Copy to clipboard

Copy to clipboard

Despite normal seasonal softness in capital sales, the first quarter of 2019 was an active one for robotic and digital surgery developments. New entrants into the orthopedic robot market like Zimmer Biomet’s ROSA Knee may lead to longer buying cycles as hospital administrators thoroughly evaluate each option. As adoption of digital surgery tools increases, leadership from joint replacement and spine companies indicated during first quarter earnings calls that they have seen a direct sales benefit from upselling and product pull through.

Seasonal Softness and New Competition

Joint Reconstruction

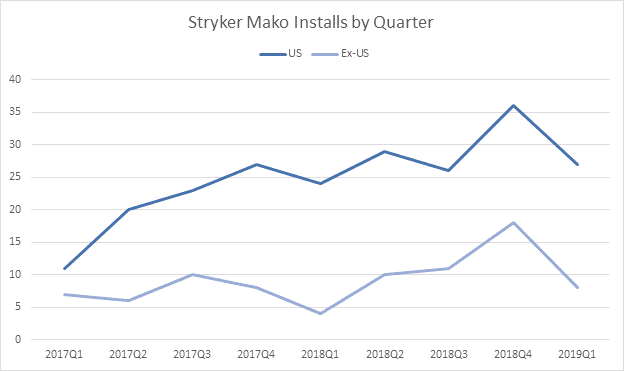

Stryker ended the first quarter of 2019 with 35 Mako installs, 27 of which were in the U.S. While the company historically sees soft first quarters on capital sales, they were able to place 55% of the installed units for the quarter into competitive accounts where Stryker has little or no market share. After increasing in four consecutive quarters, total knee procedures as a percentage of all Mako procedures was flat. Company leadership noted that both seasonality and normal utilization ramp time for newly installed units were factors. Exhibits 1 and 2 show quarterly trend data for Mako installs and procedures.

With a total global install base nearing 700 units, the company sees plenty of growth opportunity. Katherine Owen, Stryker Vice President of Strategy and Investor Relations, said, “Penetration rates in our own business are still very low. We believe the competition is going to do what it typically does in most markets; it’s going to raise awareness and interest and help to grow the overall space. Given the unique features and benefits and mounting clinical data in support of our robot, we feel bullish about the outlook.”

The competition is, of course, Zimmer Biomet’s ROSA Knee that is in limited launch. The company says they’ve received “extremely positive” feedback and are increasingly confident that ROSA will allow their key high-volume surgeons to achieve time neutrality in the robotic procedure. Additionally, Zimmer Biomet recently received regulatory clearance for a spine application that will allow them to expand the orthopedic footprint of ROSA.

Spine

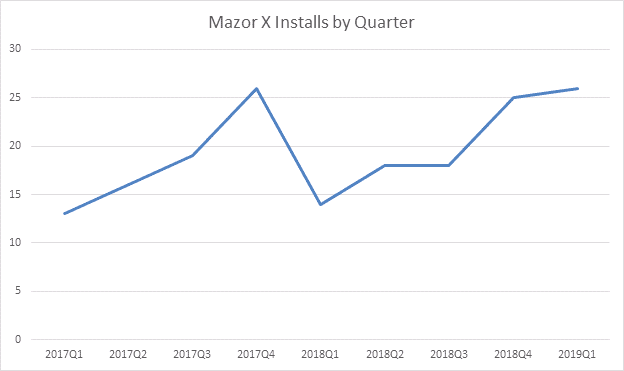

Medtronic sold 26 Mazor X systems in their first quarter after closing their acquisition of Mazor Robotics. Per leadership, the company now controls 70% of the spine robot market, with three and a half times the installs of their next closest competitor. Over 80% of Mazor X systems are sold with contracts that combine the capital equipment and implant commitments from the hospital. Indeed, Medtronic saw a double-digit increase in use of Medtronic implants with Mazor X systems vs. last quarter. Exhibit 3 shows Mazor X installs by quarter. Please note that we’ve estimated the number of units installed prior to the close of the acquisition.

Globus Medical’s ExcelsiusGPS generated $7.1 million in revenue from capital sales in 1Q, a 44% reduction from the prior year caused by seasonality and an artificially inflated comparison for 1Q 2018. ExcelsiusGPS experienced launch delays in late 2017 that led to significant pent up demand in early 2018. The company cited ExcelsiusGPS-driven product pull through as a key sales driver in the first quarter of 2019, and recently filed a 510(k) submission with FDA for an interbody module.

Exhibit 1: Stryker Mako Installs by Quarter

Exhibit 2: Stryker Mako Total Knee Application Procedure Trend

Exhibit 3: Medtronic Mazor X Installs by Quarter

New Market Entrants Elongate Buying Times

Another factor in Globus Medical’s lower-than-expected robotics sales is what CEO Dave Demski called an “elongation” of the buying times for robotics. He said, “We are also experiencing an elongation of the decision cycle by hospital executives in purchasing robotic systems due to the increase in marketing initiatives by our competition. Deals are taking longer to get finalized as accounts evaluate potential alternatives. In fact, we have already closed several deals in Q2 that we had expected to close in Q1.”

Zimmer Biomet’s agile development process for ROSA Knee led to continuous engagement with surgeon partners, giving them important insight into custom needs. “We had a specific development process that allowed significant engagement with surgeons along the way. [We did] quarter sprints from a development perspective, and each quarter would bring in surgeon partners to look at what was done, basically beat you up on what they don’t like, and then [would] do another quarter sprint to make those corrections. So, it’s not a surprise to us that it is being well received, because we had surgeon engagement throughout the entire development plan,” said Zimmer Biomet CEO Bryan Hanson.

Katherine Owen of Stryker said they have seen no difference in Mako order cycles, but did note that going forward the company will no longer provide granular data about unit placements in competitive accounts.

Driving Orthopedic Sales through Digital Surgery

Getting a capital sale on a robotic system is merely a first step toward generating a steady revenue stream as the focus turns to driving utilization. As robotic procedure adoption increases, players with integrated ecosystems will be able to leverage their robot to sell premium products.

For example, Zimmer Biomet believes the synergies of the Persona knee implant, ROSA and their mymobility digital health platform offer a unique patient experience and opportunity for improved sales mix. Bryan Hanson said, “What we love about this is, with these technologies that bring real value for our patients and our customers, you don’t have to have a new patient, you don’t have to convert a new surgeon. You just need to have the same surgical procedure, with the same patient, with the surgeon you’ve always had upsold to better technology. When that occurs, you get more share of wallet. You get more revenue per that procedure. That is absolutely something that we’re going to concentrate on.”

Medtronic leadership has noted the same trend. The benefit appears to extend to digital surgery products in general. Mike Coyle, President of Medtronic’s Cardiac and Vascular Group, said, “We’re clearly seeing faster growth and greater market share versus accounts where we don’t have a robot. And that same can be said to maybe a slightly lesser degree when we have navigation in the OR without the robot. Where we have enabling technology, our value proposition is better and we’re seeing faster growth and better market share.”

Companies are beginning to look beyond a single robotic system with a narrow procedural focus. Smith & Nephew plans to have multiple assets in their digital surgery and robotics ecosystem, with broad-based use of robotics throughout their portfolio. The company also plans to integrate their robots with additional technologies like augmented reality. This approach is closely aligned with NuVasive’s vision for Pulse as an “application rich environment” in which their upcoming robot is simply a mechanical automation layer that will provide broad support for various clinical applications.

Wright Medical has firmly embraced software as the way forward, having said repeatedly they don’t believe robotics to currently be a good fit for small, complex joints. Wright Medical CEO Bob Palmisano said, “I think that in terms of the small joint and what we have confirmed is that software is a much more elegant solution than robotics. [Software] will be a leapfrog over robotics, which is a mechanical system that is expensive, needs maintenance and has not yet at all been, I think, developed in small joints. I think software is a much more elegant solution than robotics in these areas.”

The company attributed share gains and approximately 130 new shoulder customers primarily to their BLUEPRINT technology. Additionally, Wright Medical created a new digital organization within the company to expand their digital surgery pipeline, including into new areas of lower extremities. In that pipeline are two developments for the BLUEPRINT shoulder application: an outcomes database that syncs with a patient’s smartphone and allows the surgeon to improve their practice over time, and artificial intelligence-derived surgical recommendations drawn from a database of stored cases.

Whether specific robotic systems in orthopedics become ubiquitous or fade into obsolescence, the top companies are aligning their strategic initiatives and resources around an integrated approach to technology and products. The early adopters of digital and robotic technology benefited, thus far, from being first to market. As competition in the segment increases, it will be interesting to watch how selling and adoption strategies change.

Mike Evers is ORTHOWORLD’s Market Analyst.

Despite normal seasonal softness in capital sales, the first quarter of 2019 was an active one for robotic and digital surgery developments. New entrants into the orthopedic robot market like Zimmer Biomet’s ROSA Knee may lead to longer buying cycles as hospital administrators thoroughly evaluate each option. As adoption of digital surgery tools...

Despite normal seasonal softness in capital sales, the first quarter of 2019 was an active one for robotic and digital surgery developments. New entrants into the orthopedic robot market like Zimmer Biomet’s ROSA Knee may lead to longer buying cycles as hospital administrators thoroughly evaluate each option. As adoption of digital surgery tools increases, leadership from joint replacement and spine companies indicated during first quarter earnings calls that they have seen a direct sales benefit from upselling and product pull through.

Seasonal Softness and New Competition

Joint Reconstruction

Stryker ended the first quarter of 2019 with 35 Mako installs, 27 of which were in the U.S. While the company historically sees soft first quarters on capital sales, they were able to place 55% of the installed units for the quarter into competitive accounts where Stryker has little or no market share. After increasing in four consecutive quarters, total knee procedures as a percentage of all Mako procedures was flat. Company leadership noted that both seasonality and normal utilization ramp time for newly installed units were factors. Exhibits 1 and 2 show quarterly trend data for Mako installs and procedures.

With a total global install base nearing 700 units, the company sees plenty of growth opportunity. Katherine Owen, Stryker Vice President of Strategy and Investor Relations, said, “Penetration rates in our own business are still very low. We believe the competition is going to do what it typically does in most markets; it’s going to raise awareness and interest and help to grow the overall space. Given the unique features and benefits and mounting clinical data in support of our robot, we feel bullish about the outlook.”

The competition is, of course, Zimmer Biomet’s ROSA Knee that is in limited launch. The company says they’ve received “extremely positive” feedback and are increasingly confident that ROSA will allow their key high-volume surgeons to achieve time neutrality in the robotic procedure. Additionally, Zimmer Biomet recently received regulatory clearance for a spine application that will allow them to expand the orthopedic footprint of ROSA.

Spine

Medtronic sold 26 Mazor X systems in their first quarter after closing their acquisition of Mazor Robotics. Per leadership, the company now controls 70% of the spine robot market, with three and a half times the installs of their next closest competitor. Over 80% of Mazor X systems are sold with contracts that combine the capital equipment and implant commitments from the hospital. Indeed, Medtronic saw a double-digit increase in use of Medtronic implants with Mazor X systems vs. last quarter. Exhibit 3 shows Mazor X installs by quarter. Please note that we’ve estimated the number of units installed prior to the close of the acquisition.

Globus Medical’s ExcelsiusGPS generated $7.1 million in revenue from capital sales in 1Q, a 44% reduction from the prior year caused by seasonality and an artificially inflated comparison for 1Q 2018. ExcelsiusGPS experienced launch delays in late 2017 that led to significant pent up demand in early 2018. The company cited ExcelsiusGPS-driven product pull through as a key sales driver in the first quarter of 2019, and recently filed a 510(k) submission with FDA for an interbody module.

Exhibit 1: Stryker Mako Installs by Quarter

Exhibit 2: Stryker Mako Total Knee Application Procedure Trend

Exhibit 3: Medtronic Mazor X Installs by Quarter

New Market Entrants Elongate Buying Times

Another factor in Globus Medical’s lower-than-expected robotics sales is what CEO Dave Demski called an “elongation” of the buying times for robotics. He said, “We are also experiencing an elongation of the decision cycle by hospital executives in purchasing robotic systems due to the increase in marketing initiatives by our competition. Deals are taking longer to get finalized as accounts evaluate potential alternatives. In fact, we have already closed several deals in Q2 that we had expected to close in Q1.”

Zimmer Biomet’s agile development process for ROSA Knee led to continuous engagement with surgeon partners, giving them important insight into custom needs. “We had a specific development process that allowed significant engagement with surgeons along the way. [We did] quarter sprints from a development perspective, and each quarter would bring in surgeon partners to look at what was done, basically beat you up on what they don’t like, and then [would] do another quarter sprint to make those corrections. So, it’s not a surprise to us that it is being well received, because we had surgeon engagement throughout the entire development plan,” said Zimmer Biomet CEO Bryan Hanson.

Katherine Owen of Stryker said they have seen no difference in Mako order cycles, but did note that going forward the company will no longer provide granular data about unit placements in competitive accounts.

Driving Orthopedic Sales through Digital Surgery

Getting a capital sale on a robotic system is merely a first step toward generating a steady revenue stream as the focus turns to driving utilization. As robotic procedure adoption increases, players with integrated ecosystems will be able to leverage their robot to sell premium products.

For example, Zimmer Biomet believes the synergies of the Persona knee implant, ROSA and their mymobility digital health platform offer a unique patient experience and opportunity for improved sales mix. Bryan Hanson said, “What we love about this is, with these technologies that bring real value for our patients and our customers, you don’t have to have a new patient, you don’t have to convert a new surgeon. You just need to have the same surgical procedure, with the same patient, with the surgeon you’ve always had upsold to better technology. When that occurs, you get more share of wallet. You get more revenue per that procedure. That is absolutely something that we’re going to concentrate on.”

Medtronic leadership has noted the same trend. The benefit appears to extend to digital surgery products in general. Mike Coyle, President of Medtronic’s Cardiac and Vascular Group, said, “We’re clearly seeing faster growth and greater market share versus accounts where we don’t have a robot. And that same can be said to maybe a slightly lesser degree when we have navigation in the OR without the robot. Where we have enabling technology, our value proposition is better and we’re seeing faster growth and better market share.”

Companies are beginning to look beyond a single robotic system with a narrow procedural focus. Smith & Nephew plans to have multiple assets in their digital surgery and robotics ecosystem, with broad-based use of robotics throughout their portfolio. The company also plans to integrate their robots with additional technologies like augmented reality. This approach is closely aligned with NuVasive’s vision for Pulse as an “application rich environment” in which their upcoming robot is simply a mechanical automation layer that will provide broad support for various clinical applications.

Wright Medical has firmly embraced software as the way forward, having said repeatedly they don’t believe robotics to currently be a good fit for small, complex joints. Wright Medical CEO Bob Palmisano said, “I think that in terms of the small joint and what we have confirmed is that software is a much more elegant solution than robotics. [Software] will be a leapfrog over robotics, which is a mechanical system that is expensive, needs maintenance and has not yet at all been, I think, developed in small joints. I think software is a much more elegant solution than robotics in these areas.”

The company attributed share gains and approximately 130 new shoulder customers primarily to their BLUEPRINT technology. Additionally, Wright Medical created a new digital organization within the company to expand their digital surgery pipeline, including into new areas of lower extremities. In that pipeline are two developments for the BLUEPRINT shoulder application: an outcomes database that syncs with a patient’s smartphone and allows the surgeon to improve their practice over time, and artificial intelligence-derived surgical recommendations drawn from a database of stored cases.

Whether specific robotic systems in orthopedics become ubiquitous or fade into obsolescence, the top companies are aligning their strategic initiatives and resources around an integrated approach to technology and products. The early adopters of digital and robotic technology benefited, thus far, from being first to market. As competition in the segment increases, it will be interesting to watch how selling and adoption strategies change.

Mike Evers is ORTHOWORLD’s Market Analyst.

You’ve reached your limit.

We’re glad you’re finding value in our content — and we’d love for you to keep going.

Subscribe now for unlimited access to orthopedic business intelligence.

ME

Mike Evers is a Senior Market Analyst and writer with over 15 years of experience in the medical industry, spanning cardiac rhythm management, ER coding and billing, and orthopedics. He joined ORTHOWORLD in 2018, where he provides market analysis and editorial coverage.