Copy to clipboard

Copy to clipboard

The global hip joint replacement market grew 3.2% in 2018 vs. 2017, reaching revenue of USD $7.6 billion. We project that the market will reach $8.9 billion by 2023. In this article, we’ll dive deeper into company performance for 2018 and review results from the first quarter of 2019.

In Exhibits 1 and 2, we look at 2018 hip replacement sales for players with revenue over $50MM as well as market share for the top ten players.

Exhibit 1: 2018 Hip Replacement Sales Performance – Companies Over $50MM and All Others

| Companies | 2018 | 2017 | $ Chg | % Chg |

| Zimmer Biomet | $1,921.4 | $1,873.7 | $47.7 | 2.5% |

| Stryker | $1,571.0 | $1,520.2 | $50.8 | 3.3% |

| DePuy Synthes | $1,443.9 | $1,424.9 | $19.0 | 1.3% |

| Top-Tier Subtotal | $4,936.3 | $4,818.8 | $117.5 | 2.4% |

| Smith & Nephew | $613.0 | $599.0 | $14.0 | 2.3% |

| Aesculap | $232.0 | $218.7 | $13.3 | 6.1% |

| Medacta | $187.8 | $170.8 | $17.0 | 10.0% |

| KYOCERA | $130.5 | $127.1 | $3.4 | 2.7% |

| MicroPort Orthopedics | $125.2 | $122.4 | $2.8 | 2.3% |

| LimaCorporate | $98.4 | $94.5 | $3.9 | 4.1% |

| DJO | $68.3 | $61.6 | $6.7 | 10.9% |

| Waldemar Link | $64.9 | $63.1 | $1.8 | 2.9% |

| Mathys | $63.7 | $61.8 | $1.9 | 3.0% |

| Corin | $60.0 | $55.8 | $4.2 | 7.5% |

| Exactech | $53.9 | $51.0 | $2.9 | 5.7% |

| Next-Tier Subtotal | $1,697.8 | $1,625.8 | $72.0 | 4.4% |

| All Others | $948.2 | $904.8 | $43.4 | 4.8% |

| Total | $7,582.3 | $7,349.4 | $232.9 | 3.2% |

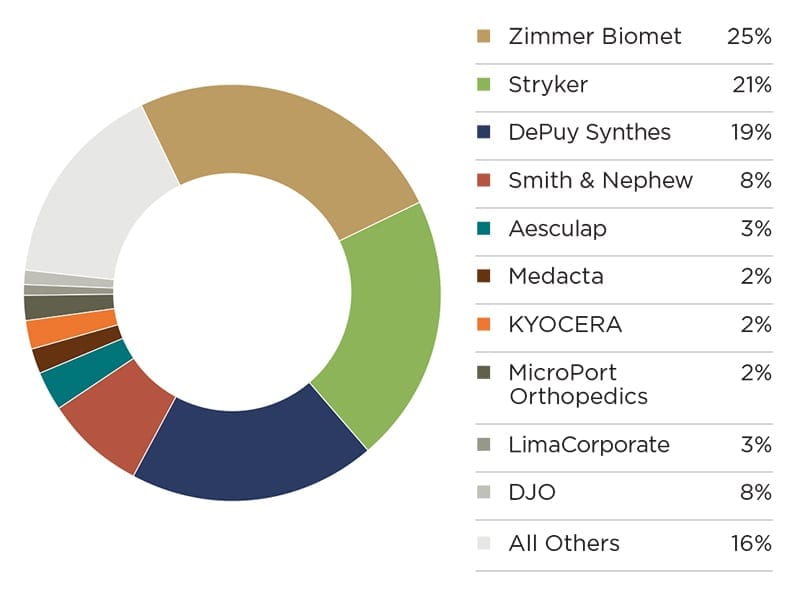

Exhibit 2: 2018 Hip Replacement Market Share – Top 10 Companies and All Others

Zimmer Biomet, Stryker, DePuy Synthes and Smith & Nephew control 73% of the hip replacement market. These four players combined for below-market growth, finishing 2018 at +2.4% vs. 2017. Zimmer Biomet improved over its 2017 results, in part due to the supply issues that were addressed in 2018. Hip replacement is one of the few segments where Stryker did not outperform the market in 2018, despite contributions from their Mako robot and the new TRIDENT II hip cup. DePuy Synthes launched their ACTIS total hip in the first quarter of 2018, but still experienced growth deceleration compared to 2017.

Leadership at Smith & Nephew believes that the company has better technology in hip replacement than recent sales indicate, and is excited about their hip replacement product pipeline. Smith & Nephew CEO Namal Nawana said, “When I joined the company, Smith & Nephew had basically a decade of flat growth in hips. And I said, ‘Hey, we’ve got a great hip portfolio, and we’re going to grow it.’ We’ve had two quarters at 4% growth (before currency exchange).” He continued, “I’m very excited about our Dual Mobility product with its OXINIUM bearing services. It’s another product that allows us to access one of those faster-growing product segments in hip replacement.”

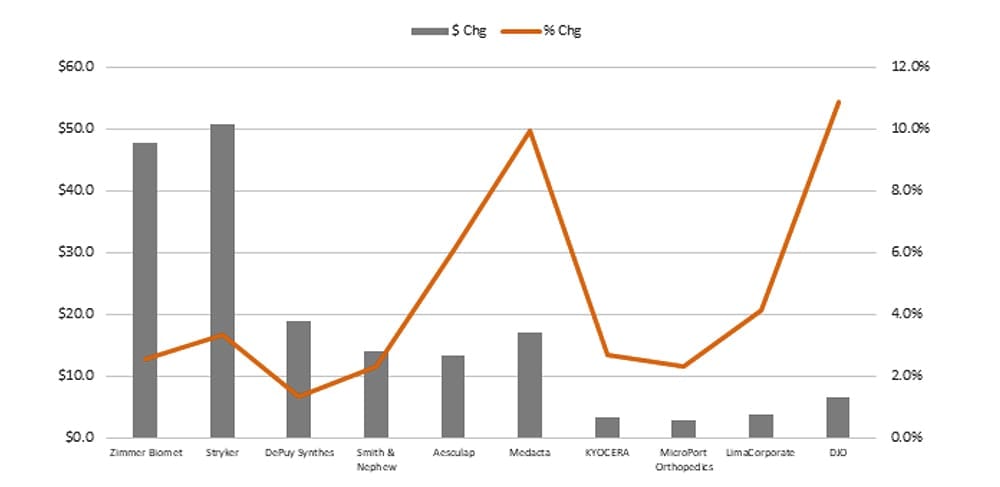

Medacta and DJO performed very well in the next-tier players, reaching double-digit growth in hip replacement, albeit on a smaller scale. To contextualize the growth rates for the top ten hip replacement companies in 2018, Exhibit 3 overlays revenue and percentage growth.

Exhibit 3: 2018 Hip Replacement Revenue and Percentage Growth – Top 10 Companies

Turning now to 2019, the top four players were mostly flat in the first quarter with +0.4% growth as shown in Exhibit 4.

Exhibit 4: 2019 Q1 Hip Replacement Sales Performance – Top Four Public Companies

| Companies | 2019Q1 | 2018Q1 | $ Chg | % Chg |

| Zimmer Biomet | $484.2 | $492.0 | -$7.8 | -1.6% |

| Stryker | $395.9 | $380.7 | $15.2 | 4.0% |

| DePuy Synthes | $370.5 | $369.2 | $1.3 | 30.0% |

| Smith & Nephew | $152.0 | $155.0 | -$3.0 | -1.9% |

| Total | $1,402.6 | $1,396.9 | $5.7 | 0.4% |

Only Stryker managed appreciable growth (+4%) on the strength of their new 3D printed acetabular cup and continuing Mako adoption. At the end of 1Q19, Stryker had 700 Mako units installed (550 in the U.S.) with utilization rates up 30% vs. the prior year. More than half of the units installed in the first quarter went into accounts where Stryker has little or no market share. We estimate that approximately 40% of all Mako procedures are hip replacements.

DePuy Synthes grew their U.S. hip franchise by +2%, but this was offset by a decline in ex-U.S. markets. Smith & Nephew’s growth was +2.4% before the impact of currency exchange headwinds. The company is well positioned for accelerating growth as they’ll launch Brainlab’s hip software for NAVIO in the second half of the year. These gains will be moderated somewhat by supply issues that will continue to resolve throughout the year.

Smaller players stayed active going into 2019, with new hip joint replacement product launches from both DJO (ADAPTABLE surgical arm) and LimaCorporate (3D printed DELTA TT Pro Acetabular System). In March of this year, Exactech received FDA 510(k) clearance to market the Alteon Acetabular Cup and XLE Liner.

We project that the hip joint replacement market will grow +3.2% in 2019, in line with performance of recent years. Zimmer Biomet CEO Bryan Hanson echoed this view when he said, “I don’t really put a lot of weight into what happens in a single quarter. There’s just too many moving variables. It could be for any organization, positive or negative comps, they could be running through with billing day differences. There are just a lot of things that could happen inside of an individual quarter. From our assumptions that we built into 2019 as we put on our guidance, we pretty much expect 2019 to look a lot like 2018 and 2017. There is always slight variation, obviously. But we’re expecting 2019 to look pretty similar to 2018. Hoping we’re wrong and the volume is better than that.”

Mike Evers is ORTHOWORLD’s Market Analyst.

The global hip joint replacement market grew 3.2% in 2018 vs. 2017, reaching revenue of USD $7.6 billion. We project that the market will reach $8.9 billion by 2023. In this article, we’ll dive deeper into company performance for 2018 and review results from the first quarter of 2019.

In Exhibits 1 and 2, we look at 2018 hip replacement sales...

The global hip joint replacement market grew 3.2% in 2018 vs. 2017, reaching revenue of USD $7.6 billion. We project that the market will reach $8.9 billion by 2023. In this article, we’ll dive deeper into company performance for 2018 and review results from the first quarter of 2019.

In Exhibits 1 and 2, we look at 2018 hip replacement sales for players with revenue over $50MM as well as market share for the top ten players.

Exhibit 1: 2018 Hip Replacement Sales Performance – Companies Over $50MM and All Others

| Companies | 2018 | 2017 | $ Chg | % Chg |

| Zimmer Biomet | $1,921.4 | $1,873.7 | $47.7 | 2.5% |

| Stryker | $1,571.0 | $1,520.2 | $50.8 | 3.3% |

| DePuy Synthes | $1,443.9 | $1,424.9 | $19.0 | 1.3% |

| Top-Tier Subtotal | $4,936.3 | $4,818.8 | $117.5 | 2.4% |

| Smith & Nephew | $613.0 | $599.0 | $14.0 | 2.3% |

| Aesculap | $232.0 | $218.7 | $13.3 | 6.1% |

| Medacta | $187.8 | $170.8 | $17.0 | 10.0% |

| KYOCERA | $130.5 | $127.1 | $3.4 | 2.7% |

| MicroPort Orthopedics | $125.2 | $122.4 | $2.8 | 2.3% |

| LimaCorporate | $98.4 | $94.5 | $3.9 | 4.1% |

| DJO | $68.3 | $61.6 | $6.7 | 10.9% |

| Waldemar Link | $64.9 | $63.1 | $1.8 | 2.9% |

| Mathys | $63.7 | $61.8 | $1.9 | 3.0% |

| Corin | $60.0 | $55.8 | $4.2 | 7.5% |

| Exactech | $53.9 | $51.0 | $2.9 | 5.7% |

| Next-Tier Subtotal | $1,697.8 | $1,625.8 | $72.0 | 4.4% |

| All Others | $948.2 | $904.8 | $43.4 | 4.8% |

| Total | $7,582.3 | $7,349.4 | $232.9 | 3.2% |

Exhibit 2: 2018 Hip Replacement Market Share – Top 10 Companies and All Others

Zimmer Biomet, Stryker, DePuy Synthes and Smith & Nephew control 73% of the hip replacement market. These four players combined for below-market growth, finishing 2018 at +2.4% vs. 2017. Zimmer Biomet improved over its 2017 results, in part due to the supply issues that were addressed in 2018. Hip replacement is one of the few segments where Stryker did not outperform the market in 2018, despite contributions from their Mako robot and the new TRIDENT II hip cup. DePuy Synthes launched their ACTIS total hip in the first quarter of 2018, but still experienced growth deceleration compared to 2017.

Leadership at Smith & Nephew believes that the company has better technology in hip replacement than recent sales indicate, and is excited about their hip replacement product pipeline. Smith & Nephew CEO Namal Nawana said, “When I joined the company, Smith & Nephew had basically a decade of flat growth in hips. And I said, ‘Hey, we’ve got a great hip portfolio, and we’re going to grow it.’ We’ve had two quarters at 4% growth (before currency exchange).” He continued, “I’m very excited about our Dual Mobility product with its OXINIUM bearing services. It’s another product that allows us to access one of those faster-growing product segments in hip replacement.”

Medacta and DJO performed very well in the next-tier players, reaching double-digit growth in hip replacement, albeit on a smaller scale. To contextualize the growth rates for the top ten hip replacement companies in 2018, Exhibit 3 overlays revenue and percentage growth.

Exhibit 3: 2018 Hip Replacement Revenue and Percentage Growth – Top 10 Companies

Turning now to 2019, the top four players were mostly flat in the first quarter with +0.4% growth as shown in Exhibit 4.

Exhibit 4: 2019 Q1 Hip Replacement Sales Performance – Top Four Public Companies

| Companies | 2019Q1 | 2018Q1 | $ Chg | % Chg |

| Zimmer Biomet | $484.2 | $492.0 | -$7.8 | -1.6% |

| Stryker | $395.9 | $380.7 | $15.2 | 4.0% |

| DePuy Synthes | $370.5 | $369.2 | $1.3 | 30.0% |

| Smith & Nephew | $152.0 | $155.0 | -$3.0 | -1.9% |

| Total | $1,402.6 | $1,396.9 | $5.7 | 0.4% |

Only Stryker managed appreciable growth (+4%) on the strength of their new 3D printed acetabular cup and continuing Mako adoption. At the end of 1Q19, Stryker had 700 Mako units installed (550 in the U.S.) with utilization rates up 30% vs. the prior year. More than half of the units installed in the first quarter went into accounts where Stryker has little or no market share. We estimate that approximately 40% of all Mako procedures are hip replacements.

DePuy Synthes grew their U.S. hip franchise by +2%, but this was offset by a decline in ex-U.S. markets. Smith & Nephew’s growth was +2.4% before the impact of currency exchange headwinds. The company is well positioned for accelerating growth as they’ll launch Brainlab’s hip software for NAVIO in the second half of the year. These gains will be moderated somewhat by supply issues that will continue to resolve throughout the year.

Smaller players stayed active going into 2019, with new hip joint replacement product launches from both DJO (ADAPTABLE surgical arm) and LimaCorporate (3D printed DELTA TT Pro Acetabular System). In March of this year, Exactech received FDA 510(k) clearance to market the Alteon Acetabular Cup and XLE Liner.

We project that the hip joint replacement market will grow +3.2% in 2019, in line with performance of recent years. Zimmer Biomet CEO Bryan Hanson echoed this view when he said, “I don’t really put a lot of weight into what happens in a single quarter. There’s just too many moving variables. It could be for any organization, positive or negative comps, they could be running through with billing day differences. There are just a lot of things that could happen inside of an individual quarter. From our assumptions that we built into 2019 as we put on our guidance, we pretty much expect 2019 to look a lot like 2018 and 2017. There is always slight variation, obviously. But we’re expecting 2019 to look pretty similar to 2018. Hoping we’re wrong and the volume is better than that.”

Mike Evers is ORTHOWORLD’s Market Analyst.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.