Copy to clipboard

Copy to clipboard

Despite the uncertainty brought on by COVID-19, we’ve looked ahead and developed our orthopedic market forecasts through 2022. This data and a full look at the orthopedic market’s 2019 performance is available for download now in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The last decade brought significant change in orthopedics to areas such as:

- new materials

- company and hospital consolidation

- the shift of procedures to outpatient centers

- the proliferation of additive manufacturing

- the advancement of enabling technologies

- stringent regulations worldwide with UDI and the E.U.’s Medical Device Regulation

However, COVID-19 presents unprecedented changes and challenges to the orthopedic market due to its unpredictability. The pandemic’s spread around the globe continues to take a great human and economic toll and stunt orthopedics through the postponement of elective procedures.

The deferral of orthopedic procedures has led to monumental revenue loss for hospitals, surgeons, OEMs and contract manufacturers, all of whom face significant business disruption and uncertainty. While some of the largest device companies have balance sheets strong enough to weather extended downturns, smaller players will soon struggle with cash flow. The disjointed nature of orthopedic procedure restarts, and uncertainty about the recovery curve, will make inventory and manufacturing forecasts difficult. Several device companies have already delayed new product launches. Healthcare delivery and manufacturing chains will need to become leaner.

Our orthopedic market forecast models ripple effects through 2022 and beyond. That said, we remain confident in orthopedics’ return to growth due to demographics and the economic need of all nations to keep their people productive.

Factors Impacting Orthopedic Market Forecast and Trends

As with all challenges, opportunities will emerge. Executives, administrators and surgeons are working to reorient themselves to a new normal. We expect the following trends to develop and endure:

- Embracing Virtual Communication

- Stronger Supply and Care Delivery Chains

- Continued Adoption of Enabling Technology

- The Proliferation of Additive Manufacturing

- Company Consolidation

- The Continued Rise of Outpatient Centers

Embracing Virtual Communication

Social distancing has forced nearly everyone to adopt some form of virtual communication for connecting with colleagues, vendors, customers, doctors and patients. Telemedicine, webinars, online conferences and virtual reality training for procedures are just a few examples of the industry’s rapid pivot to remote work. All of this technology brings the likelihood of lasting economic benefits, which means that they will be a part of your new day-to-day.

Stronger Supply and Care Delivery Chains

As providers work through the backlog of surgeries, they’ll require a higher level of transparency and efficiency in logistics, product sterilization and the O.R. This shift could bear out in greater automation of the supply chain and surgical process and an uptick in single-use sterilized products. It will also result in even more orthopedic procedures moving to ambulatory surgery centers (ASCs) and to hospitals partnering with ASCs to streamline the flow of otherwise healthy patients to these cost-reducing, efficient sites of care. Also, traditional sales rep roles that involve bringing products and serving as an advisor in the O.R. will be under intense scrutiny.

Continued Adoption of Enabling Technology

Orthopedics’ largest players shifted R&D investment and strategies to enabling technologies in 2019. A period of financial recovery for hospitals responding to COVID-19 is likely to stunt the growth of capital equipment sales into 2021. Robots currently in use are likely to be deployed in surgeries. We expect device companies to continue to invest in robotics, imaging and planning. These technologies will continue their trend toward lower cost and increased versatility as competition increases while hospital budgets become tighter.

The Proliferation of Additive Manufacturing

The adoption of 3D printing will continue to grow in orthopedics due to companies of all sizes being able to leverage the technology. Numerous small companies, primarily in spine, are building portfolios focused on 3D printing. These companies may be at a disadvantage for growth due to their limited portfolio offering. Additionally, we expect orthopedic companies and contract manufacturers will tighten their purchase of equipment and pause investments in new machines.

Company Consolidation

Stryker’s pending acquisition of Wright Medical may be the largest transaction we see for some time. Cash-rich companies could make tuck-in acquisitions to gain access to immediate revenue streams or seek deals in niche markets. Still, we expect most orthopedic companies will be too preoccupied with their COVID-19 response to think about complicated acquisition integrations in 2020 and early 2021. We maintain that small companies remain the innovation engine in orthopedics. Therefore, large and medium-sized companies will seek to acquire novel implants and software companies to expand their portfolios quickly so small acquisitions will continue.

The Continued Rise of Outpatient Centers

As elective surgeries resume, ASCs will recover more quickly than hospitals due to their efficiency as well as their orthopedic focus. ASCs have momentum with payors, hospitals, surgeons and device companies behind the push to this outpatient setting. Specifically, we expect hospitals to create relationships with physician-owned ASCs and build specialty centers with outpatient services to move orthopedic patients to these settings. Additionally, during the COVID-19 recovery period, patients will seek limited exposure to other patients and choose this setting over a hospital. ASCs have a more limited capacity than hospitals; however, companies with dedicated outpatient strategies will benefit from this focus in the short term.

Our Orthopedic Market Forecast Through 2022

We’ve based the general foundation for our orthopedic market forecast on the following: COVID-19’s disruption to orthopedic procedure volumes and day-to-day business to last through 2020 and into 2021, orthopedic procedure volume will stabilize near historical baselines by mid-2021, and device company revenues will stabilize by 2022.

The trajectory of any procedure recovery curve will be impacted by:

- High unemployment rates and economic upheaval. Would-be patients without insurance will delay and cancel treatments, and those with jobs will reconsider taking time away for fear of losing them. The U.S. Bureau of Labor Statistics reported a May 2020 adjusted unemployment rate of 16.3%.

- Apprehensive patients. The fear of contracting COVID-19 will linger and will be a significant factor in the rate of procedure recovery.

- Operating room and surgery center competition. Non-orthopedic specialties are vying for scheduling time, too.

- COVID-19 pandemic. The novel coronavirus will dictate changes to care delivery for the next 12 to 18 months at best, with an overarching expectation of the likelihood of a future epidemic or pandemic.

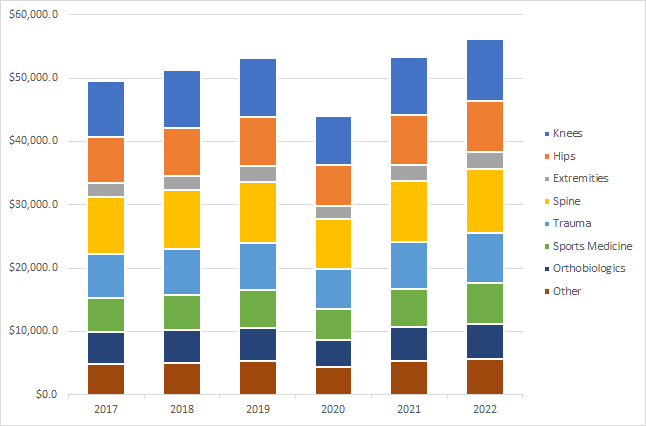

Our forecast calls for a stark -17% decline in 2020 revenue and modest +21% growth in 2021. As a result. we expect revenue growth rates to approach historical normalized levels in 2022., as shown in Exhibits 1 and 2.

Exhibit 1: Orthopedic Sales – 2017 to 2022 ($Millions)

| Product Segment | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|

| Joint Replacement | $18,242.7 | $18,919.7 | $19,549.5 | $16,146.7 | $19,584.5 | $20,525.7 |

| $ Chg | $677.0 | $629.8 | -$3,402.8 | $3,437.8 | $941.2 | |

| % Chg | 3.7% | 3.3% | -17.4% | 21.3% | 4.8% | |

| Knees | $8,783.3 | $9,058.2 | $9,324.2 | $7,673.8 | $9,300.7 | $9,709.9 |

| $ Chg | $274.9 | $266.0 | -$1,650.4 | $1,626.9 | $409.2 | |

| % Chg | 3.1% | 2.9% | -17.7% | 21.2% | 4.4% | |

| Hips | $7,349.4 | $7,582.3 | $7,788.8 | $6,472.5 | $7,799.3 | $8,142.5 |

| $ Chg | $232.9 | $206.5 | -$1,316.3 | $1,326.9 | $343.2 | |

| % Chg | 3.2% | 2.7% | -16.9% | 20.5% | 4.4% | |

| Extremities | $2,110.0 | $2,279.2 | $2,436.5 | $2,000.4 | $2,484.5 | $2,673.3 |

| $ Chg | $169.2 | $157.3 | -$436.1 | $484.1 | $188.8 | |

| % Chg | 8.0% | 6.9% | -17.9% | 24.2% | 7.6% | |

| Spine | $9,080.9 | $9,324.7 | $9,654.1 | $7,906.7 | $9,662.0 | $10,116.1 |

| $ Chg | $243.8 | $329.4 | -$1,747.4 | $1,755.3 | $454.1 | |

| % Chg | 2.7% | 3.5% | -18.1% | 22.2% | 4.7% | |

| Trauma | $6,920.0 | $7,205.9 | $7,449.3 | $6,302.1 | $7,486.9 | $7,853.8 |

| $ Chg | $285.9 | $243.4 | -$1,147.2 | $1,184.8 | $366.9 | |

| % Chg | 4.1% | 3.4% | -15.4% | 18.8% | 4.9% | |

| Sports Medicine | $5,318.5 | $5,614.4 | $5,920.7 | $4,896.4 | $6,022.6 | $6,378.0 |

| $ Chg | $295.9 | $306.3 | -$1,024.3 | $1,126.2 | $355.3 | |

| % Chg | 5.6% | 5.5% | -17.3% | 23.0% | 5.9% | |

| Orthobiologics | $5,097.1 | $5,088.0 | $5,291.1 | $4,338.7 | $5,293.2 | $5,589.6 |

| $ Chg | -$9.1 | $203.1 | -$952.4 | $954.5 | $296.4 | |

| % Chg | -0.2% | 4.0% | -18.0% | 22.0% | 5.6% | |

| Other | $4,833.3 | $5,075.0 | $5,288.2 | $4,336.3 | $5,338.0 | $5,652.9 |

| $ Chg | $241.7 | $213.2 | -$951.9 | $1,001.7 | $314.9 | |

| % Chg | 5.0% | 4.2% | -18.0% | 23.1% | 5.9% | |

| Total Market | $49,492.5 | $51,227.7 | $53,152.9 | $43,926.9 | $53,387.2 | $56,116.1 |

| $ Chg | $1,735.2 | $1,925.2 | -$9,226.0 | $9,460.3 | $2,728.9 | |

| % Chg | 3.5% | 3.8% | -17.4% | 21.5% | 5.1% |

Exhibit 2: Orthopedic Sales Trajectory – 2017 to 2022 ($Millions)

The New Normal for Orthopedics

We maintain that orthopedics will remain an attractive market due to demographics and the room for continuing innovation. However, orthopedics is entering a new normal. These extraordinary times will require everyone to diligently respond to market needs by relying on fundamental business principles. Success will come to those that:

- Over-communicate with customers. A tremendous number of variables complicate the orthopedic market forecast through 2021. Those that understand their customers’ challenges and their customers’ customers’ problems are best-positioned to help solve problems.

- Embrace change. COVID-19 upended decades-long business practices in a matter of weeks. Companies need to ask: How should we adapt to the new environment? The quickest to react to market needs are those who recognize the fast pace of change.

- Reimagine roles. Everyone in orthopedics will be impacted by the pandemic – from sales and marketing’s interaction with surgeons to R&D’s prioritization of new products, to supply chain’s collaboration with manufacturing partners. It’s an essential time to evaluate how the changing landscape affects individual roles. The better job we do, the more effective and valuable we are.

Despite the uncertainty brought on by COVID-19, we’ve looked ahead and developed our orthopedic market forecasts through 2022. This data and a full look at the orthopedic market’s 2019 performance is available for download now in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The last decade brought significant change in orthopedics to areas such...

Despite the uncertainty brought on by COVID-19, we’ve looked ahead and developed our orthopedic market forecasts through 2022. This data and a full look at the orthopedic market’s 2019 performance is available for download now in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®. The last decade brought significant change in orthopedics to areas such as:

- new materials

- company and hospital consolidation

- the shift of procedures to outpatient centers

- the proliferation of additive manufacturing

- the advancement of enabling technologies

- stringent regulations worldwide with UDI and the E.U.’s Medical Device Regulation

However, COVID-19 presents unprecedented changes and challenges to the orthopedic market due to its unpredictability. The pandemic’s spread around the globe continues to take a great human and economic toll and stunt orthopedics through the postponement of elective procedures.

The deferral of orthopedic procedures has led to monumental revenue loss for hospitals, surgeons, OEMs and contract manufacturers, all of whom face significant business disruption and uncertainty. While some of the largest device companies have balance sheets strong enough to weather extended downturns, smaller players will soon struggle with cash flow. The disjointed nature of orthopedic procedure restarts, and uncertainty about the recovery curve, will make inventory and manufacturing forecasts difficult. Several device companies have already delayed new product launches. Healthcare delivery and manufacturing chains will need to become leaner.

Our orthopedic market forecast models ripple effects through 2022 and beyond. That said, we remain confident in orthopedics’ return to growth due to demographics and the economic need of all nations to keep their people productive.

Factors Impacting Orthopedic Market Forecast and Trends

As with all challenges, opportunities will emerge. Executives, administrators and surgeons are working to reorient themselves to a new normal. We expect the following trends to develop and endure:

- Embracing Virtual Communication

- Stronger Supply and Care Delivery Chains

- Continued Adoption of Enabling Technology

- The Proliferation of Additive Manufacturing

- Company Consolidation

- The Continued Rise of Outpatient Centers

Embracing Virtual Communication

Social distancing has forced nearly everyone to adopt some form of virtual communication for connecting with colleagues, vendors, customers, doctors and patients. Telemedicine, webinars, online conferences and virtual reality training for procedures are just a few examples of the industry’s rapid pivot to remote work. All of this technology brings the likelihood of lasting economic benefits, which means that they will be a part of your new day-to-day.

Stronger Supply and Care Delivery Chains

As providers work through the backlog of surgeries, they’ll require a higher level of transparency and efficiency in logistics, product sterilization and the O.R. This shift could bear out in greater automation of the supply chain and surgical process and an uptick in single-use sterilized products. It will also result in even more orthopedic procedures moving to ambulatory surgery centers (ASCs) and to hospitals partnering with ASCs to streamline the flow of otherwise healthy patients to these cost-reducing, efficient sites of care. Also, traditional sales rep roles that involve bringing products and serving as an advisor in the O.R. will be under intense scrutiny.

Continued Adoption of Enabling Technology

Orthopedics’ largest players shifted R&D investment and strategies to enabling technologies in 2019. A period of financial recovery for hospitals responding to COVID-19 is likely to stunt the growth of capital equipment sales into 2021. Robots currently in use are likely to be deployed in surgeries. We expect device companies to continue to invest in robotics, imaging and planning. These technologies will continue their trend toward lower cost and increased versatility as competition increases while hospital budgets become tighter.

The Proliferation of Additive Manufacturing

The adoption of 3D printing will continue to grow in orthopedics due to companies of all sizes being able to leverage the technology. Numerous small companies, primarily in spine, are building portfolios focused on 3D printing. These companies may be at a disadvantage for growth due to their limited portfolio offering. Additionally, we expect orthopedic companies and contract manufacturers will tighten their purchase of equipment and pause investments in new machines.

Company Consolidation

Stryker’s pending acquisition of Wright Medical may be the largest transaction we see for some time. Cash-rich companies could make tuck-in acquisitions to gain access to immediate revenue streams or seek deals in niche markets. Still, we expect most orthopedic companies will be too preoccupied with their COVID-19 response to think about complicated acquisition integrations in 2020 and early 2021. We maintain that small companies remain the innovation engine in orthopedics. Therefore, large and medium-sized companies will seek to acquire novel implants and software companies to expand their portfolios quickly so small acquisitions will continue.

The Continued Rise of Outpatient Centers

As elective surgeries resume, ASCs will recover more quickly than hospitals due to their efficiency as well as their orthopedic focus. ASCs have momentum with payors, hospitals, surgeons and device companies behind the push to this outpatient setting. Specifically, we expect hospitals to create relationships with physician-owned ASCs and build specialty centers with outpatient services to move orthopedic patients to these settings. Additionally, during the COVID-19 recovery period, patients will seek limited exposure to other patients and choose this setting over a hospital. ASCs have a more limited capacity than hospitals; however, companies with dedicated outpatient strategies will benefit from this focus in the short term.

Our Orthopedic Market Forecast Through 2022

We’ve based the general foundation for our orthopedic market forecast on the following: COVID-19’s disruption to orthopedic procedure volumes and day-to-day business to last through 2020 and into 2021, orthopedic procedure volume will stabilize near historical baselines by mid-2021, and device company revenues will stabilize by 2022.

The trajectory of any procedure recovery curve will be impacted by:

- High unemployment rates and economic upheaval. Would-be patients without insurance will delay and cancel treatments, and those with jobs will reconsider taking time away for fear of losing them. The U.S. Bureau of Labor Statistics reported a May 2020 adjusted unemployment rate of 16.3%.

- Apprehensive patients. The fear of contracting COVID-19 will linger and will be a significant factor in the rate of procedure recovery.

- Operating room and surgery center competition. Non-orthopedic specialties are vying for scheduling time, too.

- COVID-19 pandemic. The novel coronavirus will dictate changes to care delivery for the next 12 to 18 months at best, with an overarching expectation of the likelihood of a future epidemic or pandemic.

Our forecast calls for a stark -17% decline in 2020 revenue and modest +21% growth in 2021. As a result. we expect revenue growth rates to approach historical normalized levels in 2022., as shown in Exhibits 1 and 2.

Exhibit 1: Orthopedic Sales – 2017 to 2022 ($Millions)

| Product Segment | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|

| Joint Replacement | $18,242.7 | $18,919.7 | $19,549.5 | $16,146.7 | $19,584.5 | $20,525.7 |

| $ Chg | $677.0 | $629.8 | -$3,402.8 | $3,437.8 | $941.2 | |

| % Chg | 3.7% | 3.3% | -17.4% | 21.3% | 4.8% | |

| Knees | $8,783.3 | $9,058.2 | $9,324.2 | $7,673.8 | $9,300.7 | $9,709.9 |

| $ Chg | $274.9 | $266.0 | -$1,650.4 | $1,626.9 | $409.2 | |

| % Chg | 3.1% | 2.9% | -17.7% | 21.2% | 4.4% | |

| Hips | $7,349.4 | $7,582.3 | $7,788.8 | $6,472.5 | $7,799.3 | $8,142.5 |

| $ Chg | $232.9 | $206.5 | -$1,316.3 | $1,326.9 | $343.2 | |

| % Chg | 3.2% | 2.7% | -16.9% | 20.5% | 4.4% | |

| Extremities | $2,110.0 | $2,279.2 | $2,436.5 | $2,000.4 | $2,484.5 | $2,673.3 |

| $ Chg | $169.2 | $157.3 | -$436.1 | $484.1 | $188.8 | |

| % Chg | 8.0% | 6.9% | -17.9% | 24.2% | 7.6% | |

| Spine | $9,080.9 | $9,324.7 | $9,654.1 | $7,906.7 | $9,662.0 | $10,116.1 |

| $ Chg | $243.8 | $329.4 | -$1,747.4 | $1,755.3 | $454.1 | |

| % Chg | 2.7% | 3.5% | -18.1% | 22.2% | 4.7% | |

| Trauma | $6,920.0 | $7,205.9 | $7,449.3 | $6,302.1 | $7,486.9 | $7,853.8 |

| $ Chg | $285.9 | $243.4 | -$1,147.2 | $1,184.8 | $366.9 | |

| % Chg | 4.1% | 3.4% | -15.4% | 18.8% | 4.9% | |

| Sports Medicine | $5,318.5 | $5,614.4 | $5,920.7 | $4,896.4 | $6,022.6 | $6,378.0 |

| $ Chg | $295.9 | $306.3 | -$1,024.3 | $1,126.2 | $355.3 | |

| % Chg | 5.6% | 5.5% | -17.3% | 23.0% | 5.9% | |

| Orthobiologics | $5,097.1 | $5,088.0 | $5,291.1 | $4,338.7 | $5,293.2 | $5,589.6 |

| $ Chg | -$9.1 | $203.1 | -$952.4 | $954.5 | $296.4 | |

| % Chg | -0.2% | 4.0% | -18.0% | 22.0% | 5.6% | |

| Other | $4,833.3 | $5,075.0 | $5,288.2 | $4,336.3 | $5,338.0 | $5,652.9 |

| $ Chg | $241.7 | $213.2 | -$951.9 | $1,001.7 | $314.9 | |

| % Chg | 5.0% | 4.2% | -18.0% | 23.1% | 5.9% | |

| Total Market | $49,492.5 | $51,227.7 | $53,152.9 | $43,926.9 | $53,387.2 | $56,116.1 |

| $ Chg | $1,735.2 | $1,925.2 | -$9,226.0 | $9,460.3 | $2,728.9 | |

| % Chg | 3.5% | 3.8% | -17.4% | 21.5% | 5.1% |

Exhibit 2: Orthopedic Sales Trajectory – 2017 to 2022 ($Millions)

The New Normal for Orthopedics

We maintain that orthopedics will remain an attractive market due to demographics and the room for continuing innovation. However, orthopedics is entering a new normal. These extraordinary times will require everyone to diligently respond to market needs by relying on fundamental business principles. Success will come to those that:

- Over-communicate with customers. A tremendous number of variables complicate the orthopedic market forecast through 2021. Those that understand their customers’ challenges and their customers’ customers’ problems are best-positioned to help solve problems.

- Embrace change. COVID-19 upended decades-long business practices in a matter of weeks. Companies need to ask: How should we adapt to the new environment? The quickest to react to market needs are those who recognize the fast pace of change.

- Reimagine roles. Everyone in orthopedics will be impacted by the pandemic – from sales and marketing’s interaction with surgeons to R&D’s prioritization of new products, to supply chain’s collaboration with manufacturing partners. It’s an essential time to evaluate how the changing landscape affects individual roles. The better job we do, the more effective and valuable we are.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.