Copy to clipboard

Copy to clipboard

In October, we sat down with leaders from Globus Medical to discuss their surprising entrance into the joint replacement market and robotics’ role in orthopedic surgery. As a quick refresher, during 2Q19 Globus Medical announced that it had acquired substantially all of the assets of StelKast, a privately-held manufacturer of knee and hip replacement implants and instruments. Globus paid USD $24.1 million in cash upfront with an additional potential $4.3 million in product milestone payments. Globus is expected to commercialize a robotic system for joint replacement in late 2020.

During our conversation, Globus Senior Vice President of Business Development Brian Kearns said that the nearly $775 million company (See Exhibit 1.) had historically not been interested in the joint replacement market. From his perspective, the top joint players—Zimmer Biomet, Stryker, DePuy Synthes, and Smith+Nephew—had the market well covered and outcomes are generally very good.

So, what changed?

A Strong Core Competency in Robotics and Technology

Per Mr. Kearns, the answer goes back to 2014 when Globus acquired Excelsius Surgical and started developing robotics expertise around its ExcelsiusGPS platform for spine surgery.

Since then, the company’s focus on developing a pipeline of disruptive technology has driven near double-digit growth in the spine market where segment-wide growth is only projected at nearly 2% in 2019.

A common theme among analysts and investors at NASS 2019 was the superiority of Globus’ platform versus the competition, with PiperJaffray’s industry note remarking, “We continue to believe GMED remains the technology leader at this point.” This technological advantage convinced Globus leadership that they could innovate in the joint replacement space.

During the 2Q19 earnings conference call, company President and CEO David Demski said that Globus had been working on a joint replacement robot for several quarters and accelerated that investment in the first quarter leading up to the acquisition of StelKast. He went on to say, “We’ve seen the impact that robotics can have on the implant business, and we’re very happy with the success we’ve had in spine. We think we’ve developed a really strong core competency there. We’ve got a great team. We were looking for other ways to leverage that technology, and looking at the success that other companies have had in total joints thought that was a logical place to go. We wanted to buy an implant manufacturer with a strong track record of safety and reliability, so we weren’t really looking for [a company with] revenue.”

In spine, Globus has continued to iterate upon the ExcelsiusGPS platform with imaging, navigation and robotic additions—a combination that the company believes provides a strategic advantage and is a signal of what might be important in future joint replacement enabling technology. Globus’ Interbody Solutions offers navigation and real-time feedback during dilation, disc preparation, and implant insertion. Globus is the only player to offer interbody placement with its robotic system, presently. Beyond robotics, the company is also expanding its enabling technology offerings through the development of the Globus Imaging System (GIS), slated to launch in 2020. GIS comprises a mobile combination C- and O-arm that provides fluoroscopy, digital radiation, and CT scan. GIS will be fully integrated into Globus’ robotic and navigation tools.

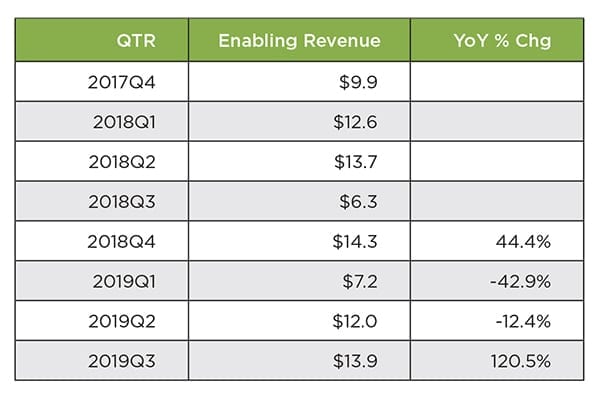

One area in which Globus is potentially challenged, however, is in its ability to place enabling technology units at the same rate as its larger competitors, likely due to its smaller sales force. After an initial strong start due to pent-up demand for ExcelsiusGPS at launch in 4Q17, revenue growth for Globus’s Enabling Technology reporting segment trailed off and hit an especially weak 1Q19 (-42.9% year over year). However, Globus returned to form in the normally soft capital sales third quarter with $13.9MM in revenue for their enabling technologies, +120.5% year-over-year growth. Exhibit 2 depicts the company’s sequential quarterly growth in enabling technology since 4Q17.

Exhibit 1: Globus Medical Revenue 2017-2019P ($Millions)

Exhibit 2: Globus Medical Revenue and Growth by Quarter ($Millions)

Opportunities in the Joint Replacement Market

Globus’ Senior Vice President and CFO Keith Pfeil laid out a “Crawl – Walk – Run” strategy for the company’s entry into joint replacement, with the aim to achieve best-in-class implant hardware and robotics. However, Mr. Kearns didn’t mince words when asked who Globus’ direct competitors in that space would be, saying that they’re going after the top players straight away (Zimmer Biomet, Stryker, DePuy Synthes, and Smith+Nephew). When Globus fully enters the joint replacement market, it will be competing against massive international companies with vast resources and salesforces and which hold 82% of the $9 billion knee replacement market and 73% of the $7.5 billion hip replacement market, according to our estimates. However, the company is used to contending with behemoths, as they share the spine segment with Medtronic and DePuy Synthes.

In his 2Q19 earnings call remarks, Mr. Demski said that the company has recognized that ExcelsiusGPS is a consistent value-add by watching spine surgeons utilize the technology in the O.R. “We know our technology is better today. We believe in it strongly. We’re going to continue to win in terms of the way the technology works…We know how this incorporates into surgical practices.”

Mr. Kearns echoed those sentiments in relation to the joint replacement market. To him, one of the company’s key strengths is their ability and willingness to work so closely with their surgeon partners to address pain points of current offerings on the market—even if it means cannibalizing product lines. Additionally, Globus doesn’t have a vast, entrenched business in joint replacement to protect. They can be disruptive and agile in ways that their larger competitors in the space cannot. Notably, Globus’ run of success coincides with missteps and setbacks from some of their future joint replacement competitors.

Zimmer Biomet

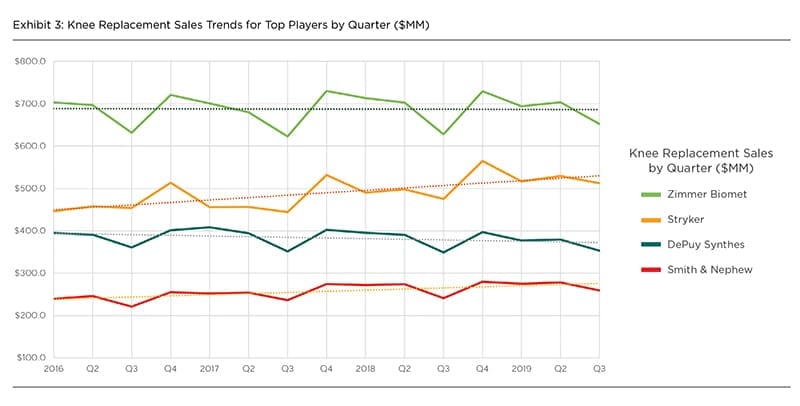

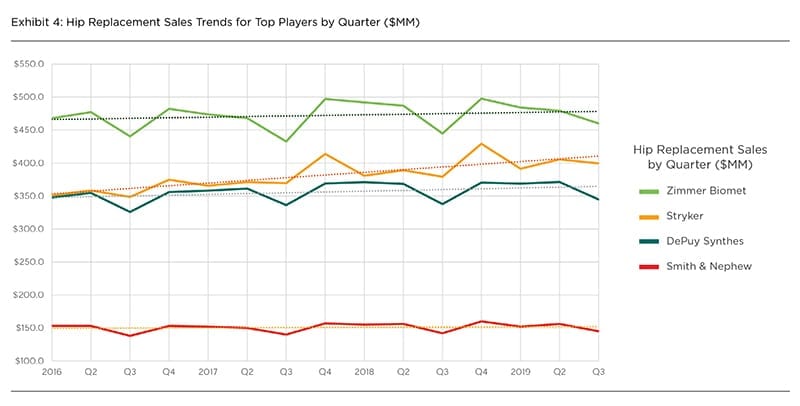

Despite their recent challenges, Zimmer Biomet still reigns supreme in knee and hip replacement through sheer size and controls 26% of the joint replacement market. However, their average quarter-over-quarter growth is just 0.4% for knees and 1.1% for hips going back to 2016. Even with the recent launch of the ROSA total knee application, Zimmer Biomet is still contending with the necessity of revamping and reducing the scope of its portfolio while regaining the trust of a salesforce that’s been burned by supply chain instability. Company leadership has long targeted 2020 as the end-goal of their lengthy recovery effort—just in time for Globus Medical to enter the fray in joint replacement.

DePuy Synthes

DePuy Synthes has also experienced headwinds in their knee franchise, with average quarter-over-quarter declines of -1% since 2016 while faring better in hip replacement, with an average growth of 1.8%. The company controls 17% of the joint replacement market. DePuy Synthes has largely been donating knee share to Stryker as Mako enters and converts key accounts. DePuy Synthes leadership believes that the addition of a cementless knee and their Orthotaxy robotic platform (expected to launch in 2020 or 2021) can turn the tide. Like Globus, DePuy Synthes has been gathering robotics expertise with the acquisition of Auris Health to enhance their digital surgery capabilities, but it remains to be seen whether Orthotaxy will bring anything new to the robotic-assisted surgery market.

Smith+Nephew

Smith+Nephew accounts for 9% of the joint replacement market and has averaged 4.8% quarter-over-quarter growth in knees since 2016, with strong performances in late 2017 and early 2018. Strong NAVIO sales and the May 2019 acquisition of Brainlab’s joint replacement business brought a much-needed infusion of growth in 3Q19, with the company driving knee replacement sales up 7.6% year over year after growing in the low single digits from 3Q18 through 2Q19. They are largely treading water with their hip franchise, averaging 1% quarter-over-quarter growth. Smith+Nephew had been behind the curve on robotics, with former CEO Namal Nawana saying in late 2018, “[Robotics is] an important part, not just in knee replacement, but more broadly in surgery. We still have some improvements to make on how we operate and how we serve our customers, and I expect our teams to lift in that area, as well as gain their understanding of how robotics can help their customers.” However, the acquisitions of Atracsys’ fusionTrack 500 optical tracking camera and Brainlab’s surgical navigation assets are expected to be integral parts of the company’s robotic-assisted surgery platform that is slated to launch mid-2020.

Stryker

Best in class enabling technology and implant hardware will be a key to competing with Stryker in joint replacement, where the company commands 21% of the market. Going back to 2016, Stryker has averaged 4.8% year-over-year growth in knees, and accelerated that growth to 7.1% since the start of 2018. Likewise, their hip franchise has consistently grown a quarter-over-quarter average of 4.7% for our timeframe. As of 3Q19, the company had placed nearly 800 Mako units globally (over 600 in the U.S.) and performed 27,000 Mako procedures in that quarter. Per company leadership, the growth of the knee segment was driven primarily by the conversion of competitive accounts. This represents a significant barrier to entry for players lagging in robotics development. Even Globus, with their proven track record of technology, has a hill to climb to overcome Stryker’s head start.

Exhibit 3 and Exhibit 4 display the top four players’ quarter-over-quarter knee and hip replacement sales going back to 2016.

The question that remains is: How big of a splash can Globus Medical make in the joint replacement market? They certainly have expertise in robotics and enabling technology to be disruptive. We believe that their product development team will be able to create something innovative out of the small portfolio acquired from StelKast, but will it be enough to tempt surgeons away from the largest players that have been mainstays in joint replacement and which, themselves, will be launching new robots in the coming year or two? Can Globus create enough scale in their joint replacement portfolio to challenge the top tier players, or will they seek another acquisition to bolster their hardware lineup? This is a storyline that will play out over the long term, well beyond the targeted late 2020 launch, and will require patience from stakeholders and observers alike.

The Future: A Full Musculoskeletal Company

As we wrapped up our meeting, we asked Mr. Kearns to speculate on the future of robotics in orthopedics. He predicted that within 10 years, most orthopedic surgery would employ robotics of some kind, and the next wave of orthopedic robot innovation will incorporate features focused on soft tissue. In the interim, Globus is focused on becoming a fully diversified musculoskeletal company. As their internally developed trauma line continues to ramp up slowly, the company plans to enter the sports medicine market in the coming years. The success or failure of their entry into joint replacement is likely to be a bellwether for the company’s overall evolution.

Mike Evers is ORTHOWORLD’s Digital Content Strategist. He can be reached by email.

In October, we sat down with leaders from Globus Medical to discuss their surprising entrance into the joint replacement market and robotics’ role in orthopedic surgery. As a quick refresher, during 2Q19 Globus Medical announced that it had acquired substantially all of the assets of StelKast, a privately-held manufacturer of knee and hip...

In October, we sat down with leaders from Globus Medical to discuss their surprising entrance into the joint replacement market and robotics’ role in orthopedic surgery. As a quick refresher, during 2Q19 Globus Medical announced that it had acquired substantially all of the assets of StelKast, a privately-held manufacturer of knee and hip replacement implants and instruments. Globus paid USD $24.1 million in cash upfront with an additional potential $4.3 million in product milestone payments. Globus is expected to commercialize a robotic system for joint replacement in late 2020.

During our conversation, Globus Senior Vice President of Business Development Brian Kearns said that the nearly $775 million company (See Exhibit 1.) had historically not been interested in the joint replacement market. From his perspective, the top joint players—Zimmer Biomet, Stryker, DePuy Synthes, and Smith+Nephew—had the market well covered and outcomes are generally very good.

So, what changed?

A Strong Core Competency in Robotics and Technology

Per Mr. Kearns, the answer goes back to 2014 when Globus acquired Excelsius Surgical and started developing robotics expertise around its ExcelsiusGPS platform for spine surgery.

Since then, the company’s focus on developing a pipeline of disruptive technology has driven near double-digit growth in the spine market where segment-wide growth is only projected at nearly 2% in 2019.

A common theme among analysts and investors at NASS 2019 was the superiority of Globus’ platform versus the competition, with PiperJaffray’s industry note remarking, “We continue to believe GMED remains the technology leader at this point.” This technological advantage convinced Globus leadership that they could innovate in the joint replacement space.

During the 2Q19 earnings conference call, company President and CEO David Demski said that Globus had been working on a joint replacement robot for several quarters and accelerated that investment in the first quarter leading up to the acquisition of StelKast. He went on to say, “We’ve seen the impact that robotics can have on the implant business, and we’re very happy with the success we’ve had in spine. We think we’ve developed a really strong core competency there. We’ve got a great team. We were looking for other ways to leverage that technology, and looking at the success that other companies have had in total joints thought that was a logical place to go. We wanted to buy an implant manufacturer with a strong track record of safety and reliability, so we weren’t really looking for [a company with] revenue.”

In spine, Globus has continued to iterate upon the ExcelsiusGPS platform with imaging, navigation and robotic additions—a combination that the company believes provides a strategic advantage and is a signal of what might be important in future joint replacement enabling technology. Globus’ Interbody Solutions offers navigation and real-time feedback during dilation, disc preparation, and implant insertion. Globus is the only player to offer interbody placement with its robotic system, presently. Beyond robotics, the company is also expanding its enabling technology offerings through the development of the Globus Imaging System (GIS), slated to launch in 2020. GIS comprises a mobile combination C- and O-arm that provides fluoroscopy, digital radiation, and CT scan. GIS will be fully integrated into Globus’ robotic and navigation tools.

One area in which Globus is potentially challenged, however, is in its ability to place enabling technology units at the same rate as its larger competitors, likely due to its smaller sales force. After an initial strong start due to pent-up demand for ExcelsiusGPS at launch in 4Q17, revenue growth for Globus’s Enabling Technology reporting segment trailed off and hit an especially weak 1Q19 (-42.9% year over year). However, Globus returned to form in the normally soft capital sales third quarter with $13.9MM in revenue for their enabling technologies, +120.5% year-over-year growth. Exhibit 2 depicts the company’s sequential quarterly growth in enabling technology since 4Q17.

Exhibit 1: Globus Medical Revenue 2017-2019P ($Millions)

Exhibit 2: Globus Medical Revenue and Growth by Quarter ($Millions)

Opportunities in the Joint Replacement Market

Globus’ Senior Vice President and CFO Keith Pfeil laid out a “Crawl – Walk – Run” strategy for the company’s entry into joint replacement, with the aim to achieve best-in-class implant hardware and robotics. However, Mr. Kearns didn’t mince words when asked who Globus’ direct competitors in that space would be, saying that they’re going after the top players straight away (Zimmer Biomet, Stryker, DePuy Synthes, and Smith+Nephew). When Globus fully enters the joint replacement market, it will be competing against massive international companies with vast resources and salesforces and which hold 82% of the $9 billion knee replacement market and 73% of the $7.5 billion hip replacement market, according to our estimates. However, the company is used to contending with behemoths, as they share the spine segment with Medtronic and DePuy Synthes.

In his 2Q19 earnings call remarks, Mr. Demski said that the company has recognized that ExcelsiusGPS is a consistent value-add by watching spine surgeons utilize the technology in the O.R. “We know our technology is better today. We believe in it strongly. We’re going to continue to win in terms of the way the technology works…We know how this incorporates into surgical practices.”

Mr. Kearns echoed those sentiments in relation to the joint replacement market. To him, one of the company’s key strengths is their ability and willingness to work so closely with their surgeon partners to address pain points of current offerings on the market—even if it means cannibalizing product lines. Additionally, Globus doesn’t have a vast, entrenched business in joint replacement to protect. They can be disruptive and agile in ways that their larger competitors in the space cannot. Notably, Globus’ run of success coincides with missteps and setbacks from some of their future joint replacement competitors.

Zimmer Biomet

Despite their recent challenges, Zimmer Biomet still reigns supreme in knee and hip replacement through sheer size and controls 26% of the joint replacement market. However, their average quarter-over-quarter growth is just 0.4% for knees and 1.1% for hips going back to 2016. Even with the recent launch of the ROSA total knee application, Zimmer Biomet is still contending with the necessity of revamping and reducing the scope of its portfolio while regaining the trust of a salesforce that’s been burned by supply chain instability. Company leadership has long targeted 2020 as the end-goal of their lengthy recovery effort—just in time for Globus Medical to enter the fray in joint replacement.

DePuy Synthes

DePuy Synthes has also experienced headwinds in their knee franchise, with average quarter-over-quarter declines of -1% since 2016 while faring better in hip replacement, with an average growth of 1.8%. The company controls 17% of the joint replacement market. DePuy Synthes has largely been donating knee share to Stryker as Mako enters and converts key accounts. DePuy Synthes leadership believes that the addition of a cementless knee and their Orthotaxy robotic platform (expected to launch in 2020 or 2021) can turn the tide. Like Globus, DePuy Synthes has been gathering robotics expertise with the acquisition of Auris Health to enhance their digital surgery capabilities, but it remains to be seen whether Orthotaxy will bring anything new to the robotic-assisted surgery market.

Smith+Nephew

Smith+Nephew accounts for 9% of the joint replacement market and has averaged 4.8% quarter-over-quarter growth in knees since 2016, with strong performances in late 2017 and early 2018. Strong NAVIO sales and the May 2019 acquisition of Brainlab’s joint replacement business brought a much-needed infusion of growth in 3Q19, with the company driving knee replacement sales up 7.6% year over year after growing in the low single digits from 3Q18 through 2Q19. They are largely treading water with their hip franchise, averaging 1% quarter-over-quarter growth. Smith+Nephew had been behind the curve on robotics, with former CEO Namal Nawana saying in late 2018, “[Robotics is] an important part, not just in knee replacement, but more broadly in surgery. We still have some improvements to make on how we operate and how we serve our customers, and I expect our teams to lift in that area, as well as gain their understanding of how robotics can help their customers.” However, the acquisitions of Atracsys’ fusionTrack 500 optical tracking camera and Brainlab’s surgical navigation assets are expected to be integral parts of the company’s robotic-assisted surgery platform that is slated to launch mid-2020.

Stryker

Best in class enabling technology and implant hardware will be a key to competing with Stryker in joint replacement, where the company commands 21% of the market. Going back to 2016, Stryker has averaged 4.8% year-over-year growth in knees, and accelerated that growth to 7.1% since the start of 2018. Likewise, their hip franchise has consistently grown a quarter-over-quarter average of 4.7% for our timeframe. As of 3Q19, the company had placed nearly 800 Mako units globally (over 600 in the U.S.) and performed 27,000 Mako procedures in that quarter. Per company leadership, the growth of the knee segment was driven primarily by the conversion of competitive accounts. This represents a significant barrier to entry for players lagging in robotics development. Even Globus, with their proven track record of technology, has a hill to climb to overcome Stryker’s head start.

Exhibit 3 and Exhibit 4 display the top four players’ quarter-over-quarter knee and hip replacement sales going back to 2016.

The question that remains is: How big of a splash can Globus Medical make in the joint replacement market? They certainly have expertise in robotics and enabling technology to be disruptive. We believe that their product development team will be able to create something innovative out of the small portfolio acquired from StelKast, but will it be enough to tempt surgeons away from the largest players that have been mainstays in joint replacement and which, themselves, will be launching new robots in the coming year or two? Can Globus create enough scale in their joint replacement portfolio to challenge the top tier players, or will they seek another acquisition to bolster their hardware lineup? This is a storyline that will play out over the long term, well beyond the targeted late 2020 launch, and will require patience from stakeholders and observers alike.

The Future: A Full Musculoskeletal Company

As we wrapped up our meeting, we asked Mr. Kearns to speculate on the future of robotics in orthopedics. He predicted that within 10 years, most orthopedic surgery would employ robotics of some kind, and the next wave of orthopedic robot innovation will incorporate features focused on soft tissue. In the interim, Globus is focused on becoming a fully diversified musculoskeletal company. As their internally developed trauma line continues to ramp up slowly, the company plans to enter the sports medicine market in the coming years. The success or failure of their entry into joint replacement is likely to be a bellwether for the company’s overall evolution.

Mike Evers is ORTHOWORLD’s Digital Content Strategist. He can be reached by email.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.