s consolidation. We surveyed the orthopedic merger and acquisition market over the last six years to show why 2020 was a busy year and 2021 may be busier; why spine continues to dominate M&A transactions; and what has driven transactions so far in 2021.

These charts, and the data that generated them, are taken from our new M&A Tracker 1993-2021 that’s available for purchase in our store.

OVERALL TRENDS FOR 2016 TO 2021

Despite the impact of pandemic-related financial and business constraints, 2020 brought a brisk pace of mergers and acquisitions. We tracked 42 transactions for orthopedic device companies last year, as shown in Exhibit 1. Through the first half, 2021 is off to a slower start with 16 closed transactions compared to 19 at the same point the previous year. An unusually large number of deals (16) closed in the fourth quarter last year, nearly 40% of all 2020 transactions. The fourth quarter averaged closer to 10 deals in recent years, but we think the flurry of smaller acquisitions could elevate the totals again for 2021.

Exhibit 1: M&A Transactions by Year 2016 to YTD 2021

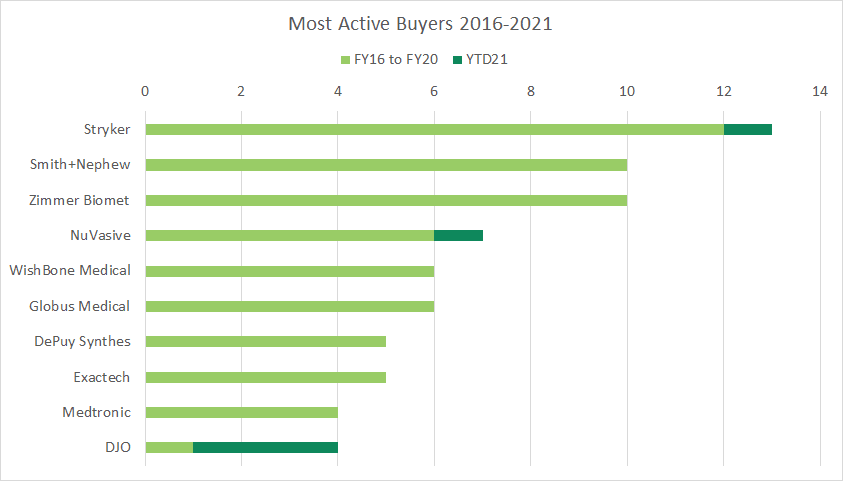

Companies in the $1 billion revenue tier dominate the M&A activity as they seek out new technologies and markets. Exhibit 2 shows that Stryker, Smith+Nephew and Zimmer Biomet have all completed at least 10 transactions since 2016.

Exhibit 2: Most Active Buyers 2016 to YTD 2021

DJO, powered by its parent company Colfax, burst into the ranking this year. The company already closed deals with Trilliant Surgical, MedShape and Mathys in 2021. Before the Mathys purchase, Colfax CEO Matthew Trerotola said, “There are bolt-ons and tuck-ins within that space that we can look at. We certainly have more flexibility now. Most of the things that we’re thinking about are in the small- to medium-size range in the short- to medium-term.”

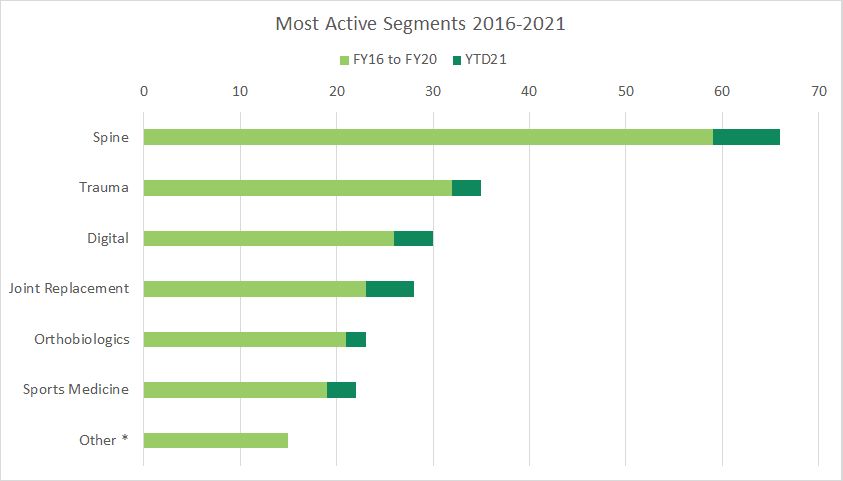

Speaking of large-cap medtech in general, Canaccord Genuity analyst Kyle Rose said there is a “paucity of true organic growth.” Therefore, M&A is a critical strategy to generate revenue. We believe that is particularly true in the spine segment. Hundreds of small companies play in the spine space, making it ripe for acquisitions. So much so, that spine accounted for 60+ or 30% of all transactions we’ve tracked since 2016 as shown in Exhibit 3.

Further activity in the spine market could be spurred as mid-tier players like Globus Medical, ATEC and Surgalign continue to take significant share and Zimmer Biomet divests it spine business.

Exhibit 3: Most Active Product Segments 2016 to YTD 2021

* Private equity firms, contract manufacturing, distributors, instruments, sterilization and O.R. products

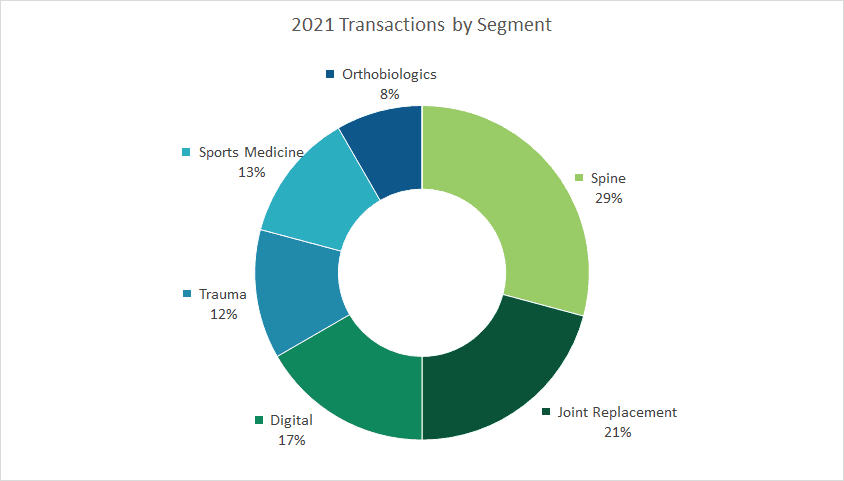

While the spine market remains the most active segment in 2021, as shown in Exhibit 4, there is fluidity in the other segments. Joint replacement has accelerated to 21% of all transactions compared to 14% for all of 2020. Trauma has fallen back to 12% from 25% last year. Transactions involving digital technology increased to 17% from just below 10% the prior year.

Exhibit 4: M&A Transactions by Segment YTD 2021

2021 TRANSACTIONS

Given the recovering market and commentary from executives, it seems reasonable to expect 2021 to finish with about 40 M&A transactions. While we don’t anticipate a deal the size of Stryker and Wright Medical for some time, we expect companies to remain aggressive in their acquisition search.

Doug Rice, CFO of Orthofix, said that the company was screening “more deals than ever” at the end of 2020.

Globus Medical has been quiet and certainly could make a splash. Globus Medical CEO Dave Demski said, “Yes, we are looking to be more aggressive there in terms of the amount we’re going to invest. We’re looking a little bit bigger. The emphasis is on expanding the differentiation within our portfolio. We’re looking for technology, not necessarily scale.”

Demski’s point about technology vs. scale is an interesting one. Viewed through that lens, the 16 transactions thus far in 2021 are roughly split down the middle.

Companies of all sizes are looking for complementary portfolio pieces and new markets. It is difficult to find a better recent example of a company deftly entering a new market than DJO. Since 2020, the company has rapidly stood up a dedicated foot-and-ankle business by investing $225 million. The addition of Mathys essentially doubles DJO’s international revenue.

Smaller players also seek similar opportunities through M&A. Through its merger with Kinos Medical, restor3d hopes to accelerate its entry into the U.S. foot and ankle market. Neo Medical acquired TriOs Medical to expand its footprint in the German and greater European markets. Implanet’s purchase of a majority stake in Orthopaedic & Spine Development will help the company achieve revenue critical mass to meet its “regulatory, clinical and economic demands.”

Like those seeking scale, companies along the revenue spectrum are finding ways to differentiate their offerings through acquisition. Enabling technology figures heavily in this category, most notably with mid-sized spine players as that segment rapidly shifts toward digital services. While COVID disrupted the timing of ATEC’s purchase of EOS imaging, the company now has a unique imaging tool to add to its AlphaInformatiX platform. SeaSpine initially partnered with 7D Surgical in 2020, but ultimately decided to purchase the company to add 7D Surgical’s FLASH™ flagship navigation system founded upon its machine-vision, image-guided platform.

Enabling technology isn’t the only differentiator sought by spine players. NuVasive filled a portfolio gap with the purchase of Simplify Medical for its Simplify® Cervical Artificial Disc. Spectrum Spine acquired BIOBraille™, a proprietary surface technology for spinal trauma applications.

Outside of spine, Paragon 28 added surgical navigation software through its purchase of Additive Orthopaedics, while Stryker boosted the capabilities of its Mako robot through the acquisition of OrthoSensor.

In all, we expect another 20 to 30 transactions in the second half of 2021. Spine is likely to remain an attractive market for M&A activity as companies seek new growth opportunities in that very mature and steady market. The ratio of joint replacement and digital transactions are likely to increase, with most deals being smaller tuck-in acquisitions.

Mike Evers is ORTHOWORLD’s Digital Content Strategist. He can be reached at [email protected].

The COVID-19 pandemic did little to slow the orthopedic market’s consolidation. We surveyed the orthopedic merger and acquisition market over the last six years to show why 2020 was a busy year and 2021 may be busier; why spine continues to dominate M&A transactions; and what has driven transactions so far in 2021.

These charts, and the data...

The COVID-19 pandemic did little to slow the orthopedic market’s consolidation. We surveyed the orthopedic merger and acquisition market over the last six years to show why 2020 was a busy year and 2021 may be busier; why spine continues to dominate M&A transactions; and what has driven transactions so far in 2021.

These charts, and the data that generated them, are taken from our new M&A Tracker 1993-2021 that’s available for purchase in our store.

OVERALL TRENDS FOR 2016 TO 2021

Despite the impact of pandemic-related financial and business constraints, 2020 brought a brisk pace of mergers and acquisitions. We tracked 42 transactions for orthopedic device companies last year, as shown in Exhibit 1. Through the first half, 2021 is off to a slower start with 16 closed transactions compared to 19 at the same point the previous year. An unusually large number of deals (16) closed in the fourth quarter last year, nearly 40% of all 2020 transactions. The fourth quarter averaged closer to 10 deals in recent years, but we think the flurry of smaller acquisitions could elevate the totals again for 2021.

Exhibit 1: M&A Transactions by Year 2016 to YTD 2021

Companies in the $1 billion revenue tier dominate the M&A activity as they seek out new technologies and markets. Exhibit 2 shows that Stryker, Smith+Nephew and Zimmer Biomet have all completed at least 10 transactions since 2016.

Exhibit 2: Most Active Buyers 2016 to YTD 2021

DJO, powered by its parent company Colfax, burst into the ranking this year. The company already closed deals with Trilliant Surgical, MedShape and Mathys in 2021. Before the Mathys purchase, Colfax CEO Matthew Trerotola said, “There are bolt-ons and tuck-ins within that space that we can look at. We certainly have more flexibility now. Most of the things that we’re thinking about are in the small- to medium-size range in the short- to medium-term.”

Speaking of large-cap medtech in general, Canaccord Genuity analyst Kyle Rose said there is a “paucity of true organic growth.” Therefore, M&A is a critical strategy to generate revenue. We believe that is particularly true in the spine segment. Hundreds of small companies play in the spine space, making it ripe for acquisitions. So much so, that spine accounted for 60+ or 30% of all transactions we’ve tracked since 2016 as shown in Exhibit 3.

Further activity in the spine market could be spurred as mid-tier players like Globus Medical, ATEC and Surgalign continue to take significant share and Zimmer Biomet divests it spine business.

Exhibit 3: Most Active Product Segments 2016 to YTD 2021

* Private equity firms, contract manufacturing, distributors, instruments, sterilization and O.R. products

While the spine market remains the most active segment in 2021, as shown in Exhibit 4, there is fluidity in the other segments. Joint replacement has accelerated to 21% of all transactions compared to 14% for all of 2020. Trauma has fallen back to 12% from 25% last year. Transactions involving digital technology increased to 17% from just below 10% the prior year.

Exhibit 4: M&A Transactions by Segment YTD 2021

2021 TRANSACTIONS

Given the recovering market and commentary from executives, it seems reasonable to expect 2021 to finish with about 40 M&A transactions. While we don’t anticipate a deal the size of Stryker and Wright Medical for some time, we expect companies to remain aggressive in their acquisition search.

Doug Rice, CFO of Orthofix, said that the company was screening “more deals than ever” at the end of 2020.

Globus Medical has been quiet and certainly could make a splash. Globus Medical CEO Dave Demski said, “Yes, we are looking to be more aggressive there in terms of the amount we’re going to invest. We’re looking a little bit bigger. The emphasis is on expanding the differentiation within our portfolio. We’re looking for technology, not necessarily scale.”

Demski’s point about technology vs. scale is an interesting one. Viewed through that lens, the 16 transactions thus far in 2021 are roughly split down the middle.

Companies of all sizes are looking for complementary portfolio pieces and new markets. It is difficult to find a better recent example of a company deftly entering a new market than DJO. Since 2020, the company has rapidly stood up a dedicated foot-and-ankle business by investing $225 million. The addition of Mathys essentially doubles DJO’s international revenue.

Smaller players also seek similar opportunities through M&A. Through its merger with Kinos Medical, restor3d hopes to accelerate its entry into the U.S. foot and ankle market. Neo Medical acquired TriOs Medical to expand its footprint in the German and greater European markets. Implanet’s purchase of a majority stake in Orthopaedic & Spine Development will help the company achieve revenue critical mass to meet its “regulatory, clinical and economic demands.”

Like those seeking scale, companies along the revenue spectrum are finding ways to differentiate their offerings through acquisition. Enabling technology figures heavily in this category, most notably with mid-sized spine players as that segment rapidly shifts toward digital services. While COVID disrupted the timing of ATEC’s purchase of EOS imaging, the company now has a unique imaging tool to add to its AlphaInformatiX platform. SeaSpine initially partnered with 7D Surgical in 2020, but ultimately decided to purchase the company to add 7D Surgical’s FLASH™ flagship navigation system founded upon its machine-vision, image-guided platform.

Enabling technology isn’t the only differentiator sought by spine players. NuVasive filled a portfolio gap with the purchase of Simplify Medical for its Simplify® Cervical Artificial Disc. Spectrum Spine acquired BIOBraille™, a proprietary surface technology for spinal trauma applications.

Outside of spine, Paragon 28 added surgical navigation software through its purchase of Additive Orthopaedics, while Stryker boosted the capabilities of its Mako robot through the acquisition of OrthoSensor.

In all, we expect another 20 to 30 transactions in the second half of 2021. Spine is likely to remain an attractive market for M&A activity as companies seek new growth opportunities in that very mature and steady market. The ratio of joint replacement and digital transactions are likely to increase, with most deals being smaller tuck-in acquisitions.

Mike Evers is ORTHOWORLD’s Digital Content Strategist. He can be reached at [email protected].

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.