Copy to clipboard

Copy to clipboard

COVID-19’s effect on the orthopedic industry became clearer as the public device companies reported their first-quarter earnings. Below we’ll examine how the companies performed and the actions they took to mitigate the pandemic’s impact. We’ll also review the consensus for recovery scenarios and look at ways that COVID may leave a lasting mark on orthopedics once sales volumes normalize.

Late March Slowdowns Lead to Bleak Second Quarter

The orthopedic market started 2020 with significant momentum, according to the companies we covered. Nearly every company said that January and February trended above expectations. Globus Medical, DJO and SeaSpine all tracked toward double-digit growth in the quarter. As the pandemic deepened in March, however, orthopedic players saw an abrupt decline in sales volume. Procedure declines hit particularly hard in the last two weeks of March as, for example, Stryker’s sales declined -30% while Zimmer Biomet’s sales fell -60% for that period.

Capital sales like robotic systems are generally weighted toward quarter-end and suffered significantly due to the timing of the downturn. While Globus Medical’s ExcelsiusGPS grew +11.8%, it did so against one of the weakest comparisons in the product’s history. Zimmer Biomet’s ROSA Knee contributed little to first quarter sales after a strong start in late 2019. Company CEO Bryan Hanson said, “[ROSA] had very little impact for us in Q1. That’s not surprising; it’s not even concerning. Most of the sales of a robotics program, or capital equipment in general, comes toward the end of the quarter. It’s not surprising that many of those opportunities got deferred.”

We suspect that the orthopedic market declined in the high single digits for the first quarter of 2020. Exhibit 1 shows 1Q20 orthopedic sales results for select public companies. We estimate that these companies represent roughly 60% of the market.

Exhibit 1: Orthopedic Sales by Company for 1Q20 ($ Millions)

| Company | 1Q20 | 1Q19 | $ Chg | % Chg |

|---|---|---|---|---|

| DePuy Synthes | $2,038.0 | $2,203.0 | ($165.0) | (7.5%) |

| Stryker | $1,793.7 | $1,846.6 | ($52.9) | (2.9%) |

| Zimmer Biomet | $1,602.4 | $1,764.1 | ($161.7) | (9.2%) |

| Smith+Nephew | $800.9 | $885.2 | ($84.3) | (9.5%) |

| NuVasive | $259.9 | $274.8 | ($14.9) | (5.4%) |

| Wright Medical | $218.5 | $230.1 | ($11.6) | (5%) |

| Globus Medical | $190.6 | $182.9 | $7.6 | 4.2% |

| Orthofix | $104.8 | $109.1 | ($4.3) | (3.9%) |

| ConMed | $99.3 | $113.4 | ($14.2) | (12.5%) |

| DJO | $89.3 | $89.9 | ($0.5) | (0.6%) |

| Sanofi | $62.7 | $73.5 | ($10.8) | (14.7%) |

| SeaSpine | $36.1 | $36.2 | ($0.0) | (0.1%) |

| Anika | $33.4 | $23.0 | $10.4 | 45% |

| ATEC Spine | $30.1 | $24.6 | $5.6 | 22.6% |

| Amplitude Surgical | $28.8 | $31.9 | ($3.1) | (9.8%) |

| Integra LifeSciences | $21.5 | $22.7 | ($1.2) | (5.3%) |

| Vericel | $20.3 | $16.6 | $3.7 | 22.4% |

| SI-BONE | $16.8 | $15.0 | $1.8 | 12.2% |

| Conformis | $16.5 | $20.6 | ($4.2) | (20.2%) |

| OrthoPediatrics | $16.4 | $14.7 | $1.7 | 11.6% |

| Total | $7,479.9 | $7,977.9 | ($498.0) | (6.2%) |

While there is some debate where specific orthopedic procedures fall on the spectrum of “electiveness,” no segment was genuinely insulated from COVID procedure deferrals. Trauma, the most emergent of the segments, suffered like the rest as stay-at-home orders reduced auto- and work-related accidents. Trauma players like Orthofix that rely on deformity correction portfolios saw even sharper declines. DePuy Synthes noted that 20% of its trauma procedures were deferrable.

Virtually all companies agree that the orthopedic market will bottom out in the second quarter. Thankfully, it seems that the market has endured through the worst period with April most likely representing the trough. We expect second quarter sales to decline between -60% and -70% based on April trends. Companies with well-diversified medtech portfolios mitigated some negative impacts in April, but orthopedic business lines struggled consistently. Stryker, for instance, declined by about -35% overall in April while its orthopedic and spine business declined -65%. Players like NuVasive and Globus fell around -70% for April, while severely exposed companies like Conformis declined -95% for the month.

With revenue plummeting, companies initiated aggressive cost-containment measures and sought to bolster liquidity via credit facilities. Standard measures included low hanging fruit like reducing discretionary spending, eliminating travel and entertainment and terminating consulting fees.

Players sought to find a balance, however, between lowering costs and maintaining business continuity. To create room for these initiatives, many companies have instituted pay reductions for board members and executive teams. Some have also temporarily suspended employee benefits.

Companies refrained from reducing salesforce headcount in anticipation of a market rebound later in the year. Companies like Smith+Nephew have instituted programs to lessen the financial blow to commission-based reps. Likewise, modulating inventory levels is a critical task to ensure adequate inventory levels for the anticipated backlog of patients.

Well capitalized companies vowed to push forward with R&D and innovation initiatives in an attempt to widen or create a competitive advantage during the downtime. Zimmer Biomet said that they plan to “double down” on critical efforts like robotics while NuVasive CFO Matt Harbaugh said, “You’ll notice that we continue to spend at a healthy clip in R&D, a bit higher than where we were this time last year. We have the capital to invest there. If others are slowing while we’re keeping our foot on the gas pedal, that should play into our strategy.”

We Expect a Slow but Steady Recovery

Orthopedic companies are confident that patients with deferred procedures will return to the sales pipeline when restrictions lift. While orthopedic surgery is elective, it generally treats degenerative conditions that cause significant pain and do not improve with time. Spine-focused players are particularly confident that their procedures will be among the first to enter the funnel.

Surgeons and hospital administrators are highly driven to work through patient backlogs to recoup lost revenue. Stryker Chairman and CEO Kevin Lobo said, “Hospitals are very motivated to do our procedures. Orthopedics and spine procedures are moneymakers for hospitals. Hospitals treating coronavirus patients now are bleeding in their P&Ls. There’s financial motivation. Hospital CEOs and surgeons that I’ve spoken to are all absolutely gearing up to start bringing back patients.”

The reinstatement of elective procedures will vary significantly by both geography and health system, thus slowing the recovery curve. Our conversations with surgeons and hospital and ASC administrators indicate that procedure ramp-up could be complicated by numerous factors, including patient scheduling, O.R. availability as other specialties vie for time, surgical staff shortages that could come via contraction of the virus or burnout from the sheer volume of catching up, and fewer people with insurance. Additionally, new risk mitigation processes will decrease efficiency in the operating room. The availability of personal protective equipment and coronavirus testing will also modulate the number of surgical procedures.

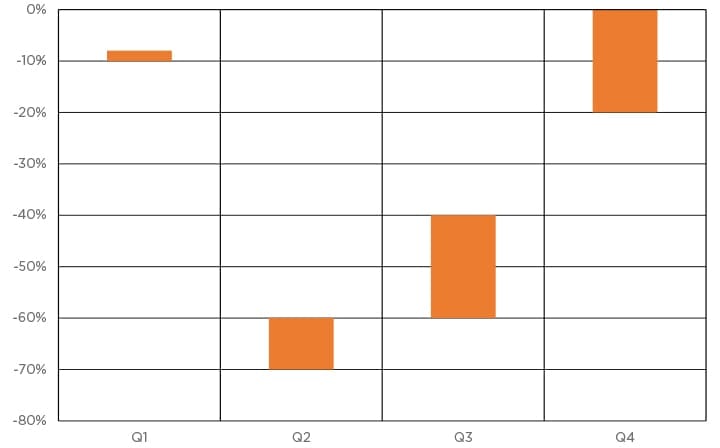

We expect recovery efforts to begin early in the third quarter with procedural volumes down -40% to -60% vs. the prior year. The fourth quarter could be the first time that the market reaches a semblance of “normal” when procedures approach pre-COVID levels. For example, modeling from Integra LifeSciences shows 4Q20 revenues in line with 4Q19 and, in some favorable scenarios, bringing opportunities for growth. Exhibit 2 depicts all orthopedic procedure declines by quarter in 2020.

Exhibit 2: Estimated Ranges of Orthopedic Procedure Declines by Quarter in 2020

We have little confidence in a “V”-shaped recovery curve. Virtually all public company modeling assumes no significant resurgence of infection rates in the fall. Given the course of the pandemic to this point, it seems likely that infection rates will surge again at some point as countries begin to reopen.

NuVasive President Matt Link said, “Even under the best-case circumstances, we’re not returning to an environment that’s COVID-free. When you start to think about protocols across the service line, how are they going to protect healthcare providers? How are they going to protect patients? How they’re going to limit the potential impact of a subsequent rebound is critically important. That’s going to impact volumes and throughputs. They’ll be inherently less efficient.”

The New Normal: Potential Long-Term Impacts from COVID

Many companies found ways to continue to connect with employees and educate customers during surgical shutdowns. Senior leaders at OrthoPediatrics make weekly calls to sales consultants to maintain team cohesion. Company CEO Mark Throdahl described the calls, saying, “Our HR VP puts out a telephone chain to the entire senior management team so that one of us touches base with one of our associates every week. These are non-business calls; it’s just to call and ask about the weather in Des Moines. How is your family keeping? As you can imagine, that has a very powerful impact on people who are working remotely.”

Zimmer Biomet created a virtual reality “booth” where their healthcare partners can tour and learn about the products that they would have seen at AAOS. They can talk directly to commercial teams via the virtual experience and sign up for training that would have been available at the conference. We expect companies across the industry to embrace remote work further and find new ways to leverage technology in their customer relationships. Travel reduction is a likely outcome of this pivot and could potentially have follow-on implications for industry conferences.

We do not expect the shift of procedures to ASCs to accelerate rapidly in the wake of COVID-19. While the existing trend toward ASCs will continue, those settings do not appear to have adequate capacity to handle a massive influx of new procedures. Per Stryker, there are about 300 ASCs in the U.S. that perform knee and hip procedures. They were all running at or near full capacity before the pandemic. Even with staff working longer hours, additional procedures are limited.

NuVasive’s Matt Link echoed those sentiments for the spine market, “It’s not as if there’s necessarily a huge capacity for new procedures to shift to that setting. I do think that the surgeries that are routinely done in that setting will see some uptake.” Spine surgeries suited to ASCs tend to be lower in complexity and revenue.

We also predict that there will be some consolidation in the market. Some companies will simply run out of financial runway. Conformis, for example, can remain liquid for about another year. Steep sales declines in 2019 due to Aetna coverage issues and devastating impacts from COVID could cause Conformis to sink below the horizon or become an acquisition target. While we expect that most companies will be preoccupied by COVID-19 recoveries in 2020 and into 2021, cash-rich companies could make tuck-in acquisitions to gain access to immediate revenue streams or seek deals for novel technology.

Even smaller companies with adequate capital could find themselves on the outside of accounts. We expect many health systems will seek ways to reduce foot traffic in and around the operating room. Paring down vendor lists, even to a sole or dual source, is a likely scenario. Companies with robust portfolios and enabling technologies will have a profound advantage over smaller players.

While early-May trends showed hopeful signs of improvement over April, we anticipate that procedure recovery will improve only incrementally in 3Q before the market returns to something approximating baseline in 4Q. While hospitals and surgeons are highly motivated to work through patient backlogs, facility capacity limitations and newly-implemented protocols will offset some of that higher volume. Again, we expect the recovery to extend into 2021.

Patients awaiting orthopedic surgeries are usually in significant pain and experiencing a reduced quality of life. We expect the vast majority of them to return and have their procedures eventually done. The underlying fundamentals of the orthopedic industry remain unchanged due to COVID-19. However, we should prepare for significant alterations in the market landscape as well as the ways that we interact with colleagues and customers.

Mike Evers is ORTHOWORLD’s Digital Content Strategist.

COVID-19’s effect on the orthopedic industry became clearer as the public device companies reported their first-quarter earnings. Below we’ll examine how the companies performed and the actions they took to mitigate the pandemic’s impact. We’ll also review the consensus for recovery scenarios and look at ways that COVID may leave a lasting mark...

COVID-19’s effect on the orthopedic industry became clearer as the public device companies reported their first-quarter earnings. Below we’ll examine how the companies performed and the actions they took to mitigate the pandemic’s impact. We’ll also review the consensus for recovery scenarios and look at ways that COVID may leave a lasting mark on orthopedics once sales volumes normalize.

Late March Slowdowns Lead to Bleak Second Quarter

The orthopedic market started 2020 with significant momentum, according to the companies we covered. Nearly every company said that January and February trended above expectations. Globus Medical, DJO and SeaSpine all tracked toward double-digit growth in the quarter. As the pandemic deepened in March, however, orthopedic players saw an abrupt decline in sales volume. Procedure declines hit particularly hard in the last two weeks of March as, for example, Stryker’s sales declined -30% while Zimmer Biomet’s sales fell -60% for that period.

Capital sales like robotic systems are generally weighted toward quarter-end and suffered significantly due to the timing of the downturn. While Globus Medical’s ExcelsiusGPS grew +11.8%, it did so against one of the weakest comparisons in the product’s history. Zimmer Biomet’s ROSA Knee contributed little to first quarter sales after a strong start in late 2019. Company CEO Bryan Hanson said, “[ROSA] had very little impact for us in Q1. That’s not surprising; it’s not even concerning. Most of the sales of a robotics program, or capital equipment in general, comes toward the end of the quarter. It’s not surprising that many of those opportunities got deferred.”

We suspect that the orthopedic market declined in the high single digits for the first quarter of 2020. Exhibit 1 shows 1Q20 orthopedic sales results for select public companies. We estimate that these companies represent roughly 60% of the market.

Exhibit 1: Orthopedic Sales by Company for 1Q20 ($ Millions)

| Company | 1Q20 | 1Q19 | $ Chg | % Chg |

|---|---|---|---|---|

| DePuy Synthes | $2,038.0 | $2,203.0 | ($165.0) | (7.5%) |

| Stryker | $1,793.7 | $1,846.6 | ($52.9) | (2.9%) |

| Zimmer Biomet | $1,602.4 | $1,764.1 | ($161.7) | (9.2%) |

| Smith+Nephew | $800.9 | $885.2 | ($84.3) | (9.5%) |

| NuVasive | $259.9 | $274.8 | ($14.9) | (5.4%) |

| Wright Medical | $218.5 | $230.1 | ($11.6) | (5%) |

| Globus Medical | $190.6 | $182.9 | $7.6 | 4.2% |

| Orthofix | $104.8 | $109.1 | ($4.3) | (3.9%) |

| ConMed | $99.3 | $113.4 | ($14.2) | (12.5%) |

| DJO | $89.3 | $89.9 | ($0.5) | (0.6%) |

| Sanofi | $62.7 | $73.5 | ($10.8) | (14.7%) |

| SeaSpine | $36.1 | $36.2 | ($0.0) | (0.1%) |

| Anika | $33.4 | $23.0 | $10.4 | 45% |

| ATEC Spine | $30.1 | $24.6 | $5.6 | 22.6% |

| Amplitude Surgical | $28.8 | $31.9 | ($3.1) | (9.8%) |

| Integra LifeSciences | $21.5 | $22.7 | ($1.2) | (5.3%) |

| Vericel | $20.3 | $16.6 | $3.7 | 22.4% |

| SI-BONE | $16.8 | $15.0 | $1.8 | 12.2% |

| Conformis | $16.5 | $20.6 | ($4.2) | (20.2%) |

| OrthoPediatrics | $16.4 | $14.7 | $1.7 | 11.6% |

| Total | $7,479.9 | $7,977.9 | ($498.0) | (6.2%) |

While there is some debate where specific orthopedic procedures fall on the spectrum of “electiveness,” no segment was genuinely insulated from COVID procedure deferrals. Trauma, the most emergent of the segments, suffered like the rest as stay-at-home orders reduced auto- and work-related accidents. Trauma players like Orthofix that rely on deformity correction portfolios saw even sharper declines. DePuy Synthes noted that 20% of its trauma procedures were deferrable.

Virtually all companies agree that the orthopedic market will bottom out in the second quarter. Thankfully, it seems that the market has endured through the worst period with April most likely representing the trough. We expect second quarter sales to decline between -60% and -70% based on April trends. Companies with well-diversified medtech portfolios mitigated some negative impacts in April, but orthopedic business lines struggled consistently. Stryker, for instance, declined by about -35% overall in April while its orthopedic and spine business declined -65%. Players like NuVasive and Globus fell around -70% for April, while severely exposed companies like Conformis declined -95% for the month.

With revenue plummeting, companies initiated aggressive cost-containment measures and sought to bolster liquidity via credit facilities. Standard measures included low hanging fruit like reducing discretionary spending, eliminating travel and entertainment and terminating consulting fees.

Players sought to find a balance, however, between lowering costs and maintaining business continuity. To create room for these initiatives, many companies have instituted pay reductions for board members and executive teams. Some have also temporarily suspended employee benefits.

Companies refrained from reducing salesforce headcount in anticipation of a market rebound later in the year. Companies like Smith+Nephew have instituted programs to lessen the financial blow to commission-based reps. Likewise, modulating inventory levels is a critical task to ensure adequate inventory levels for the anticipated backlog of patients.

Well capitalized companies vowed to push forward with R&D and innovation initiatives in an attempt to widen or create a competitive advantage during the downtime. Zimmer Biomet said that they plan to “double down” on critical efforts like robotics while NuVasive CFO Matt Harbaugh said, “You’ll notice that we continue to spend at a healthy clip in R&D, a bit higher than where we were this time last year. We have the capital to invest there. If others are slowing while we’re keeping our foot on the gas pedal, that should play into our strategy.”

We Expect a Slow but Steady Recovery

Orthopedic companies are confident that patients with deferred procedures will return to the sales pipeline when restrictions lift. While orthopedic surgery is elective, it generally treats degenerative conditions that cause significant pain and do not improve with time. Spine-focused players are particularly confident that their procedures will be among the first to enter the funnel.

Surgeons and hospital administrators are highly driven to work through patient backlogs to recoup lost revenue. Stryker Chairman and CEO Kevin Lobo said, “Hospitals are very motivated to do our procedures. Orthopedics and spine procedures are moneymakers for hospitals. Hospitals treating coronavirus patients now are bleeding in their P&Ls. There’s financial motivation. Hospital CEOs and surgeons that I’ve spoken to are all absolutely gearing up to start bringing back patients.”

The reinstatement of elective procedures will vary significantly by both geography and health system, thus slowing the recovery curve. Our conversations with surgeons and hospital and ASC administrators indicate that procedure ramp-up could be complicated by numerous factors, including patient scheduling, O.R. availability as other specialties vie for time, surgical staff shortages that could come via contraction of the virus or burnout from the sheer volume of catching up, and fewer people with insurance. Additionally, new risk mitigation processes will decrease efficiency in the operating room. The availability of personal protective equipment and coronavirus testing will also modulate the number of surgical procedures.

We expect recovery efforts to begin early in the third quarter with procedural volumes down -40% to -60% vs. the prior year. The fourth quarter could be the first time that the market reaches a semblance of “normal” when procedures approach pre-COVID levels. For example, modeling from Integra LifeSciences shows 4Q20 revenues in line with 4Q19 and, in some favorable scenarios, bringing opportunities for growth. Exhibit 2 depicts all orthopedic procedure declines by quarter in 2020.

Exhibit 2: Estimated Ranges of Orthopedic Procedure Declines by Quarter in 2020

We have little confidence in a “V”-shaped recovery curve. Virtually all public company modeling assumes no significant resurgence of infection rates in the fall. Given the course of the pandemic to this point, it seems likely that infection rates will surge again at some point as countries begin to reopen.

NuVasive President Matt Link said, “Even under the best-case circumstances, we’re not returning to an environment that’s COVID-free. When you start to think about protocols across the service line, how are they going to protect healthcare providers? How are they going to protect patients? How they’re going to limit the potential impact of a subsequent rebound is critically important. That’s going to impact volumes and throughputs. They’ll be inherently less efficient.”

The New Normal: Potential Long-Term Impacts from COVID

Many companies found ways to continue to connect with employees and educate customers during surgical shutdowns. Senior leaders at OrthoPediatrics make weekly calls to sales consultants to maintain team cohesion. Company CEO Mark Throdahl described the calls, saying, “Our HR VP puts out a telephone chain to the entire senior management team so that one of us touches base with one of our associates every week. These are non-business calls; it’s just to call and ask about the weather in Des Moines. How is your family keeping? As you can imagine, that has a very powerful impact on people who are working remotely.”

Zimmer Biomet created a virtual reality “booth” where their healthcare partners can tour and learn about the products that they would have seen at AAOS. They can talk directly to commercial teams via the virtual experience and sign up for training that would have been available at the conference. We expect companies across the industry to embrace remote work further and find new ways to leverage technology in their customer relationships. Travel reduction is a likely outcome of this pivot and could potentially have follow-on implications for industry conferences.

We do not expect the shift of procedures to ASCs to accelerate rapidly in the wake of COVID-19. While the existing trend toward ASCs will continue, those settings do not appear to have adequate capacity to handle a massive influx of new procedures. Per Stryker, there are about 300 ASCs in the U.S. that perform knee and hip procedures. They were all running at or near full capacity before the pandemic. Even with staff working longer hours, additional procedures are limited.

NuVasive’s Matt Link echoed those sentiments for the spine market, “It’s not as if there’s necessarily a huge capacity for new procedures to shift to that setting. I do think that the surgeries that are routinely done in that setting will see some uptake.” Spine surgeries suited to ASCs tend to be lower in complexity and revenue.

We also predict that there will be some consolidation in the market. Some companies will simply run out of financial runway. Conformis, for example, can remain liquid for about another year. Steep sales declines in 2019 due to Aetna coverage issues and devastating impacts from COVID could cause Conformis to sink below the horizon or become an acquisition target. While we expect that most companies will be preoccupied by COVID-19 recoveries in 2020 and into 2021, cash-rich companies could make tuck-in acquisitions to gain access to immediate revenue streams or seek deals for novel technology.

Even smaller companies with adequate capital could find themselves on the outside of accounts. We expect many health systems will seek ways to reduce foot traffic in and around the operating room. Paring down vendor lists, even to a sole or dual source, is a likely scenario. Companies with robust portfolios and enabling technologies will have a profound advantage over smaller players.

While early-May trends showed hopeful signs of improvement over April, we anticipate that procedure recovery will improve only incrementally in 3Q before the market returns to something approximating baseline in 4Q. While hospitals and surgeons are highly motivated to work through patient backlogs, facility capacity limitations and newly-implemented protocols will offset some of that higher volume. Again, we expect the recovery to extend into 2021.

Patients awaiting orthopedic surgeries are usually in significant pain and experiencing a reduced quality of life. We expect the vast majority of them to return and have their procedures eventually done. The underlying fundamentals of the orthopedic industry remain unchanged due to COVID-19. However, we should prepare for significant alterations in the market landscape as well as the ways that we interact with colleagues and customers.

Mike Evers is ORTHOWORLD’s Digital Content Strategist.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.